Europe Solid State Battery Market Research Report: Forecast (2026-2032)

Europe Solid State Battery Market - By Type (Thin Film Battery, Portable Battery), By Capacity (Below 20 mAh, 20 mAh - 500 mAh, Above 500 mAh), By Cell Type (Single-Cell Battery, M ... ulti-Cell Battery), By Application (Consumer Electronics, Electric Vehicles, Medical Devices, Wearables, Energy Harvesting, Wireless Sensors, Others), and others Read more

- Energy

- Mar 2026

- Pages 250

- Report Format: PDF, Excel, PPT

Europe Solid State Battery Market

Projected 28.44% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 139 Million

Market Size (2032)

USD 624 Million

Base Year

2025

Projected CAGR

28.44%

Leading Segments

By Cell Type: Multi-Cell Battery

Europe Solid State Battery Market Report Key Takeaways:

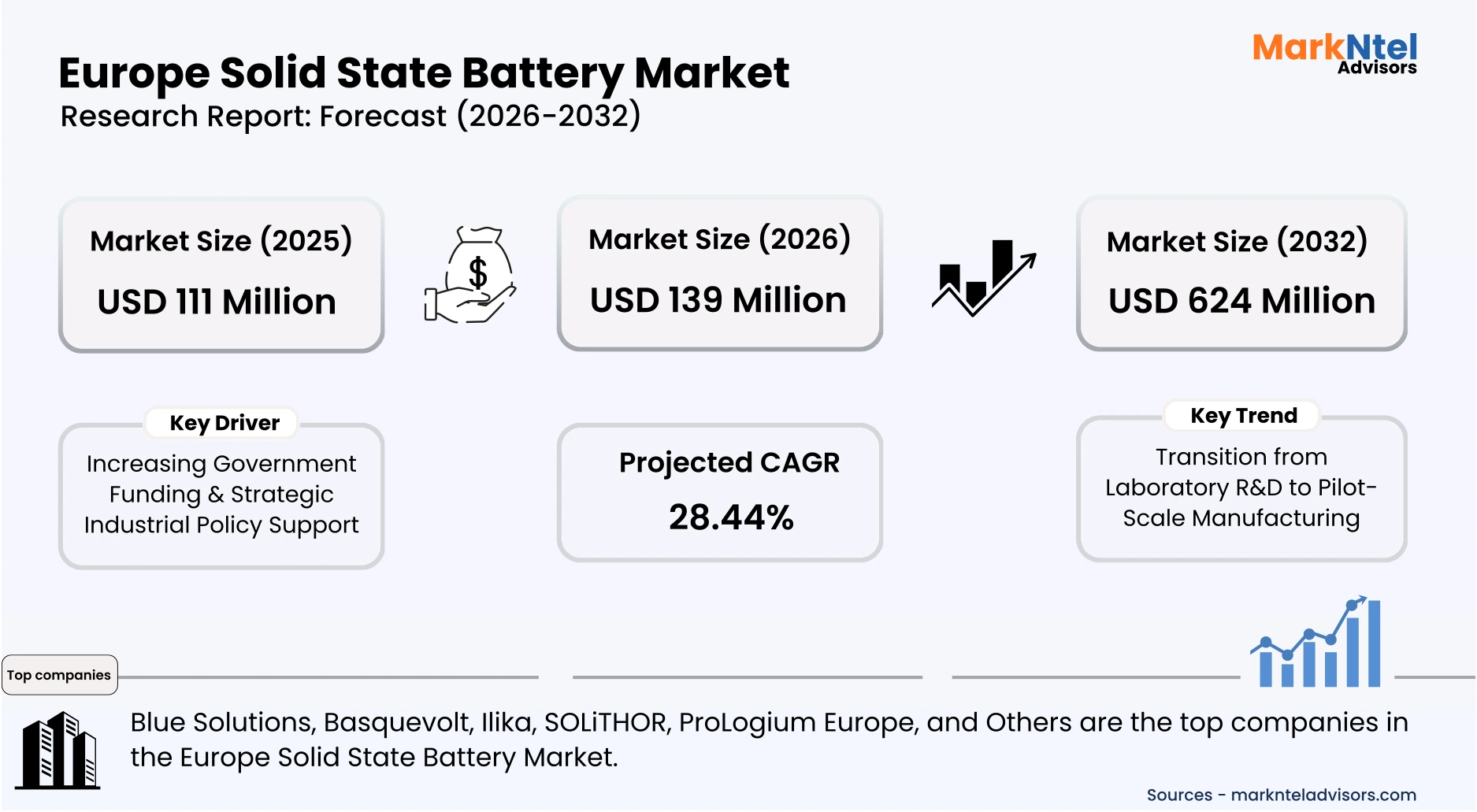

- Market size was valued at around USD 111 million in 2025 and is projected to grow from USD 139 million in 2026 to approximately USD 624 million by 2032. The estimated CAGR from 2026 to 2032 is around 28.44%, indicating strong growth.

- By Country, Germany is dominating this market by accounting for more than 19% of the market share in 2026.

- By Cell Type, multi-cell battery represented a significant market share of about 56% in the Europe Solid State Battery Market in 2026.

- By Application, the Electric Vehicles segment holds the largest market share of nearly 40% in the European Solid State Battery Industry in 2026.

- Leading Solid State Battery companies in Europe are Blue Solutions, Basquevolt, Ilika, SOLiTHOR, ProLogium Europe, and Others.

Market Insights & Analysis: Europe Solid State Battery Market (2026-32):

The Europe Solid State Battery Market size was valued at around USD 111 million in 2025 and is projected to grow from USD 139 million in 2026 to approximately USD 624 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 28.44% during the forecast period, i.e., 2026-32.

Europe’s solid-state battery market is gaining strong momentum as the region builds on its established electric-vehicle (EV) battery manufacturing base and aligns this capacity with long-term climate and industrial goals. For instance, in 2023, Europe produced about 110 GWh of EV batteries, supporting roughly 2.5 million electric vehicles, highlighting the region’s proven ability to manufacture batteries at scale, primarily using lithium-ion technology. This existing industrial strength is important because it provides the manufacturing expertise, skilled workforce, and supply-chain depth needed to gradually transition toward more advanced battery technologies such as solid-state systems.

Additionally, Europe is increasingly converting this manufacturing capability into concrete, solid-state investments. France is emerging as a key center of activity, with Blue Solutions announcing plans for a 25 GWh solid-state battery gigafactory targeting EV applications by 2030. This planned facility reflects a strategic move beyond conventional lithium-ion cells toward safer, higher-energy, and more thermally stable batteries that are better suited for next-generation EV platforms. Such investments indicate that solid-state batteries are no longer limited to research but are being prepared for industrial deployment.

Similarly, rising EV adoption and regulatory clarity are reinforcing this transition. The European Union’s long-term emissions reduction targets and commitment to zero-emission vehicles provide manufacturers with confidence to invest in next-generation batteries. Automotive OEMs across Europe are increasingly evaluating solid-state batteries to address key challenges such as driving range, safety, and battery lifespan, which are critical for mass-market EV adoption.

While solid-state battery production in Europe remains at pilot and early industrial stages, the combination of large existing EV battery capacity, targeted gigafactory plans, and supportive policy frameworks suggests a clear and structured pathway toward commercialization. Over the coming years, Europe is well-positioned to gradually integrate solid-state batteries into its EV ecosystem, strengthening its role in the global battery value chain.

Europe Solid State Battery Market Recent Developments:

- January 2026: Syensqo and Axens announced the launch of Argylium, a new company focused on developing and scaling advanced materials for solid-state batteries in Europe. The initiative aims to accelerate the industrialization of next-generation sulfide solid electrolytes, supporting the commercialization of all-solid-state battery technologies and strengthening Europe’s battery innovation ecosystem.

- September 2025: Volkswagen Group, together with its subsidiaries PowerCo and Elli, showcased advanced battery and energy technologies at IAA Mobility 2025, including a prototype test vehicle equipped with a solid-state battery, highlighting progress toward next-generation battery technologies and reinforcing Europe’s efforts to accelerate solid-state battery development.

- May 2024: ProLogium officially announced the opening of its first overseas R&D center in Paris-Saclay, France, specifically to support solid-state battery technology tailored for the European market.

Europe Solid State Battery Market Scope:

| Category | Segments |

|---|---|

| By Type | Thin Film Battery, Portable Battery), |

| By Capacity | Below 20 mAh, 20 mAh - 500 mAh, Above 500 mAh), |

| By Cell Type | Single-Cell Battery, Multi-Cell Battery), |

| By Application | Consumer Electronics, Electric Vehicles, Medical Devices, Wearables, Energy Harvesting, Wireless Sensors, Others), and others |

Europe Solid State Battery Market Driver:

Increasing Government Funding & Strategic Industrial Policy Support

Government-led sustainability policies, climate strategies, and direct public investments are central drivers accelerating Europe’s Solid-State Battery Market, as governments align decarbonization goals with industrial competitiveness and energy security.

For instance, France’s “France 2030” investment plan commits around USD58.3 billion, with a strong focus on decarbonized transport and advanced battery technologies. By supporting next-generation batteries with higher safety and energy density, France aims to strengthen domestic battery manufacturing while cutting transport-related CO₂ emissions and reducing reliance on imported technologies.

Similarly, in 2023, the UK government has committed over USD2.5 billion through its Automotive Transformation Fund, targeting battery manufacturing and next-generation technologies as part of its legally binding net-zero-by-2050 objective. Solid-state batteries are positioned as a future solution to improve EV range, safety, and sustainability.

Likewise, in 2023, Italy’s National Recovery and Resilience Plan (PNRR) allocates more than EUR 20 billion to green transition measures, including sustainable mobility and energy storage, while in 2024, Spain’s PERTE VEC program mobilizes over USD1.5 billion to build a competitive EV and battery ecosystem. These rising investments, along with government policies, are significantly driving the market growth.

Europe Solid State Battery Market Trend:

Transition from Laboratory R&D to Pilot-Scale Manufacturing

The European Solid-State Battery Market is increasingly defined by a shift from laboratory research toward pilot-scale and pre-industrial manufacturing, as policymakers and industry focus on commercialization readiness. This transition is strongly evidenced by the European Commission and publicly funded research initiatives.

For instance, the European Commission’s Joint Research Centre (JRC) classifies solid-state batteries as being at a pre-industrial or early pilot scale, emphasizing that current efforts are centered on process optimization, scale-up, and manufacturability, rather than basic materials research. This marks a clear move away from lab-only development.

Additionally, EU battery policy and funding priorities increasingly support pilot infrastructure. Under EU industrial and innovation programs, funding is directed toward pilot lines, validation facilities, and industrial testing environments, reflecting the need to de-risk future gigafactories before large capital commitments. The European Commission explicitly highlights pilot manufacturing as a critical bridge between research and commercialization.

Europe Solid State Battery Market Challenges:

High Cost & Manufacturing Scale Challenges Impeding Market Growth

The most critical challenge in the European Solid-State Battery Market is scaling manufacturing while reducing costs to levels suitable for mass adoption, particularly in automotive and grid-storage applications. For instance, solid-state batteries remain at a “pre-industrial or early pilot scale,” with yields and process stability still far below mature lithium-ion production.

Additionally, conventional lithium-ion gigafactories in Europe typically achieve cell yields with a major fraction, whereas solid-state pilot lines remain well below this level, driving higher scrap rates and costs.

Similarly, cost competitiveness remains a major hurdle. European automotive OEMs and EU transport policy documents commonly cite around USD100 per kWh at pack level as the threshold for mass-market EV adoption, a level that solid-state batteries in Europe have not yet reached due to costly solid electrolytes, lithium-metal processing, and low throughput.

Europe Solid State Battery Market (2026-32) Segmentation Analysis:

The Europe Solid State Battery Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Cell Type

- Single-Cell Battery

- Multi-Cell Battery

Multi-cell battery architectures dominate this market, accounting for 56% market share, because they are the only practical format for automotive, aerospace, and grid-scale applications, which represent Europe’s primary demand centers. Unlike single-cell designs, multi-cell solid-state batteries enable higher voltage, scalable energy capacity, and system-level safety compliance, aligning with European industrial requirements.

For instance, the European automotive sector requires battery packs operating above 400V, a threshold that can only be achieved by connecting dozens to hundreds of cells in series, according to vehicle safety and performance standards referenced by the European Commission’s transport and mobility framework. Additionally, the EU’s Battery Regulation (EU 2023/1542) emphasizes lifecycle safety, traceability, and modularity, all of which favor multi-cell configurations that allow monitoring, redundancy, and thermal management.

Similarly, European solid-state battery manufacturers such as Blue Solutions and ProLogium Europe focus on multi-cell modules rather than single cells, as their primary customers include electric buses, passenger vehicles, and energy-storage operators. These are contributing to the dominance of the Multi-Cell Battery in this market.

Based on Application

- Consumer Electronics

- Electric Vehicles

- Medical Devices

- Wearables

- Energy Harvesting

- Wireless Sensors

- Others

Electric vehicles (EVs) represent the dominant application segment in this market, accounting for about 40% market share, driven by regulatory pressure, automotive electrification targets, and large-scale OEM investment priorities. This dominance is evident from policy direction, deployment volumes, and funding allocation, rather than market-research estimates.

For instance, the European Commission’s “Fit for 55” package mandates a 100% reduction in CO₂ emissions from new passenger cars by 2035, effectively accelerating the shift toward battery-electric vehicles and intensifying demand for next-generation batteries such as solid-state systems. Additionally, the European Automobile Manufacturers’ Association (ACEA) reported that battery-electric vehicles accounted for over 14% of new car registrations in the EU in 2023, underscoring the scale of EV adoption already underway.

Similarly, major European automotive OEMs, including Volkswagen, BMW, and Mercedes-Benz, have publicly stated that solid-state batteries are primarily being developed for future EV platforms, due to their potential for higher energy density, improved safety, and longer driving range. For reference, EV battery packs typically require high-voltage, multi-cell architectures, making them the most suitable and commercially relevant application for solid-state technology.

Europe Solid State Battery Market (2026-32): Regional Projection

Germany holds a dominant position in this market, accounting for about 19% market share, driven by its strong industrial base, public funding, and automotive leadership. This dominance is based on concrete manufacturing infrastructure, pilot production, and sustained government-backed initiatives.

For instance, as of 2024, as per the German Federal Government, in the last 15 years, Germany has invested well over USD1.08 billion in battery research. With a significant share directed toward solid-state and next-generation battery technologies. These funds support pilot lines, scale-up facilities, and industry–research collaboration across Germany.

Additionally, Germany’s automotive ecosystem strongly reinforces this position. Major OEMs such as Volkswagen, BMW, and Mercedes-Benz are deeply engaged in solid-state battery validation through domestic pilot programs, prototype integration, and long-term industrialization roadmaps. German battery specialists such as Volkswagen Group Components have already entered solid-state cells at pilot scale for aerospace, defense, and premium mobility applications. These factors are contributing to the dominance of Germany in this market.

Gain a Competitive Edge with Our Europe Solid State Battery Market Report

- Europe Solid State Battery Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Europe Solid State Battery Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Solid State Battery Market Regulations, Policies & Standards

- Europe Solid State Battery Market Trends & Developments

- Europe Solid State Battery Market Dynamics

- Growth Drivers

- Challenges

- Europe Solid State Battery Market Hotspots & Opportunities

- Europe Solid State Battery Market Supply Chain Analysis

- Europe Solid State Battery Market Pricing Analysis

- Europe Solid State Battery Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Type- (USD Million)

- Thin Film Battery

- Portable Battery

- By Capacity- (USD Million)

- Below 20 mAh

- 20 mAh - 500 mAh

- Above 500 mAh

- By Cell Type- (USD Million)

- Single-Cell Battery

- Multi-Cell Battery

- By Application- (USD Million)

- Consumer Electronics

- Electric Vehicles

- Medical Devices

- Wearables

- Energy Harvesting

- Wireless Sensors

- Others

- By Country

- Germany

- UK

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type- (USD Million)

- Market Size & Analysis

- Germany Solid State Battery Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Type- (USD Million)

- By Capacity- (USD Million)

- By Cell Type- (USD Million)

- By Application- (USD Million)

- Market Size & Analysis

- UK Solid State Battery Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Type- (USD Million)

- By Capacity- (USD Million)

- By Cell Type- (USD Million)

- By Application- (USD Million)

- Market Size & Analysis

- France Solid State Battery Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Type- (USD Million)

- By Capacity- (USD Million)

- By Cell Type- (USD Million)

- By Application- (USD Million)

- Market Size & Analysis

- Italy Solid State Battery Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Type- (USD Million)

- By Capacity- (USD Million)

- By Cell Type- (USD Million)

- By Application- (USD Million)

- Market Size & Analysis

- Spain Solid State Battery Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Type- (USD Million)

- By Capacity- (USD Million)

- By Cell Type- (USD Million)

- By Application- (USD Million)

- Market Size & Analysis

- Netherlands Solid State Battery Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Type- (USD Million)

- By Capacity- (USD Million)

- By Cell Type- (USD Million)

- By Application- (USD Million)

- Market Size & Analysis

- Russia Solid State Battery Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Type- (USD Million)

- By Capacity- (USD Million)

- By Cell Type- (USD Million)

- By Application- (USD Million)

- Market Size & Analysis

- Europe Solid State Battery Market Key Strategic Imperatives for Growth & Success

- Competitive Outlook

- Company Profiles

- Blue Solutions

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Basquevolt

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Ilika

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- SOLiTHOR

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- ProLogium Europe

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Blue Solutions

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now