Saudi Arabia Medical Consumables Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Healthcare Settings (Hospitals (General Hospitals, Specialty Hospitals, Multispecialty Hospitals), Specialty Clinics, Others), By Usage (Surgical, Non-Surgical), By Division (Ex ... am Gloves, Surgeons’ Gloves, Diagnostics Consumables, O.R. Consumables (non-glove), Anaesthesia Consumables, Advanced Wound Care, Vascular Access, Laboratory Consumables, Respiratory Consumables, EVS / Infection Control, Personal Protection (non-glove PPE), Urology, Personal Care, Primary + Preventive Care, SPT, Ready Care, Rehab & Fall Prevention, Medline Textiles, Others / Misc.), By Clinical Specialties (Cardiology, Gynecology, Urology, Orthopedics and Trauma, General Surgery and Laparoscopic Surgery, Nephrology and Dialysis, Oncology Medical and Surgical, Respiratory and Pulmonology, Gastroenterology, Vascular Surgery and Endovascular Procedures, Anesthesiology and Perioperative Care, Others), By Material (Disposable, Non-Disposable), and others Read more

- Healthcare

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

Saudi Arabia Medical Consumables Market

Projected 4.87% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 1.26 Billion

Market Size (2032)

USD 2.23 Billion

Base Year

2025

Projected CAGR

4.87%

Leading Segments

By Material: Disposable

Saudi Arabia Medical Consumables Market Report Key Takeaways:

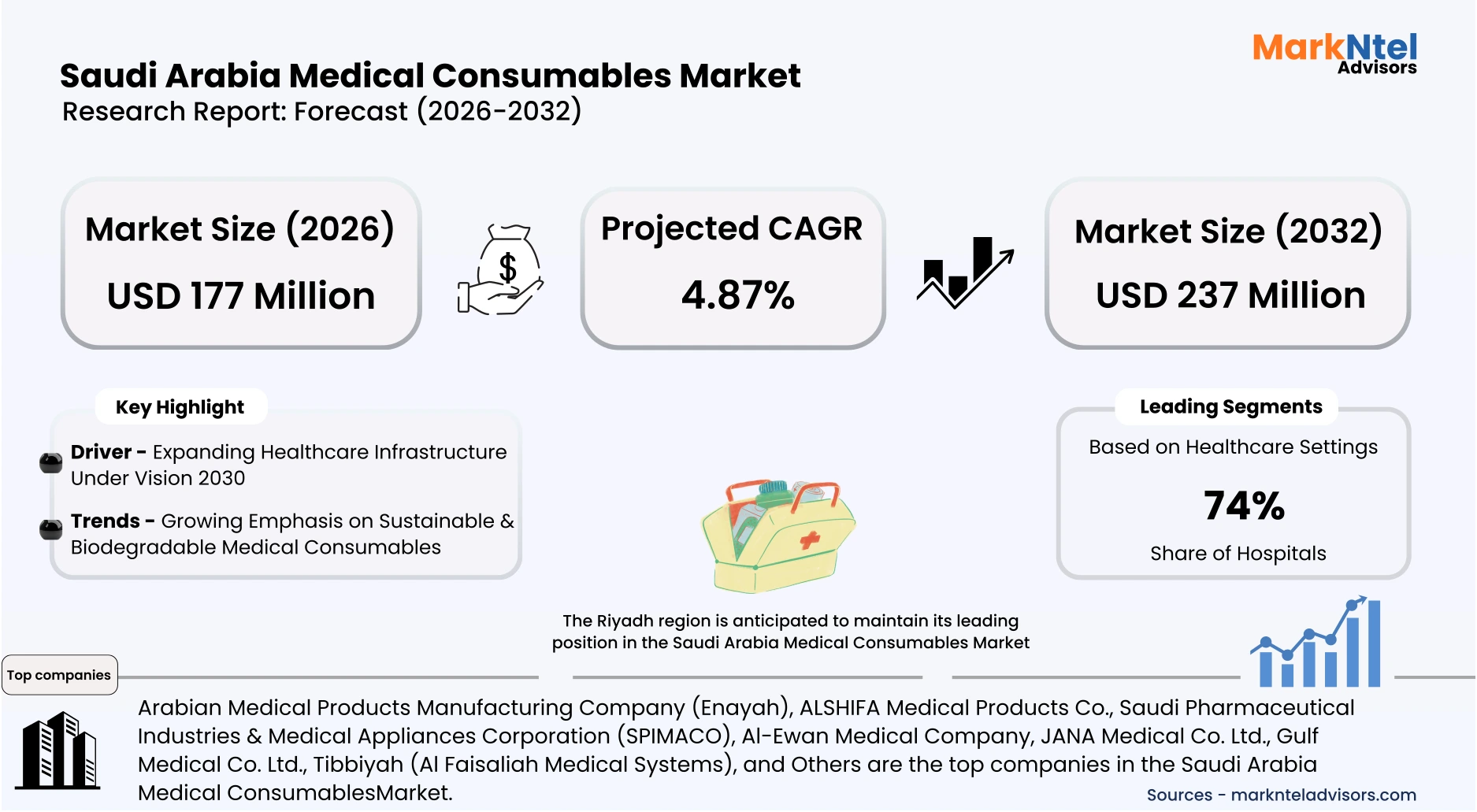

- Saudi Arabia Medical Consumables Market: USD 1.1 Billion in 2025, USD 1.26 Billion in 2026 and USD 2.23 Billion By 2032. The estimated CAGR from 2026 to 2032 is around 4.87%, indicating strong growth.

- By Healthcare Settings, the Hospitals segment represented a significant share of about 74% in the Saudi Arabia Medical Consumables Market in 2026.

- By material, the disposable segment presented a significant share of about 85% in the Saudi Arabia Medical Consumables Market in 2026.

- Leading Saudi Arabia Medical Consumables Companies in the Saudi Arabia are Arabian Medical Products Manufacturing Company (Enayah), ALSHIFA Medical Products Co., Saudi Pharmaceutical Industries & Medical Appliances Corporation (SPIMACO), DISPRO (Saudi Disposable Hygienic Products Co.), Al-Jeel Medical and Trading Co., National Medical Products Co., Al-Ewan Medical Company, JANA Medical Co. Ltd., Gulf Medical Co. Ltd., Tibbiyah (Al Faisaliah Medical Systems), and Others.

Market Insights & Analysis: Saudi Arabia Medical Consumables Market (2026-32):

The Saudi Arabia Medical Consumables Market size is estimated at USD 1.1 Billion in 2025, USD 1.26 Billion in 2026 and USD 2.23 Billion By 2032. Along with this, the market is estimated to grow at a CAGR of around 4.87% during the forecast period, i.e., 2026-32.

Saudi Arabia’s healthcare system is experiencing structural expansion that underpins robust demand for medical consumables across institutional settings. The Ministry of Health reported that its budget accounted for USD28 billion of health and social development spending in 2023 and is projected to remain a top fiscal priority in 2025 , reflecting sustained public expenditure on services and facilities. This fiscal emphasis supports recurrent consumption of single-use items such as syringes, IV sets, and wound care supplies in hospitals and clinics across the Kingdom.

Institutional capacity expansion reinforces baseline consumables utilization. According to the General Authority for Statistics Healthcare Establishments and Workforce Statistics 2024, the Kingdom had 516 hospitals, with the highest concentration in Riyadh, and 23.4 hospital beds per 10,000 individuals, indicating broad inpatient service capacity. Combined with 36.8 physicians per 10,000 population, these structural resources support extensive procedural throughput that drives routine demand for medical consumables in surgical, emergency, and general care workflows.

Chronic disease prevalence further elevates consumables usage intensity. The 2024 Health Status Statistics Bulletin reported that 18.95 % of adults aged 15 and above have at least one chronic condition, including diabetes and hypertension, which require frequent clinical interventions and follow-up care, inherently increasing usage of diagnostic and therapeutic disposables. Consumables such as diagnostic test kits, catheters, and infection control materials are routinely consumed as part of chronic disease management protocols across outpatient and inpatient settings.

Beyond demand drivers, healthcare infrastructure modernisation under national reforms improves supply chain predictability and procurement efficiency. Vision 2030 reforms and related healthcare projects, e.g., large-scale hospital expansions and speciality centres, aim to reduce capacity gaps and broaden service coverage. The Saudi Healthcare Sector 2025 overview notes a target to add approximately 27,000 additional hospital beds by 2030 to meet rising demand, which will structurally increase institutional consumables requirements across regions over time.

Saudi Arabia Medical Consumables Market Recent Developments:

- 2025: The Saudi Food and Drug Authority (SFDA) granted marketing authorization for a fully Saudi-developed surgical tool that improves the safety and efficiency of surgical procedures. It is a hand-worn device with a magnetic holder that secures suture needles during operations, reducing risk of accidental needle injuries and improving ergonomic use of consumables like suturing kits. This invention is patented in Saudi Arabia and the U.S. and is locally manufactured.

- 2026:Professional Medical Expertise Co. (ProMedEx) signed a Memorandum of Understanding (MoU) with Zhende Medical Co. Ltd and MedSurg FZ-LLC to establish a joint venture (JV) in Saudi Arabia to manufacture medical supplies and consumables for the Kingdom and the wider GCC/Middle East market.

Saudi Arabia Medical Consumables Market Scope:

| Category | Segments |

|---|---|

| By Healthcare Settings | (Hospitals (General Hospitals, Specialty Hospitals, Multispecialty Hospitals), Specialty Clinics, Others), |

| By Usage | (Surgical, Non-Surgical), |

| By Division | (Exam Gloves, Surgeons’ Gloves, Diagnostics Consumables, O.R. Consumables (non-glove), Anaesthesia Consumables, Advanced Wound Care, Vascular Access, Laboratory Consumables, Respiratory Consumables, EVS / Infection Control, Personal Protection (non-glove PPE), Urology, Personal Care, Primary + Preventive Care, SPT, Ready Care, Rehab & Fall Prevention, Medline Textiles, Others / Misc.), |

| By Clinical Specialties | (Cardiology, Gynecology, Urology, Orthopedics and Trauma, General Surgery and Laparoscopic Surgery, Nephrology and Dialysis, Oncology Medical and Surgical, Respiratory and Pulmonology, Gastroenterology, Vascular Surgery and Endovascular Procedures, Anesthesiology and Perioperative Care, Others), |

| By Material | (Disposable, Non-Disposable), |

Saudi Arabia Medical Consumables Market Driver:

Expanding Healthcare Infrastructure Under Vision 2030

The primary driver accelerating growth in the Saudi Arabia Medical Consumables Market is the continued expansion and modernisation of healthcare infrastructure under Vision 2030 reforms. The government has prioritised healthcare accessibility and quality improvement as a core transformation objective, resulting in large-scale hospital development, capacity upgrades, and service decentralisation across regions.

According to the Ministry of Health (MoH) and the General Authority for Statistics (GASTAT), Saudi Arabia had 516 hospitals and more than 23 hospital beds per 10,000 population as of the latest healthcare establishment statistics. Ongoing infrastructure projects continue to add new facilities and speciality centres, increasing inpatient admissions, surgical volumes, and diagnostic procedures nationwide.

Further, the Ministry of Health announced multiple hospital expansions and new project inaugurations in 2025, adding thousands of beds and specialised service units as part of Vision 2030 healthcare transformation initiatives. These projects are designed to enhance regional healthcare coverage and reduce capacity gaps.

In parallel, government budget allocations reinforce this structural expansion. The Ministry of Health Budget confirms sustained annual funding support for healthcare development programs, infrastructure upgrades, and procurement modernisation. Stable public financing enhances institutional purchasing of essential consumables such as syringes, IV sets, surgical gloves, catheters, wound care products, and diagnostic disposables.

As hospital capacity increases and service penetration expands beyond major urban centres, procedural volumes rise correspondingly. Each inpatient admission, surgical intervention, emergency visit, and chronic disease consultation directly translates into recurring consumption of disposable medical supplies. Consequently, healthcare infrastructure growth structurally elevates baseline demand for medical consumables, ensuring sustained market expansion throughout the forecast period.

Saudi Arabia Medical Consumables Market Trend:

Growing Emphasis on Sustainable & Biodegradable Medical Consumables

A notable trend influencing the Saudi Arabia Medical Consumables Market is the increasing institutional focus on environmental sustainability and medical waste reduction. Healthcare facilities across the Kingdom are strengthening waste segregation, recycling, and environmentally responsible disposal practices in alignment with national sustainability objectives and the Saudi Green Initiative. Reports indicate that hospitals are promoting the use of biodegradable materials and reducing reliance on non-recyclable plastics within clinical environments

The Ministry of Health’s expanded medical waste management initiatives and public- private contracts for environmentally compliant waste handling further reinforce sustainability priorities within healthcare operations. In 2025, companies secured MoH projects centred on regulated medical waste treatment, reflecting structured investments in cleaner healthcare systems. These initiatives create indirect demand for consumables that are easier to dispose of, recyclable, or biodegradable.

As sustainability metrics become integrated into procurement and hospital accreditation standards, suppliers offering eco-friendly medical consumables, including biodegradable waste bags, compostable packaging, and reduced-plastic sterile products, are likely to gain a competitive advantage. While adoption remains gradual, environmental compliance and waste reduction objectives are increasingly shaping purchasing decisions within the Saudi healthcare ecosystem.

Saudi Arabia Medical Consumables Market Opportunity:

Expansion of Private Sector Participation & Health Insurance Coverage

A significant growth opportunity in the Saudi Arabia Medical Consumables Market stems from the expanding role of the private healthcare sector under the Kingdom’s healthcare transformation agenda. The government is actively promoting greater private sector participation in healthcare delivery and financing to reduce pressure on public facilities, improve operational efficiency, and enhance service quality across regions.

According to the Health Sector Transformation Program, one of the key strategic objectives is to increase private sector contribution through public–private partnerships (PPPs), corporatization of public hospitals, and increased private investment in specialized care facilities. This structural shift is expected to drive higher procedural volumes in private hospitals and day-surgery centers, thereby accelerating demand for high-frequency medical consumables such as surgical disposables, IV supplies, and diagnostic kits.

Additionally, rising health insurance penetration further amplifies this opportunity. The Council of Health Insurance (CHI) regulates mandatory employer-provided health insurance under the Cooperative Health Insurance Law and actively enforces compliance by monitoring coverage and penalising non-compliant employers, as seen in a 2025 action where 110 firms were fined ~USD 666,000 for failing to insure workers and dependents. By expanding insured populations, including private sector employees and their families, CHI’s regulatory actions improve affordability for elective procedures and preventive care, thereby increasing patient footfall and procedural volumes in private hospitals.

Moreover, demographic and epidemiological shifts create long-term opportunity pockets in high-frequency consumables segments. According to the World Health Organisation (WHO), noncommunicable diseases account for approximately 73% of total deaths in Saudi Arabia, necessitating continuous monitoring, repeated clinical visits, and procedural interventions, all of which require recurring disposable medical supplies.

Furthermore, ongoing digital transformation and centralised procurement reforms within Saudi Arabia’s healthcare system are strengthening supply chain efficiency for medical consumables across public health clusters. The Ministry of Health, through unified electronic procurement platforms and cluster-based governance models, has stream lined tendering processes, enhanced inventory tracking, and improved demand forecasting for high-volume consumables such as syringes, surgical gloves, IV sets, and wound care products.

This centralised purchasing framework increases transparency and volume aggregation, creating structured opportunities for domestic manufacturers and international suppliers to participate in standardised tenders and long-term supply contracts for essential disposable medical products.

Saudi Arabia Medical Consumables Market Challenge:

Regulatory Compliance Burden Under SFDA Medical Device Framework

A primary structural barrier in the Saudi Arabia medical consumables market is the stringent regulatory framework administered by the Saudi Food and Drug Authority (SFDA). Under the Medical Devices Law and its Implementing Regulations, all medical consumables must undergo product listing, conformity assessment, and establishment licensing prior to commercialization. The SFDA requires compliance with the Medical Device Marketing Authorization (MDMA) process, technical documentation review, and quality management system certification. These requirements have intensified following recent enforcement updates aimed at strengthening patient safety and supply chain traceability.

The compliance process involves mandatory registration on the GHAD system, submission of safety and performance evidence, and payment of regulatory fees denominated in USD equivalent value. According to the SFDA Medical Devices Interim Regulation and 2025 guidance updates, failure to obtain proper authorization can result in product seizure, fines, and suspension of import privileges. Public enforcement announcements demonstrate periodic penalties and recalls for non-compliant devices, reinforcing regulatory scrutiny. These procedural and documentation requirements increase administrative timelines and operational costs for manufacturers and distributors.

This regulatory burden materially restricts market entry and scalability, particularly for small and mid-sized suppliers lacking local regulatory expertise. Extended approval timelines delay product launches and limit responsiveness to hospital tenders under centralized procurement frameworks. Compliance costs also reduce margin flexibility in a price-sensitive, volume-driven consumables market. Consequently, regulatory complexity remains a systemic constraint that influences investment decisions and competitive positioning across the sector.

Saudi Arabia Medical Consumables Market (2026-32) Segmentation Analysis:

The Saudi Arabia Medical Consumables Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Healthcare Settings:

- Hospitals

- General Hospitals

- Specialty Hospitals

- Multispecialty Hospitals

- Specialty Clinics

- Others

Hospitals dominate the Saudi Arabia Medical Consumables Market with market share of around 74% due to their structural role in handling the highest volume of inpatient admissions and complex interventions. According to the Ministry of Health Statistical Yearbook 2024, hospitals account for the overwhelming majority of inpatient discharges and surgical procedures nationwide, directly translating into recurring consumption of sterile disposables. The concentration of intensive care units, operating theaters, and emergency departments within hospital facilities further elevates high-frequency utilization of gloves, syringes, and wound care products.

Government capital expenditure on hospital capacity expansion under the 2025 national budget allocation for health and social development has strengthened institutional procurement volumes. Large tertiary and multispecialty hospitals perform advanced cardiovascular, oncology, and transplant procedures, each associated with higher consumables usage per case compared to outpatient settings. Institutional accreditation standards and mandatory quality reporting frameworks also require consistent replenishment of certified medical supplies.

Moreover, public hospitals remain the primary recipients of state-funded treatment programs and referral-based care pathways, concentrating demand within centralized facilities. Bulk procurement contracts and framework agreements negotiated at institutional levels reinforce purchasing scale advantages. These structural demand concentrations, combined with procedural intensity and formalized procurement systems, collectively sustain hospital leadership within the healthcare settings segmentation.

Based on Material:

- Disposable

- Non-Disposable

The dominance of disposable materials in the Saudi Arabia Medical Consumables Market is reinforced by official infection prevention and safety protocols that require single-use items to be discarded after one patient use. This segment holds a substantial market share, around 85%. The Ministry of Health’s National Guide for Auditors in Infection Control mandates that single-use devices such as syringes, needles, and wound kits must not be reprocessed or reused, reducing cross-infection risk and increasing recurring consumption of disposables. The Saudi Food and Drug Authority evaluation of facility compliance further emphasizes that hospitals must develop and follow policies preventing reuse of single-use devices, highlighting the regulatory emphasis on disposable consumables in clinical practice.

For instance, during the 2025 Hajj season, the Saudi Ministry of Health reported that its healthcare system delivered over 102,000 medical services, with 27,231 emergency cases, 4,970 hospital admissions, and more than 200 cardiac catheterisations and open-heart surgeries by the 8th of Dhul Hajjah. These high volumes of clinical activity directly require extensive use of medical consumables including syringes, IV sets, protective apparel, catheter kits, and procedure-specific disposables across hospitals and emergency departments, demonstrating real procedural demand that structures consumables turnover.

Additionally, domestic manufacturers have expanded production of plastic-based disposable consumables within industrial zones, improving supply continuity and cost competitiveness. Shorter procurement cycles and predictable replacement frequency further enhance disposable volume stability. These operational, regulatory, and manufacturing dynamics collectively position disposable materials as the dominant segment in Saudi Arabia’s medical consumables market.

Saudi Arabia Medical Consumables Market (2026-32) Regional Analysis:

The Riyadh region is anticipated to maintain its leading position in the Saudi Arabia Medical Consumables Market through 2032, primarily due to its dense concentration of advanced healthcare infrastructure. Riyadh accounts for more than 20,000 hospital beds approximately 20,457 beds, representing the highest absolute bed capacity among all regions in Saudi Arabia. The region serves a population exceeding 8 million residents, reinforcing its position as the Kingdom’s largest healthcare service hub in terms of infrastructure and inpatient capacity. This large inpatient base structurally translates into higher recurring consumption of IV sets, syringes, surgical drapes, wound dressings, and catheter kits per admission compared to other regions.

In addition, Riyadh is home to nationally specialised tertiary centres such as King Faisal Specialist Hospital & Research Centre, which performs advanced oncology treatments, organ transplants, and complex cardiovascular procedures. Transplant surgeries and cardiac interventions require extensive use of sterile, single-use surgical kits, perfusion disposables, anaesthesia circuits, and post-operative ICU consumables. Similarly, King Saud Medical City, one of the largest medical cities in the Riyadh, manages high trauma and emergency volumes annually, reinforcing sustained turnover of emergency department disposables and critical care supplies.

Furthermore, Riyadh Health Clusters collectively serve millions of beneficiaries across dozens of hospitals and primary care centres, creating continuous inpatient and outpatient procedural flow. The combination of the Kingdom’s largest hospital bed base, concentration of specialised referral centres, and high-acuity case mix structurally positions Riyadh as the primary demand hub for medical consumables nationwide.

Gain a Competitive Edge with Our Saudi Arabia Medical Consumables Market Report:

- The Saudi Arabia Medical Consumables Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Saudi Arabia Medical Consumables Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Saudi Arabia Medical Consumables Market Policies, Regulations, and Product Standards

- Saudi Arabia Medical Consumables Market Trends & Developments

- Saudi Arabia Medical Consumables Market Dynamics

- Growth Factors

- Challenges

- Saudi Arabia Medical Consumables Market Hotspot & Opportunities

- Saudi Arabia Medical Consumables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- Hospitals

- General Hospitals

- Specialty Hospitals

- Multispecialty Hospitals

- Specialty Clinics

- Others

- Hospitals

- By Usage- Market Size & Forecast 2022-2032, USD Million

- Surgical

- Non-Surgical

- By Division- Market Size & Forecast 2022-2032, USD Million

- Exam Gloves

- Surgeons’ Gloves

- Diagnostics Consumables

- O.R. Consumables (non-glove)

- Anaesthesia Consumables

- Advanced Wound Care

- Vascular Access

- Laboratory Consumables

- Respiratory Consumables

- EVS / Infection Control

- Personal Protection (non-glove PPE)

- Urology

- Personal Care

- Primary + Preventive Care

- SPT

- Ready Care

- Rehab & Fall Prevention

- Medline Textiles

- Others / Misc.

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- Cardiology

- Gynecology

- Urology

- Orthopedics and Trauma

- General Surgery and Laparoscopic Surgery

- Nephrology and Dialysis

- Oncology Medical and Surgical

- Respiratory and Pulmonology

- Gastroenterology

- Vascular Surgery and Endovascular Procedures

- Anesthesiology and Perioperative Care

- Others

- By Material- Market Size & Forecast 2022-2032, USD Million

- Disposable

- Non-Disposable

- By Region- Market Size & Forecast 2022-2032, USD Million

- Riyadh

- Makkah

- Eastern Province (Ash-Sharqiyah)

- Madinah

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Disposable Medical Consumables Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Non-Disposable Medical Consumables Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Medical Consumables Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Arabian Medical Products Manufacturing Company (Enayah)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ALSHIFA Medical Products Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saudi Pharmaceutical Industries & Medical Appliances Corporation (SPIMACO)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DISPRO (Saudi Disposable Hygienic Products Co.)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al-Jeel Medical and Trading Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- National Medical Products Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al-Ewan Medical Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- JANA Medical Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gulf Medical Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tibbiyah (Al Faisaliah Medical Systems)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arabian Medical Products Manufacturing Company (Enayah)

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now