Japan Yoghurt Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Product Type (Spoonable Yoghurt, Drinkable Yoghurt, Greek / High-Protein Yoghurt, Frozen Yoghurt), By Flavor (Flavored, Plain / Natural), By Type (Dairy-Based, Non-Dairy / Plant ... -Based), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Others), and others Read more

- Food & Beverages

- Feb 2026

- Pages 130

- Report Format: PDF, Excel, PPT

Japan Yoghurt Market

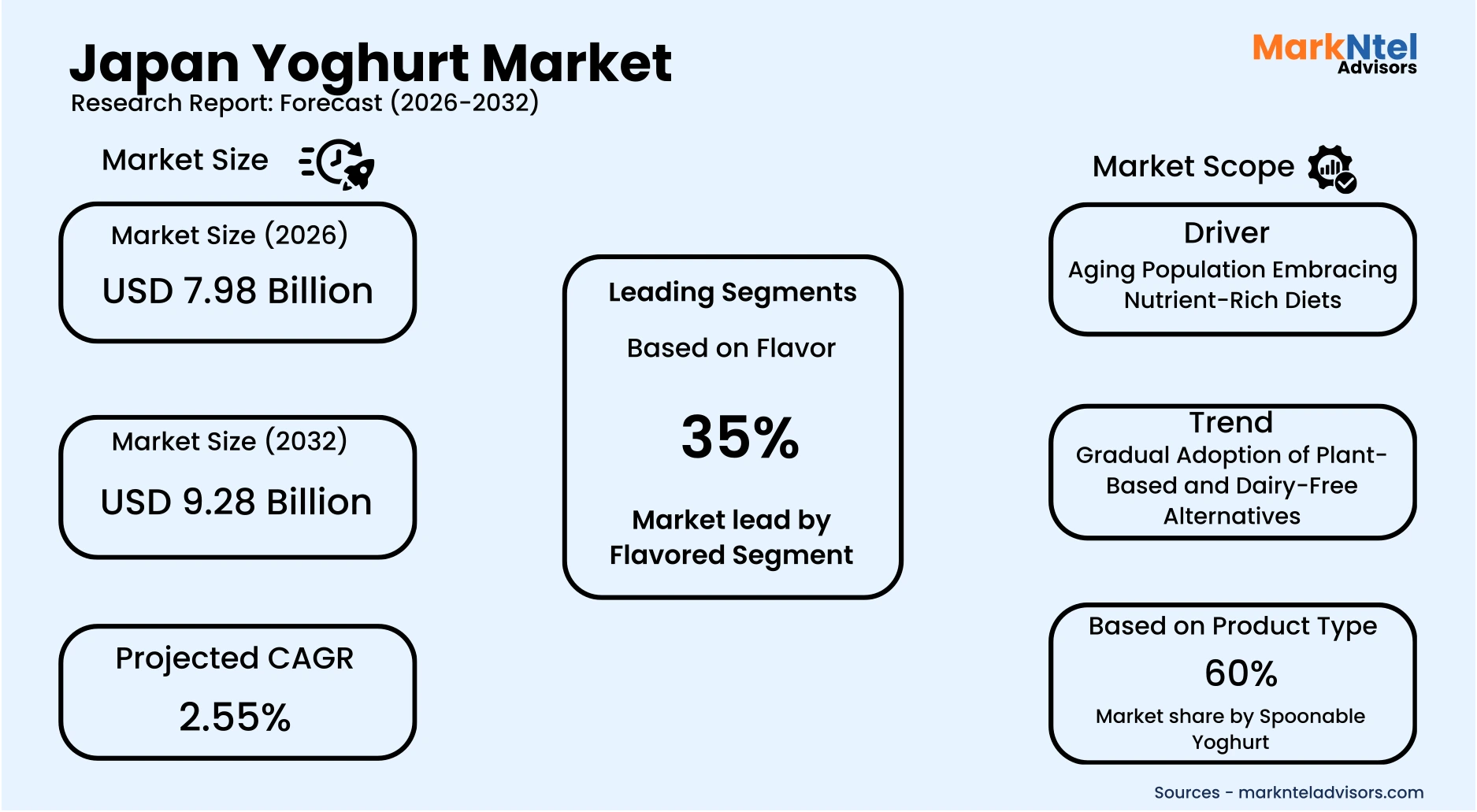

Projected 2.55% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 7.98 Billion

Market Size (2032)

USD 9.28 Billion

Base Year

2025

Projected CAGR

2.55%

Leading Segments

By Flavor: Flavored

Japan Yoghurt Market Report Key Takeaways:

- The Japan Yoghurt Market size was valued at around USD 7.11 billion in 2025 and is projected grow from USD 7.98 billion in 2026 to USD 9.28 billion by 2032, exhibiting a CAGR of 2.55% during the forecast period.

- By Region, Kanto holds the largest market share of about 39% in the Japan Yoghurt Market in 2026.

- By Product Type, the Spoonable Yoghurt segment represented a significant share of about 60% in the Japan Yoghurt Market in 2026.

- By Flavor, the Flavored segment presented a significant share of about 35% in the Japan Yoghurt Market in 2026.

- Leading Yoghurt Companies in Japan are Meiji Co., Ltd., Morinaga Milk Industry Co., Ltd., Megmilk Snow Brand Co., Ltd., Yakult Honsha Co., Ltd., Danone Japan, Nissin York Co, Nippon Luna, Ezaki Glico Co., Ltd., Chichiyasu Dairy Co., Ltd., Ohayo Dairy Products, and Others.

Market Insights & Analysis: Japan Yoghurt Market (2026-32):

The Japan Yoghurt Market size was valued at around USD 7.11 billion in 2025 and is projected grow from USD 7.98 billion in 2026 to USD 9.28 billion by 2032, exhibiting a CAGR of 2.55% during the forecast period, i.e., 2026-32.

Japan’s yoghurt market continues to demonstrate structural stability, supported by sustained household expenditure and an established dairy supply base. According to the USDA (GAIN Report JA2025-0066), citing Japan’s Statistics Bureau Family Income and Expenditure Survey, average yoghurt spending among two-or-more-person households reached USD 70.99 during January–September 2025, confirming yoghurt’s role as a routine food purchase . This steady per-household expenditure reflects resilient residential demand despite broader food price pressures. Consistent domestic milk output reported by Japan’s Ministry of Agriculture, Forestry and Fisheries (MAFF) further ensures raw material availability for fermented dairy production.

Demographic trends are a critical long-term growth driver, as Japan remains one of the world’s most rapidly aging societies. The Statistics Bureau reports that nearly 29% of the population is aged 65 or older, strengthening demand for probiotic and digestive-health products commonly consumed by senior households . Regulatory oversight under the Ministry of Health, Labor and Welfare’s Food for Specified Health Uses (FOSHU) and Foods with Function Claims (FFC) systems allows scientifically validated health claims, reinforcing consumer confidence in functional yoghurt products. These frameworks support innovation while maintaining strict labeling compliance, thereby enhancing product credibility across residential and institutional end users.

Beyond household consumption, commercial and institutional users contribute incremental demand growth. Hospitals, elderly care facilities, and school meal programs increasingly incorporate probiotic dairy into nutrition planning, aligning with preventive healthcare objectives. Supermarkets and convenience stores, Japan’s dominant food retail formats, provide extensive cold-chain coverage, ensuring nationwide accessibility and supporting high product turnover. Infrastructure modernization and digital logistics improvements outlined in recent economic revitalization strategies further enhance distribution efficiency, enabling manufacturers to scale premium and high-protein yoghurt offerings across urban centers.

Looking ahead, MAFF’s ongoing dairy productivity initiatives and sustainability measures aim to stabilize domestic milk supply while improving environmental performance. Leading manufacturers continue investing in functional formulations, recyclable packaging, and localized production capacity to align with national circular economy objectives. Stable household expenditure levels, regulatory clarity, demographic-driven health awareness, and diversified end-user demand collectively support moderate but sustained market expansion. Consequently, Japan’s yoghurt market outlook remains positive through the late 2020s, underpinned by policy-backed supply stability and consistent consumer consumption patterns.

Japan Yoghurt Market Recent Developments:

- 2025 : Meiji Co., Ltd. launched Meiji Haemoglobin A1c Countermeasure Yogurt and its drinkable version nationwide, formulated with MI-2 lactic acid bacteria to support blood sugar control. The 112g products retail at approximately USD 1.05 and are positioned as daily functional foods, though they are not classified as medicines or government-approved treatments.

- 2025 : Meiji introduced Meiji W Skin Care Yogurt, a drinkable functional yoghurt combining SC-2 lactic acid bacteria with collagen peptides and sphingomyelin to address skin hydration and UV tolerance concerns.

Japan Yoghurt Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Spoonable Yoghurt, Drinkable Yoghurt, Greek / High-Protein Yoghurt, Frozen Yoghurt), |

| By Flavor | (Flavored, Plain / Natural), |

| By Type | (Dairy-Based, Non-Dairy / Plant-Based), |

| By Distribution Channel | (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Others), |

Japan Yoghurt Market Driver:

Aging Population Embracing Nutrient-Rich Diets

Japan’s demographic transition toward an older society remains the most influential structural driver expanding yoghurt demand. In 2025, the Ministry of Internal Affairs and Communications estimated the elderly population at 36.19 million, including 20.51 million women and 15.68 million men, highlighting the scale of the senior consumer base. This sustained expansion structurally increases the proportion of health-focused households across the country. The continued rise in elderly and elderly-couple households permanently enlarges the segment most inclined toward preventive nutrition and functional food consumption.

The demand impact is reinforced by national nutrition guidance and corporate response. Japan’s health longevity guidelines recommend that adults aged 65 and older derive 15–20% of daily energy from protein, highlighting the importance of adequate protein intake for muscle maintenance and healthy aging. Reflecting this shift, Morinaga Milk Industry Co., Ltd. launched a series of functional products across yoghurt, fermented drinks, and milk formulations in 2025 to support the nutritional needs of Japan’s aging population, with immune health identified as a key consumer focus. Such innovation demonstrates direct alignment between demographic realities and product development strategies.

This driver materially expands market volume rather than merely influencing pricing because demographic aging structurally increases the number of routine yoghurt consumers. Older adults are more likely to incorporate probiotic and protein-rich dairy into their daily diets for digestive and immune support, driving consistent repeat purchases. Institutional procurement by hospitals and long-term care facilities further scales with the expanding elderly population, generating sustained bulk demand beyond retail channels. As demographic aging is predictable and long-term, it functions as a systemic volume generator underpinning sustained growth in Japan’s yoghurt market.

Japan Yoghurt Market Trend:

Gradual Adoption of Plant-Based and Dairy-Free Alternatives

The gradual adoption of plant-based and dairy-free alternatives represents a structural shift reshaping Japan’s yoghurt market, supported by sustainability policy alignment and evolving consumer preferences. Japan’s Ministry of Agriculture, Forestry, and Fisheries has emphasized protein diversification and sustainable food systems under its 2025 policy direction, encouraging innovation in alternative protein sources. Simultaneously, Japan’s reaffirmed commitment to carbon neutrality by 2050 has intensified corporate focus on lower-emission food production. These policy drivers have accelerated the expansion of plant-derived fermented products within mainstream retail channels.

The trend is further reinforced by measurable dietary tolerance patterns within the population. Peer-reviewed clinical research has reported that approximately 19% of Japanese adults exhibited milk intolerance symptoms after consuming 200 mL of milk, while broader scientific literature confirms high lactase deficiency prevalence across East Asian populations. These physiological factors provide a structural demand foundation for lactose-reduced and plant-based yoghurt alternatives. As awareness of digestive health increases, consumers are increasingly considering non-dairy options as practical dietary substitutes.

This shift is influencing product portfolios, supply chains, and competitive positioning across the value chain. Manufacturers are expanding soy-based yoghurt alternatives, leveraging Japan’s established fermentation expertise and soy-processing infrastructure. In 2024, Marusanai Co., Ltd. relaunched its “Soymilk Yogurt 400g Made with Domestic Soybeans” as a functional food approved by Japan’s Consumer Affairs Agency for improving bowel movements, with the series reporting shipment growth for 13 consecutive years . In 2025, Tsunan Sake Brewery Co., Ltd. joined the JOGURT project to develop plant-based “Sake Brewery Yogurt” using upcycled sake lees under brewery-grade fermentation standards, reinforcing circular production models within the dairy-alternative segment. Retailers are allocating shelf space to dairy-free SKUs alongside conventional dairy, signaling mainstream integration. Anchored in both sustainability policy and stable biological dietary patterns, the trend is expected to persist, materially shaping long-term market diversification and industry dynamics.

Japan Yoghurt Market Opportunity:

Growth in Functional and Fortified Yogurt Innovations

A significant structural opportunity exists in Japan’s functional and fortified yogurt segment, driven by regulatory accessibility and rising preventive health demand. Japan’s Consumer Affairs Agency operates the Foods with Function Claims (FFC) system, which allows companies to commercialize scientifically supported health claims through a notification-based framework rather than full FOSHU approval. This regulatory structure lowers compliance complexity and reduces entry barriers for smaller firms. As health-conscious consumption expands under national dietary guidance, functional dairy products are increasingly prioritized by consumers.

This opportunity translates into measurable demand because consumers actively seek products addressing digestive health, immunity, metabolic balance, and protein intake. Peer-reviewed scientific research supporting probiotic strains and nutrient fortification reinforces product credibility, encouraging repeat purchases. Clear on-pack functional labeling enhances consumer trust and supports premium pricing potential. For instance, in September 2024, Showa Sangyo Co., Ltd. launched “Bone Care Drink Yogurt Flavor,” a functional beverage formulated with maltobionic acid to enhance calcium absorption and support bone density maintenance, demonstrating the expanding commercialization of condition-specific fortified dairy products . Consequently, differentiated fortified yogurt products can achieve faster shelf penetration within modern retail channels.

The segment is particularly advantageous for new entrants due to its innovation-driven nature rather than scale-driven competition. Smaller firms can specialize in targeted strains, plant-based fortification, or condition-specific formulations aligned with FFC notifications. Unlike incumbents managing broad portfolios, emerging players can focus on niche health positioning and agile product development. Therefore, functional and fortified yogurt innovation presents a scalable, regulation-supported opportunity for competitive differentiation in Japan’s yogurt market.

Japan Yoghurt Market Challenge:

Volatile Cost of Raw Milk & Feed

Volatility in raw milk and feed costs represents a structural constraint limiting profitability and scalability within Japan’s yogurt market. Japan relies heavily on imported feed grains, making domestic dairy production sensitive to global commodity price fluctuations and exchange rate movements. According to Japan’s Ministry of Agriculture, Forestry and Fisheries, feed costs have remained elevated following global supply disruptions and currency depreciation pressures in recent years. This dependence exposes dairy processors to input cost instability beyond domestic control.

The impact is measurable across the value chain. Rising feed costs increase farm-level milk production expenses, which translate into higher procurement prices for processors. In response, dairy companies have implemented retail price revisions to offset increased raw material and energy costs, as widely reported by major Japanese food manufacturers in 2024 and 2025. Such price adjustments can dampen consumer purchasing frequency in a price-sensitive retail environment. Reflecting these pressures, the number of dairy farmers in Japan fell below 10,000 in October 2024 for the first time since 2005, with 58.9% reportedly operating at a deficit and 47.9% considering exiting the industry, underscoring the financial strain linked to rising input costs and currency weakness. Smaller producers are particularly vulnerable due to limited hedging capacity and narrower operating margins.

This volatility materially restricts market expansion by discouraging long-term capital investment and new market entry. Uncertain input costs complicate production planning and inventory management, affecting operational efficiency. While government dairy support measures aim to stabilize farm income, exposure to global feed markets remains significant. Consequently, persistent raw material cost fluctuations act as a systemic barrier to predictable growth and sustainable margin expansion within Japan’s yogurt industry.

Japan Yoghurt Market (2026-32) Segmentation Analysis:

The Japan Yoghurt market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Spoonable Yoghurt

- Drinkable Yoghurt

- Greek / High-Protein Yoghurt

- Frozen Yoghurt

The spoonable yoghurt dominates the Japan Yoghurt Market, accounting for approximately 60% of total product demand, primarily because it aligns with traditional eating habits and structured meal consumption patterns. Spoonable yoghurt is commonly consumed at breakfast or as a dessert-style snack, making it more integrated into daily routines compared to drinkable formats. Its thicker texture and perceived satiety value position it as a food item rather than a beverage substitute. This habitual integration drives consistent repeat purchases and higher household penetration.

Manufacturing and retail dynamics further reinforce this leadership. Domestic dairy processors have long-established fermentation and cup-filling infrastructure optimized for spoonable formats, enabling large-scale, cost-efficient production. Supermarkets and convenience stores allocate significant refrigerated shelf space to multi-serve tubs and single-serve cups, enhancing visibility and promotional activity. The format also supports private-label expansion, increasing competitive pricing options and strengthening volume sales across mainstream retail channels.

Additionally, spoonable yoghurt offers greater formulation flexibility for value-added innovation. It can incorporate fruit preparations, cereals, high-protein blends, and probiotic strains without altering core consumption behavior. This adaptability allows brands to launch functional and premium variants while retaining familiar packaging and eating occasions. As a result, established consumption habits, production scalability, and innovation compatibility collectively sustain spoonable yoghurt’s dominant 60% market share in Japan.

Based on Flavor:

- Flavored

- Plain / Natural

The flavored segment dominates the Japan Yoghurt Market, accounting for approximately 35% of total flavor demand, primarily because it aligns with consumer preference for taste-enhanced, ready-to-eat dairy products. Flavored variants such as strawberry, blueberry, and peach are widely positioned as convenient snack options, appealing to both children and working adults seeking balanced sweetness and nutritional value. Japan’s strong culture of seasonal fruit consumption further supports demand for fruit-based yoghurt flavors. This sensory appeal increases repeat purchases and expands usage beyond traditional breakfast occasions.

Retail and product innovation dynamics further reinforce this dominance. Supermarkets and convenience stores frequently rotate limited-edition and seasonal fruit flavors, stimulating trial consumption and impulse purchases. Domestic manufacturers continuously introduce region-specific fruit blends and reduced-sugar flavored variants, combining indulgence with health positioning. For example, Kaneka Corporation launched its organic JAS-certified “Pur Natur™ Organic Yogurt Strawberry-Mix,” while McDonald's Japan Co., Ltd. introduced a limited-time Blueberry Yogurt Flavored Grimace Shake in October 2024, reflecting continued innovation in fruit-based yogurt flavors. The ability to combine probiotics, added protein, and fruit preparations in a single cup strengthens perceived value without altering consumption habits.

Additionally, flavored yoghurt benefits from broader demographic penetration compared to plain or natural variants, which are often preferred for cooking or health-specific purposes. The mild sweetness profile enhances accessibility among younger consumers and those less inclined toward unsweetened dairy products. Scalable fruit preparation supply chains and established blending technologies enable cost-efficient production at volume.

Japan Yoghurt Market (2026-32): Regional Projection

The Kanto region dominates the Japan Yoghurt Market, accounting for approximately 39% of total regional demand, primarily because it represents the country’s largest population and economic concentration zone. According to Japan’s Statistics Bureau, the Greater Tokyo Area, which includes Tokyo, Kanagawa, Saitama, and Chiba, remains the most densely populated metropolitan cluster in the country. This high population density sustains strong daily consumption of packaged food products, including yogurt, through modern retail and convenience store networks. The region’s urban lifestyle and higher disposable income levels further support frequent purchases of value-added and premium dairy products.

Industrial and distribution infrastructure also reinforces Kanto’s leadership. The region hosts headquarters and production facilities of major food and dairy companies, enabling efficient supply chain coordination and rapid product rollout. Tokyo’s position as Japan’s commercial hub strengthens logistics connectivity, ensuring high product turnover and minimal distribution delays. Extensive cold-chain infrastructure across supermarkets and convenience stores enhances the availability of spoonable, drinkable, and functional yogurt variants.

Additionally, Kanto’s concentration of working professionals and students drives demand for convenient, ready-to-eat dairy snacks. Retail innovation, promotional activity, and frequent product launches are typically piloted in Tokyo before nationwide expansion, reinforcing regional sales concentration. The combination of demographic scale, economic concentration, retail density, and manufacturing presence collectively positions Kanto as the leading regional market for yogurt consumption in Japan.

Gain a Competitive Edge with Our Japan Yoghurt Market Report:

- Japan Yoghurt Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Japan Yoghurt Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Japan Yoghurt Market Policies, Regulations, and Product Standards

- Japan Yoghurt Market Trends & Developments

- Japan Yoghurt Market Dynamics

- Growth Factors

- Challenges

- Japan Yoghurt Market Hotspot & Opportunities

- Japan Yoghurt Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Spoonable Yoghurt

- Drinkable Yoghurt

- Greek / High-Protein Yoghurt

- Frozen Yoghurt

- By Flavor- Market Size & Forecast 2022-2032, USD Million

- Flavored

- Plain / Natural

- By Type- Market Size & Forecast 2022-2032, USD Million

- Dairy-Based

- Non-Dairy / Plant-Based

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Others

- By Region- Market Size & Forecast 2022-2032, USD Million

- Kanto

- Kansai

- Chubu

- Kyushu

- Tohoku

- Chugoku

- Hokkaido

- Shikoku

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Spoonable Yoghurt Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Flavor- Market Size & Forecast 2022-2032, USD Million

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Drinkable Yoghurt Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Flavor- Market Size & Forecast 2022-2032, USD Million

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Greek / High-Protein Yoghurt Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Flavor- Market Size & Forecast 2022-2032, USD Million

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Frozen Yoghurt Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Flavor- Market Size & Forecast 2022-2032, USD Million

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Yoghurt Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Meiji Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Morinaga Milk Industry Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Megmilk Snow Brand Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yakult Honsha Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Danone Japan

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nissin York Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nippon Luna

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ezaki Glico Co Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chichiyasu Dairy Co Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ohayo Dairy Products

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Meiji Co., Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now