Latin America Biodiesel Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Feedstock (Vegetable Oils, Animal Fats, Others), By Application (Fuel, Power Generation, Others), By Production Technology (Conventional Alcohol Trans-esterification, Pyrolysis, ... Hydro Heating), By Blend Grade (B100, B20, B10, B7, B5, Others), and others Read more

- Energy

- Mar 2026

- Pages 225

- Report Format: PDF, Excel, PPT

Latin America Biodiesel Market

Projected 5.50% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 9.09 Billion

Market Size (2032)

USD 12.54 Billion

Base Year

2025

Projected CAGR

5.50%

Leading Segments

By Application: Fuel

Latin America Biodiesel Market Report Key Takeaways:

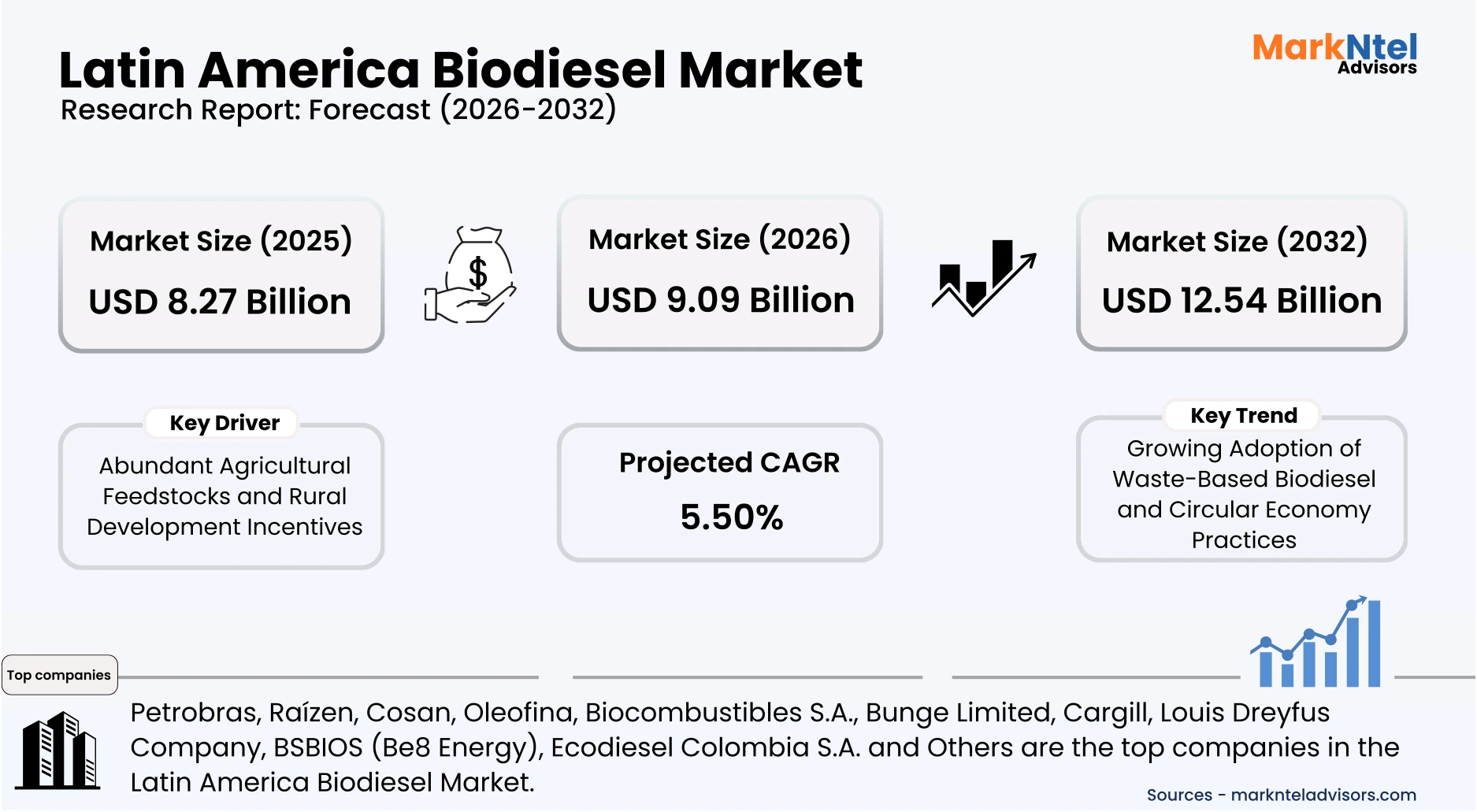

- The Latin America Biodiesel Market size was valued at around USD 8.27 billion in 2025 and is projected to grow from USD 9.09 billion in 2026 to USD 12.54 billion by 2032, exhibiting a CAGR of 5.50% during the forecast period.

- Brazil is the leading country with a significant share of around 65%.

- By Production Technology, the Conventional Alcohol Trans-esterification represented a significant share of about 95% in the Latin America Biodiesel Market in 2026.

- By Application, the Fuel segment seized a significant share of about 92% in the Latin America Biodiesel Market in 2026.

- Leading biodiesel companies in Latin America are Petrobras, Raízen, Cosan, Oleofina, Biocombustibles S.A., Bunge Limited, Cargill, Louis Dreyfus Company, BSBIOS (Be8 Energy), Ecodiesel Colombia S.A. and Others.

Market Insights & Analysis: Latin America Biodiesel Market (2026-32):

The Latin America Biodiesel market size was valued at around USD 8.27 billion in 2025 and is projected to grow from USD 9.09 billion in 2026 to USD 12.54 billion by 2032, exhibiting a CAGR of 5.50% during the forecast period. i.e., 2026-32.

Latin America’s biodiesel market has expanded steadily due to long-standing national biofuel programmes and blending mandates that enhance energy security and reduce fossil fuel reliance. The presence of biodiesel blending requirements in Argentina, Colombia, and other countries further underpins a growing regulatory foundation for biodiesel integration into mainstream fuel markets. Such mandates create stable demand signals necessary for economic planning and capacity expansion.

End-user demand across transport and industrial segments is a key force shaping biodiesel uptake, with heavy-duty freight and public transport fleets increasingly influenced by blending requirements. In Brazil, mandatory biodiesel content applies to highway diesel, ensuring that commercial logistics operators and mass transit systems consume significant volumes of biodiesel annually. Regional variations in mandates mean that industrial users in Colombia transition toward higher blends (e.g., B12–B15 depending on region), driving biodiesel use beyond niche applications. These institutional and commercial segments generate concentrated demand volumes that support biodiesel market growth and attract investment into distribution and blending infrastructure.

Looking ahead, technological and institutional developments signal sustained biodiesel market momentum. Brazil has established technical subcommittees to evaluate the feasibility of higher biodiesel blends (B>15), integrating government, research institutions, and industry stakeholders to assess performance and infrastructure readiness. Expansion of biodiesel use in marine and heavy transport sectors is under study, reflecting an evolving policy emphasis on decarbonizing harder‑to‑abate energy end‑uses. The continued alignment of national plans with emissions reduction commitments and infrastructure upgrades suggests that biodiesel will remain a strategic component of Latin America’s energy transition through the mid‑2020s and beyond.

Latin America Biodiesel Market Recent Developments:

- 2025: Brazil and Mexico forge biofuel partnership. In 2025, Brazil and Mexico signed memorandums of understanding to strengthen commercial cooperation in the agriculture and biocombustível sectors, highlighting strategic cross-border investment and trade initiatives for biodiesel and other renewable fuels.

- 2026: Volvo adds B100 biodiesel option. In early 2026, automaker Volvo announced that its urban chassis model (B320R) would offer compatibility with 100 % biodiesel (B100), marking an important adoption milestone for higher‑blend biodiesel use in Latin America.

Latin America Biodiesel Market Scope:

| Category | Segments |

|---|---|

| By Feedstock | (Vegetable Oils, Animal Fats, Others), |

| By Application | (Fuel, Power Generation, Others), |

| By Production Technology | (Conventional Alcohol Trans-esterification, Pyrolysis, Hydro Heating), |

| By Blend Grade | (B100, B20, B10, B7, B5, Others), |

Latin America Biodiesel Market Driver:

Abundant Agricultural Feedstocks and Rural Development Incentives

The large-scale availability of agricultural feedstocks across Latin America has emerged as a fundamental driver accelerating biodiesel market expansion in the region. Countries such as Brazil and Argentina are among the world’s largest producers of soybeans, which represent the primary feedstock for biodiesel production. According to the United States Department of Agriculture (USDA), Brazil produced approximately 166 million metric tons of soybeans in 2025, maintaining its position as the world’s largest producer . This extensive agricultural output ensures a stable and cost-effective supply of soybean oil for biodiesel manufacturers. As biodiesel production relies heavily on vegetable oils and animal fats, the region’s strong agricultural base directly supports large-scale fuel production capacity.

The measurable influence of feedstock availability is reflected in expanding biodiesel manufacturing volumes and processing infrastructure across major producing countries. Brazil’s Ministry of Agriculture reported that soybean crushing capacity has continued to expand to meet both export and domestic biofuel demand. Similarly, Argentina’s Secretariat of Agriculture noted that the country remains one of the world’s leading exporters of soybean oil, a key biodiesel input. The Food and Agriculture Organization (FAO) states that South America accounts for a substantial share of global soybean cultivation, providing a consistent raw material pipeline for the biodiesel industry. This large feedstock base allows producers to maintain stable supply chains and scale production efficiently across domestic and export markets.

Government-led rural development incentives have further strengthened the link between agriculture and biodiesel production in the region. Brazil’s RenovaBio program and the Social Fuel Seal policy encourage biodiesel producers to source feedstock from smallholder farmers by offering tax benefits and market access incentives. In 2025, Brazil’s Ministry of Mines and Energy reaffirmed support for integrating family agriculture into biodiesel supply chains to boost rural incomes. Such policies expand biodiesel feedstock cultivation while promoting regional economic development. As a result, the combination of abundant agricultural resources and supportive rural policies continues to structurally increase biodiesel production capacity and market demand across Latin America.

Latin America Biodiesel Market Trend:

Growing Adoption of Waste-Based Biodiesel and Circular Economy Practices

A significant trend shaping the Latin America biodiesel market is the growing adoption of waste-based feedstocks, particularly used cooking oil and animal fats, to support circular economy objectives. Governments and biofuel producers are increasingly utilizing waste materials to produce biodiesel to reduce environmental impact and improve resource efficiency. According to the International Energy Agency, waste oils and residues are becoming an important feedstock source for biofuel production due to their lower lifecycle emissions. This shift is encouraging biodiesel producers to diversify raw material sourcing beyond conventional vegetable oils. As sustainability regulations strengthen, the use of waste-derived feedstocks is gaining greater policy and industry support. For example, in Argentina expansion of biofuels is also reducing dependency on fossil fuels.

The expansion of waste-based biodiesel production is creating structural changes across the value chain by integrating waste collection systems with biofuel manufacturing. Municipal waste management authorities, food service industries, and biodiesel producers are increasingly collaborating to collect and process used cooking oil for fuel production. The Food and Agriculture Organization highlights that utilizing agricultural and food waste streams for bioenergy can significantly improve resource efficiency and reduce environmental burdens. This integration is also encouraging investments in specialized processing facilities capable of converting low-cost residues into high-quality biodiesel.

The trend is expected to persist as governments and industries intensify efforts to promote sustainable fuel production. Waste-based biodiesel offers significant lifecycle emission reductions compared to conventional fossil diesel while minimizing pressure on agricultural land resources. International organizations such as the International Renewable Energy Agency emphasize the importance of advanced biofuels derived from residues and wastes for achieving long-term climate targets. Consequently, the adoption of circular economy practices is likely to play an increasingly important role in the evolution of the Latin American biodiesel market.

Latin America Biodiesel Market Opportunity:

Increasing Demand from International Markets

A major market opportunity for new and emerging players in the Latin American biodiesel market is the growing export demand from regions implementing stricter renewable fuel regulations. European countries are strengthening low-carbon fuel policies to reduce transport emissions, creating additional demand for sustainable biodiesel imports. According to the International Energy Agency, biofuels remain a key component of decarbonizing heavy-duty transport, where electrification remains limited. Latin American producers, particularly in soybean-rich countries such as Argentina and Brazil, possess strong feedstock availability and large-scale agricultural supply chains. These structural advantages position the region as a competitive supplier of biodiesel to international markets seeking low-carbon fuel alternatives.

The opportunity has emerged due to tightening sustainability targets and renewable fuel mandates in global energy markets. As countries introduce stricter emissions standards, demand for certified biofuels that meet environmental criteria continues to increase. Reuters has reported that Argentina has expanded biodiesel production and exports in response to international demand for renewable fuels. This export-driven demand encourages investment in biodiesel production capacity and supply chain infrastructure across Latin American economies. Increased international trade in biofuels also enables producers to access higher-value markets beyond domestic fuel blending programs.

This opportunity is particularly advantageous for smaller or new producers because biodiesel production technologies are relatively modular and scalable. Companies can establish mid-sized production facilities that utilize locally available feedstocks such as soybean oil or animal fats. With growing international demand for sustainable fuels, exporters that meet certification and quality standards can access global markets without competing solely in domestic fuel markets. As renewable fuel regulations continue strengthening worldwide, export-oriented biodiesel production will remain a promising growth pathway for emerging market participants.

Latin America Biodiesel Market Challenge:

High Feedstock Price Volatility and Supply Constraints

A major structural challenge in the Latin American biodiesel market is the volatility and constrained availability of feedstocks such as soybean oil, palm oil, and animal fats. The region’s biodiesel industry relies heavily on soybean oil, particularly in Brazil and Argentina, where the International Energy Agency (IEA) notes that more of the biodiesel output depends on soybean-derived inputs. Fluctuations in global oilseed prices, influenced by weather variability and export demand, have significantly increased input costs for biodiesel producers.

Recent policy developments have further intensified supply pressures. In 2025, Brazil’s National Energy Policy Council maintained the biodiesel blending mandate at B14 but delayed the planned B15 increase due to concerns over feedstock cost inflation and food price impacts, according to Brazil’s Ministry of Mines and Energy. Similarly, Argentina’s soybean oil exports surged following currency adjustments and international demand, tightening domestic availability for biodiesel processing facilities.

These conditions create operational uncertainty and restrict market scalability for producers across the region. High and unpredictable feedstock prices reduce profit margins, discourage capacity expansion, and increase financial risk for new entrants. The World Bank and FAO have also highlighted that competing demand from the food sector and export markets continues to elevate oilseed prices, limiting stable and cost-efficient biodiesel production growth in Latin America.

Latin America Biodiesel Market (2026-32) Segmentation Analysis:

The Latin America Biodiesel Market of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Production Technology:

- Conventional Alcohol Trans-esterification

- Pyrolysis

- Hydro Heating

The Conventional Alcohol Trans-esterification process dominates biodiesel production across Latin America with a market share of 95% due to its proven scalability, low capital intensity, and compatibility with widely available feedstocks such as soybean oil and animal fats. Countries like Brazil and Argentina heavily rely on this method because it enables high-volume production with operational reliability, unlike pyrolysis or hydro heating, which require more complex infrastructure and higher investment.

Government policies, particularly blending mandates and renewable fuel incentives, reinforce the use of transesterification technology. Brazil’s national biodiesel program mandates minimum biodiesel content in diesel, encouraging producers to adopt facilities integrated with oilseed processing plants. These policy frameworks provide predictable demand, making conventional transesterification a low-risk investment choice.

Investment flows into infrastructure expansion and feedstock supply chains further strengthen the dominance of this technology. Large agribusiness and biofuel firms, including Petrobras, Raizen, Cosan, Bunge, and Cargill, have invested in expanding transesterification capacity . These investments, combined with growing end-user demand in transportation and logistics, ensure that conventional alcohol transesterification remains the leading production technology in the region. Brazilian processors, including major agribusiness firms, are investing over USD 1.1 billion to expand crushing capacity tied to biodiesel supply.

Based on Application:

- Fuel

- Power Generation

- Others

The Fuel segment leads the Latin America biodiesel market with a market share of 92%, as biodiesel is primarily consumed as a transportation fuel blended with conventional diesel. Road freight, public transport, and agricultural machinery in countries such as Brazil, Argentina, and Colombia drive consistent demand, creating a robust base for the fuel application segment.

Government mandates for biodiesel blending in diesel supply, such as Brazil’s national policy, directly support sustained consumption in transportation. Regulatory requirements provide stable, long-term volumes that enable fuel distributors to integrate biodiesel into nationwide fuel networks efficiently.

Investment in renewable fuels and decarbonization strategies also bolsters the fuel segment. Capital allocation by both private firms and renewable energy funds targets transport fuel infrastructure, blending terminals, and distribution networks. Companies such as Raízen, Cosan, Oleofina, Biocombustibles S.A., and Ecodiesel Colombia S.A. contribute to scaling up production and distribution. For example, Argentina has dozens of biodiesel plants and a significant biodiesel industry, which implies that companies such as Biocombustibles S.A. operate within a well-established sector of producers. Argentina is home to around 33 biodiesel plants, showing a mature industrial base. Consequently, the Fuel segment’s dominance is reinforced by policy-driven demand, investment in infrastructure, and high-end-user adoption in the transportation sector.

Latin America Biodiesel Market (2026-32) Regional Analysis:

Brazil accounts for the largest share of biodiesel production in Latin America, with a market share of 65%, responsible for a majority of regional output thanks to its vast agricultural base and well-developed industrial infrastructure. The country produced an estimated 8.9 billion liters of biodiesel in 2024, up sharply from previous years, driven by expanding plant capacity and more blending in diesel fuel. This large production is supported by abundant feedstock such as soybean oil and advanced processing capacity across numerous facilities in states like Mato Grosso and Rio Grande do Sul. Brazil’s agri-industrial clusters and logistics networks allow efficient scale-up compared to neighboring countries, where capacity is smaller and more fragmented.

Brazil’s biodiesel market leadership is strongly reinforced by ambitious government policy. The National Program for the Production and Use of Biodiesel (PNPB) has guided the industry for two decades, resulting in cumulative production of 77 billion liters and substantial diesel import savings. Blending mandates have steadily increased from B12 to 14 % in 2024 and are planned rise to 15 % in 2025, with future increases planned under the “Fuel of the Future” law and National Energy Policy Council targets. These mandates provide l ong‑term demand certainty and attract investment into plant expansions and supply chain upgrades.

End-user demand in Brazil’s transport and logistics sectors is concentrated and large, with biodiesel now an integral part of the national diesel pool. Diesel demand growth for road freight and agriculture translates directly into biodiesel consumption under the blending laws. Bunge Brazil inaugurated its first biodiesel plant in Nova Mutum, Mato Grosso, with USD 11.35 million investment and an annual production target of around 150,000 m³ (~150 million L).

Gain a Competitive Edge with Our Latin America Biodiesel Market Report:

- The Latin America Biodiesel Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Latin America Biodiesel Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Latin America Biodiesel Market Policies, Regulations, and Product Standards

- Latin America Biodiesel Market Trends & Developments

- Latin America Biodiesel Market Dynamics

- Growth Factors

- Challenges

- Latin America Biodiesel Market Hotspot & Opportunities

- Latin America Biodiesel Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Liters)

- Market Share & Analysis

- By Feedstock- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Vegetable Oils

- Soybean Oil

- Palm Oil

- Waste Cooking Oil

- Animal Fats

- Others

- Vegetable Oils

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Fuel

- Power Generation

- Others

- By Production Technology- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Conventional Alcohol Trans-esterification

- Pyrolysis

- Hydro Heating

- By Blend Grade- Market Size & Forecast 2022-2032, USD Million & Million Liters

- B100

- B20

- B10

- B7

- B5

- Others

- By Country

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Peru

- Rest of Latin America

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Feedstock- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Brazil Biodiesel Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Liters)

- Market Share & Analysis

- By Feedstock- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Production Technology- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Blend Grade- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Mexico Biodiesel Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Liters)

- Market Share & Analysis

- By Feedstock- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Production Technology- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Blend Grade- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Argentina Biodiesel Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Liters)

- Market Share & Analysis

- By Feedstock- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Production Technology- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Blend Grade- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Colombia Biodiesel Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Liters)

- Market Share & Analysis

- By Feedstock- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Production Technology- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Blend Grade- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Chile Biodiesel Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Liters)

- Market Share & Analysis

- By Feedstock- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Production Technology- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Blend Grade- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Peru Biodiesel Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Liters)

- Market Share & Analysis

- By Feedstock- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Application- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Production Technology- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Blend Grade- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Latin America Biodiesel Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Petrobras

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Raízen

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cosan

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Oleofina

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Biocombustibles S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bunge Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cargill

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Louis Dreyfus Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BSBIOS (Be8 Energy)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ecodiesel Colombia S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Petrobras

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now