Saudi Arabia Flame Retardants Market Research Report: Growth Drivers & Forecast (2026-2032)

By Compound (Inorganic, Phosphorus-based, Halogenated (chlorinated or brominated), Organic (containing nitrogen or other hetero elements)), By Application (Plastics and polymers, T ... extile, Wire and cable, Coating and sealant, Adhesive and composite), By End-User (Building and construction, Electrical and electronics, Automotive and transportation, Consumer goods, Industrial and manufacturing), and others Read more

- Chemicals

- Mar 2026

- Pages 165

- Report Format: PDF, Excel, PPT

Saudi Arabia Flame Retardants Market

Projected 11.21% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 185 Million

Market Size (2032)

USD 350 Million

Base Year

2025

Projected CAGR

11.21%

Leading Segments

By Application: Plastics & polymers

Saudi Arabia Flame Retardants Market Report Key Takeaways:

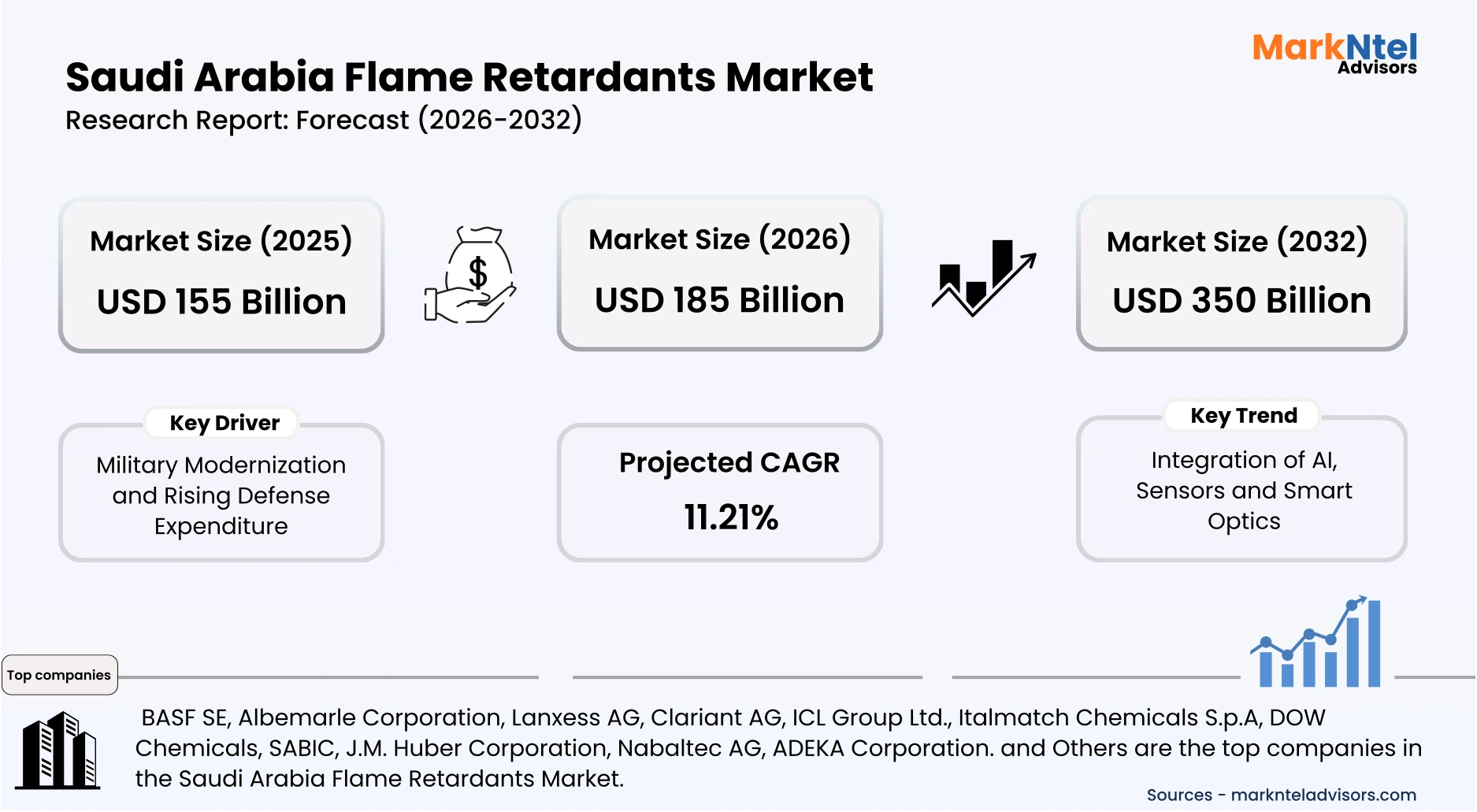

- The Saudi Arabia Flame Retardants Market size was valued at around USD 155 million in 2025 and is projected to grow from USD 185 million in 2026 to USD 350 million by 2032, exhibiting a CAGR of 11.21% during the forecast period.

- The Central region is the leading region with a significant share of around 40% in 2026.

- By End user, the building and construction segment represented a significant share of about 38 % in the Saudi Arabia Flame Retardants Market in 2026.

- By Application, the Plastics and polymers segment presented a significant share of about 32% in the Saudi Arabia Flame Retardants Market in 2026.

- Leading flame retardants companies are BASF SE, Albemarle Corporation, Lanxess AG, Clariant AG, ICL Group Ltd., Italmatch Chemicals S.p.A, DOW Chemicals, SABIC, J.M. Huber Corporation, Nabaltec AG, ADEKA Corporation. and Others.

Market Insights & Analysis: Saudi Arabia Flame Retardants Market (2026-32):

The Saudi Arabia Flame Retardants Market size was valued at around USD 155 million in 2025 and is projected to grow from USD 185 million in 2026 to USD 350 million by 2032, exhibiting a CAGR of 11.21% during the forecast period. i.e., 2026-32.

Saudi Arabia flame retardants industry has grown steadily in line with the Kingdom’s urban expansion and industrial diversification. Industrial modernization, including chemical and petrochemical plants in the Eastern Region, has further stimulated the consumption of specialized flame retardants to meet workplace safety standards. Population growth and urbanization in major cities such as Riyadh and Jeddah have reinforced residential construction demand, amplifying the need for compliant building materials.

Regulatory developments continue to shape market dynamics. The Saudi Building Code (SBC) 2025 update mandates enhanced fire resistance standards for polymers, coatings, and insulation used in new constructions, while the Saudi Fire Code (SFC) reinforces emergency preparedness and material compliance across commercial and industrial facilities. Simultaneously, the Civil Defence Authority has increased inspections of high-risk buildings, effectively driving manufacturers to adopt certified flame-retardant additives. The Ministry of Municipality and Rural Affairs’ guidelines for public infrastructure projects emphasize fire safety in material selection, providing a direct regulatory stimulus for flame-retardant adoption.

End-user demand patterns vary across sectors, with residential and commercial construction representing the largest consumers of flame-retardant plastics and composite materials. Industrial facilities, particularly in the petrochemical, energy, and logistics sectors, require specialised flame-retardant coatings and adhesives to safeguard equipment and maintain compliance with occupational safety regulations. Institutional projects, such as universities and hospitals, have introduced stricter procurement requirements for fire-resistant products, further sustaining demand. Urban planning initiatives under Vision 2030, including new mixed-use developments in the Central Region, have heightened integration of safety-compliant materials early in the construction lifecycle.

Private and public initiatives complement regulatory drivers, supporting market expansion through innovation and technology adoption. In 2025, the National Industrial Development and Logistics Program (NIDLP) promoted localization of high-performance chemical additives, encouraging domestic production of flame retardants. Collaborative training programs between the Saudi Standards, Metrology and Quality Organization (SASO) and industrial stakeholders improved testing and certification capabilities for fire-resistant materials . Leading chemical companies have introduced halogen-free phosphorus-based solutions, aligning with environmental and safety regulations while advancing sustainability objectives. These measures collectively underpin a positive outlook for the market through 2032.

Saudi Arabia Flame Retardants Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Fruit Juice (Fresh Juice, Fortified Juice, Fruit Nectars (High Concentration (40%–50% fruit content), Medium Concentration (30%–39% fruit content), Low Concentration (25%–29% fruit content))), Vegetable Juice, Fruit and Vegetable Blends), |

| By Source | (Not from Concentrate (NFC), From Concentrate (FC)), |

| By Packaging | (Cartons (Tetra Pak) (Single-Serve Packs, Family Packs), PET Bottles (Small-Size Bottles, Large-Size Bottles), Glass Bottles, Cans, Others), |

| By Distribution Channel | (Off-Trade (Retail) (Supermarkets & Hypermarkets, Convenience Stores, Traditional Grocery), On-Trade (HoReCa) (Hotels, Restaurants & Cafes), Online Retail), |

| By End User | (Household, Hotels, Restaurants, and Cafes (HoReCa), Institutional, Industrial), |

| By Region | (UAE, Saudi Arabia, Oman, Qatar, Kuwait, Bahrain) |

Saudi Arabia Flame Retardants Market Driver:

Infrastructure Development and Automotive Industry Growth

The expansion of construction and automotive manufacturing activities has become a significant structural driver, increasing demand for flame-retardant materials in Saudi Arabia. Construction activity continues to rise due to strong public infrastructure spending and private real estate development linked to the national diversification agenda. Government data indicate that the sector is projected to grow by about 4.4% in 2025 , supported by the national budget allocation for public expenditure, including infrastructure and development programs. Such large-scale development requires fire-resistant materials in electrical installations, insulation systems, and polymer-based building components, directly increasing the consumption of flame-retardant additives.

The housing and urban development segment further intensifies this demand by expanding residential construction across major cities. Under national housing initiatives, the government has launched programs to deliver over 40,000 new housing units across 24 residential projects in 2025, while also targeting an increase in homeownership to 70% by 2030. These projects require extensive use of polymer pipes, insulated wiring systems, and protective coatings, all of which incorporate flame-retardant compounds to comply with building safety standards. As residential, commercial, and mixed-use developments scale nationwide, the total volume of fire-resistant construction materials used in buildings continues to expand.

Automotive components, electrical connectors, and interior polymer parts increasingly require flame-retardant additives to meet international safety and performance standards. The simultaneous growth of construction, housing, and industrial production, therefore, generates sustained and measurable demand for flame-retardant materials across multiple end-use sectors in the Kingdom. Battery packs in electric and hybrid vehicles require fire-resistant materials because lithium-ion batteries can experience thermal runaway, which generates extremely high temperatures. Flame-retardant thermoplastics are therefore used in battery module housings, electrical enclosures, brackets, and insulation barriers surrounding battery cells.

Saudi Arabia Flame Retardants Market Trend:

Transition Toward Halogen-Free and Environmentally Safer Flame-Retardant Technologies

A significant structural trend shaping the Saudi Arabia flame retardants market is the growing transition toward halogen-free and environmentally safer flame-retardant technologies. This shift has accelerated in recent years due to increasing regulatory scrutiny over hazardous chemical substances used in construction materials, electrical equipment, and consumer products. The Saudi Standards, Metrology and Quality Organization (SASO) has strengthened technical regulations governing product safety and chemical compliance under the national Product Safety Law framework implemented in 2024–2025. These regulations require manufacturers to ensure that materials used in electrical appliances, cables, and building components meet strict safety and environmental standards.

This regulatory shift is transforming the value chain by encouraging manufacturers and chemical producers to develop advanced flame-retardant solutions that minimise toxic emissions during combustion. Companies supplying polymer additives are increasingly introducing phosphorus-based and nitrogen-based alternatives to traditional halogenated compounds, particularly for applications in wiring systems, insulation materials, and electronics housings. Saudi Basic Industries Corporation SABIC has publicly documented the development of halogen‑free flame‑retardant engineering thermoplastics tailored for electrical, automotive, and constru ction applications.

SABIC’s materials portfolio includes phosphorus‑based and nitrogen‑based flame‑retardant compounds designed to meet both safety and sustainability requirements in end‑use markets such as automotive electrical systems and building components.

These materials are used in wiring harnesses, connectors, and polymer housings where compliance with fire‑safety and environmental standards is essential. National industrial programs encourage domestic production of advanced speciality chemicals and materials that comply with global environmental standards. As international supply chains and export markets increasingly require compliance with stricter chemical regulations, manufacturers operating in the Kingdom are adopting halogen-free technologies to maintain competitiveness. This structural transition is expected to reshape product development strategies and sustain long-term demand for advanced flame-retardant formulations across multiple industries.

Saudi Arabia Flame Retardants Market Opportunity:

Leveraging Local Partnerships to Produce Sustainable Flame-Retardant Materials

Collaborating with established local manufacturers in Saudi Arabia presents a structural opportunity for new entrants in the flame-retardant market. Local industrial players often possess well-established production facilities, distribution networks, and experience navigating regulatory approvals under SASO and the Product Safety Law. By forming partnerships, emerging companies can leverage these capabilities to accelerate market entry, reduce capital expenditure, and ensure rapid compliance with fire-safety and environmental regulations. Such collaborations enable faster scaling of production for halogen-free or sustainable flame-retardant solutions tailored to construction, automotive, and electronics sectors.

Recent initiatives under Vision 2030 encourage industrial localisation partnerships and joint ventures, particularly in speciality chemicals and advanced materials. For instance, the Saudi Industrial Development Fund (SIDF) provides financing for projects involving collaborations between foreign technology providers and local manufacturers, with preferential loan terms and risk-sharing mechanisms. This framework reduces entry barriers and allows emerging players to access existing supply chains and distribution networks, directly translating into tangible market demand for flame-retardant compounds in high-volume applications like wiring insulation, polymer housings, and building materials.

Collaborations also foster technology transfer and knowledge sharing, enabling smaller companies to innovate in environmentally safer flame-retardant chemistries, such as phosphorus-based or nitrogen-based compounds. By combining local expertise with new formulations, entrants can differentiate their offerings, meet regulatory and sustainability requirements, and capture market share efficiently. Partnerships with local players, therefore, provide both operational leverage and strategic positioning in a market increasingly defined by compliance, safety, and sustainability priorities.

Saudi Arabia Flame Retardants Market Challenge:

Regulatory Complexities and Compliance Costs

A primary structural challenge facing the Saudi Arabia flame retardants market is the high regulatory complexity and associated compliance costs for manufacturers. The Kingdom has implemented the Product Safety Law (2024) and updated the Saudi Building Code (2025) and Fire Code (SFC), mandating strict fire-safety, material testing, and chemical compliance for polymers, coatings, and insulation. These frameworks require extensive documentation, testing, and certification, including alignment with SASO standards, RoHS-like restrictions, and international fire-resistance norms. For new and smaller market entrants, meeting these requirements involves significant capital expenditure and technical expertise, acting as a barrier to entry and slowing the adoption of new flame-retardant products.

The operational impact is evident across both domestic and foreign suppliers. Compliance entails laboratory testing, quality certification, and repeated auditing, increasing production lead times and raising product costs. For example, manufacturers of halogen-free and phosphorus-based flame-retardant polymers report additional USD 1,500-5,000 in annual certification and conformity assessment expenses to meet SASO and international safety standards. Such costs are disproportionately burdensome for smaller firms, limiting scalability, discouraging innovation, and slowing market expansion in high-volume applications like wiring, automotive components, and construction materials.

Moreover, regulatory divergence between different standards, including SASO, ISO fire-safety norms, and regional chemical compliance requirements, compounds operational complexity. Companies must navigate overlapping frameworks while maintaining product performance and environmental compliance. This structural challenge materially restricts investment decisions, as firms weigh the high upfront cost and ongoing compliance burden against uncertain market returns. Consequently, regulatory and certification hurdles remain the single most critical barrier limiting growth and operational efficiency in Saudi Arabia’s flame-retardant materials market.

Saudi Arabia Flame Retardants Market (2026-32) Segmentation Analysis:

The Saudi Arabia Flame Retardants Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on End-User:

- Building and construction

- Electrical and electronics

- Automotive and transportation

- Consumer goods

- Industrial and manufacturing

The building and construction segment dominates the Saudi Arabia Flame Retardants Market with 38% share, due to rapid urbanisation, extensive residential and commercial infrastructure projects, and stringent fire safety regulations under the Saudi Building Code (SBC 2025). Mandatory fire-resistant materials for insulation, coatings, and structural components create continuous demand, directly linking regulatory compliance to market volume. Government investments under Vision 2030’s urban development programs further expand high-rise construction, increasing the requirement for flame-retardant materials in both public and private sector projects.

Specialist fire engineering firms such as AESG are expanding operations in Saudi Arabia ahead of new SBC and Fire Code enforcement in 2025, reflecting rapid infrastructure growth and rising compliance demand in the construction sector. Additionally, the influx of energy-efficient buildings necessitates polymer-based insulation and cables with high fire-resistance, expanding the addressable market.

Investments in local manufacturing and collaborations with global chemical suppliers ensure material availability, reduce lead times, and allow competitive pricing. This structural support enables the segment to absorb rising costs of advanced flame retardants without deterring adoption. Coupled with consistent regulatory enforcement and large-scale urban projects, building and construction remains the leading end-user segment, sustaining dominance through high and predictable demand over 2026–2032.

Based on Application:

- Plastics and polymers

- Textile

- Wire and cable

- Coating and sealant

- Adhesive and composite

The plastics and polymers segment leads the industry with 32% share, due to its widespread integration in construction, automotive, and electrical applications requiring enhanced fire safety. Regulatory mandates such as SBC 2025 and SASO fire compliance standards compel manufacturers to embed flame retardants in polymer-based wiring, insulation, housings, and composite panels. High adoption in industrial and consumer products ensures volume demand, linking end-user safety priorities directly to segment growth.

Saudi Arabia is investing heavily in large-scale urban development, including NEOM, The Red Sea Project, and Qiddiya Entertainment City, which require extensive use of fire-resistant materials in residential, commercial, and hospitality infrastructure. These mega-projects incorporate advanced insulation, wiring, and polymer-based panels that must comply with the Saudi Building Code. The scale and pace of construction create sustained demand for flame-retardant materials. Collaborations between global polymer suppliers and domestic manufacturers facilitate technology transfer, enhance product quality, and optimize formulation of halogen-free or phosphorus-based flame retardants, increasing the segment’s competitiveness.

Moreover, the versatility of plastics in multiple end-use applications, including construction panels, automotive interiors, and electrical insulation, ensures sustained investment and procurement. Rising infrastructure projects, combined with regulatory enforcement and localised production, strengthen plastics and polymers’ dominance, positioning them as the primary application segment with high resilience and growth potential through 2032.

Saudi Arabia Flame Retardants Market (2026-32) Regional Analysis:

The Central Region, anchored by Riyadh, is the dominant driver of Saudi Arabia’s flame retardants market due to its outsized role in infrastructure development and economic activity. This region seized around 40% share in 2026. Riyadh functions as the Kingdom’s political, financial, and administrative capital, attracting continuous investment in commercial, institutional, and residential construction. According to a recent construction spending analysis, 38 % of Saudi Arabia’s construction contract value is in Riyadh Province , underscoring its dominance in nationwide infrastructure activity. This concentration of projects creates high demand for flame‑resistant building materials, polymer composites, and safety‑compliant construction inputs.

Regulatory and policy advantages further amplify Riyadh’s lead. The Regional Headquarters Programme and broader Vision 2030 investment reforms have made Saudi Arabia, and particularly Riyadh, an attractive destination for global capital and corporate clusters. Substantial foreign direct investment inflows and incentives such as long-term tax exemptions have drawn multinational firms and advanced industrial ventures to base operations in the Central Region, expanding industrial diversity and demand for advanced materials in construction and manufacturing.

SABIC has publicly introduced flame‑retardant compounds designed for modern applications, including consumer electronics and electric vehicle control units, demonstrating active development of flame‑resistant polymer products: LNP THERMOTUF WF0087N, a flame‑retardant PBT compound for electronics. LNP THERMOCOMP WFC061I, a non‑halogenated flame‑retardant compound for EV control units.

Gain a Competitive Edge with Our Saudi Arabia Flame Retardants Market Report:

- The Saudi Arabia Flame Retardants Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Saudi Arabia Flame Retardants Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Saudi Arabia Flame Retardants Market Policies, Regulations, and Product Standards

- Saudi Arabia Flame Retardants Market Trends & Developments

- Saudi Arabia Flame Retardants Market Dynamics

- Growth Factors

- Challenges

- Saudi Arabia Flame Retardants Market Hotspot & Opportunities

- Saudi Arabia Flame Retardants Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Tons)

- Market Share & Outlook

- By Compound- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Inorganic

- Phosphorus-based

- Halogenated (chlorinated or brominated)

- Organic (containing nitrogen or other hetero elements)

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Plastics and polymers

- Textile

- Wire and cable

- Coating and sealant

- Adhesive and composite

- By End-User- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Building and construction

- Electrical and electronics

- Automotive and transportation

- Consumer goods

- Industrial and manufacturing

- By Region- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Central Region

- Eastern Region

- Western Region

- Southern Region

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Compound- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Saudi Arabia Inorganic Flame Retardants Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Tons)

- Market Share & Outlook

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-User- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Saudi Arabia Phosphorus-based Flame Retardants Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Tons)

- Market Share & Outlook

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-User- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Saudi Arabia Halogenated (chlorinated or brominated) Flame Retardants Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Tons)

- Market Share & Outlook

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-User- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Saudi Arabia Organic (containing nitrogen or other hetero elements) Flame Retardants Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Tons)

- Market Share & Outlook

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-User- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Saudi Arabia Flame Retardants Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- BASF SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Albemarle Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lanxess AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Clariant AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ICL Group Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Italmatch Chemicals S.p.A

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DOW Chemicals

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SABIC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- J.M. Huber Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nabaltec AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ADEKA CORPORATION

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF SE

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now