Italy Swimming Pool Chemicals Market Research Report: Growth Drivers & Forecast (2026-2032)

By Product (Sanitizers & Treatment Types (Sanitizers, pH Adjusters, Algaecides, Water Balancers), By Form (Tablets/Granules, Liquids, Cartridges/Pods, Other Forms), By Pool Type (R ... esidential Pools, Commercial Pools, Public Pools), By End User (Hospitality Sector, Real Estate, Sports Facilities, Municipal Bodies, Other End Users), and others Read more

- Chemicals

- Mar 2026

- Pages 150

- Report Format: PDF, Excel, PPT

Italy Swimming Pool Chemicals Market

Projected 5.83% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 32.6 Million

Market Size (2032)

USD 45.80 Million

Base Year

2025

Projected CAGR

5.83%

Leading Segments

By the pool type: Residential Pools

Italy Swimming Pool Chemicals Market Report Key Takeaways:

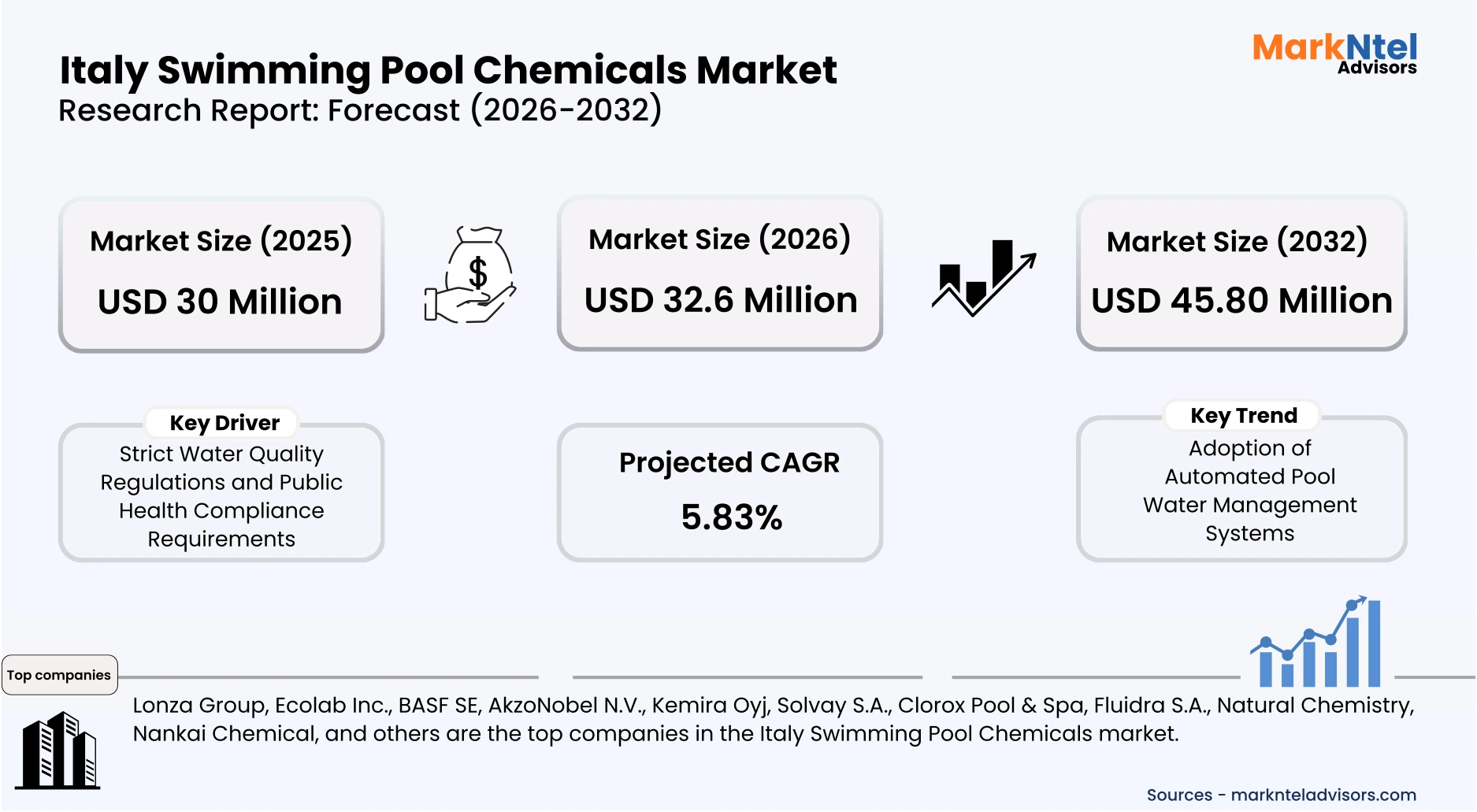

- The Italy Swimming Pool Chemicals market size was valued at USD 30 million in 2025 and is projected to grow from USD 32.6 million in 2026 to USD 45.80 million by 2032, exhibiting a CAGR of 5.83% during the forecast period.

- Northwest is the leading region with a significant share of 28% in 2026.

- By Product Type, Sanitizer seized a significant share of about 45% in the Italian Swimming Pool Chemicals Industry in 2026.

- By Pool Type, the residential pools hold a significant share of about 55% in the Italy Swimming Pool Chemicals market in 2026.

- Leading companies are Lonza Group, Ecolab Inc., BASF SE, AkzoNobel N.V., Kemira Oyj, Solvay S.A., Clorox Pool & Spa, Fluidra S.A., Natural Chemistry, Nankai Chemical, and Others.

Market Insights & Analysis: Italy Swimming Pool Chemicals Market (2026-32):

The Italy Swimming Pool Chemicals Market size was valued at USD 30 million in 2025 and is projected to grow from USD 32.6 million in 2026 to USD 45.80 million by 2032, exhibiting a CAGR of 5.83% during the forecast period. i.e., 2026-32.

Italy’s swimming pool market has shown measurable growth driven by rising residential and commercial demand, with industry data indicating a significant expansion in installation activity over recent years. Independent estimates point to around 15,000 in‑ground residential pools sold annually and a total base of approximately 700,000 residential pool structures, highlighting a steady uptake among homeowners seeking lifestyle amenities and outdoor enhancements.

Regional adoption patterns reflect Italy’s climatic advantages and established tourism infrastructure, particularly in the leisure and wellness sectors, where facilities invest in recreational water features to attract visitors.

The public sector also contributes to broader industry scale, with over 1,150 public swimming pool venues supporting sport and community recreation in 2025. Cur rent market conditions are shaped by evolving consumer preferences for sustainable and modular solutions, as seen in design innovations such as container‑based pools that offer rapid installation and reduced environmental impact.

These trends exemplify how industry participants are diversifying offerings to appeal to both cost‑conscious residential clients and commercial investors focused on sustainability goals. Looking ahead, demographic shifts and tourism growth suggest continued opportunities for new pool installations and related services, underpinned by ongoing demand from private villa projects and hospitality investments catering to domestic and international visitors.

Italy’s broader fiscal framework for residential renovation has implications for outdoor facility development, with the 2025 “Bonus Casa” program offering up to 50% tax deductions on eligible property improvements that indirectly reduce overall renovation costs for homeowners.

Complementary building incentives like the Ecobonus remain active, providing deductions for energy efficiency upgrades that can influence decisions around pool‑related systems, such as heating or filtration, when integrated with broader home improvement work.

Although the Superbonus 110% program is being phased out or restricted, regulatory extensions through 2026 for qualifying building safety work reflect ongoing government support for residential property enhancements, which can affect adjacent outdoor infrastructure investments.

These fiscal instruments form part of a mosaic of policies aimed at stimulating construction and improving energy performance, indirectly supporting market conditions favorable to swimming pool projects as part of comprehensive home renovations and lifestyle upgrades.

The residential segment remains the predominant driver of market activity in Italy, accounting for a large share of new pool installations as families invest in home upgrades and outdoor amenities. This aligns with broader residential construction trends and reflects consumers’ emphasis on leisure, wellness, and quality of life enhancements. In the commercial segment, hospitality establishments such as resorts and wellness centers are increasingly integrating pools as value‑added services, driving demand for high‑end installations that enhance guest experience and extend seasonal usage. This segment’s investments contribute to niche growth dynamics distinct from residential patterns. Institutional and public sectors also influence market demand, with sports facilities, municipal recreation centers, and educational institutions maintaining and sometimes expanding aquatic infrastructures to support community programs and youth development. This segment supports recurring maintenance and renovation spending separate from initial construction trends.

Italy Swimming Pool Chemicals Market Scope:

| Category | Segments |

|---|---|

| By Product | (Sanitizers & Treatment Types (Sanitizers, pH Adjusters, Algaecides, Water Balancers), |

| By Form | (Tablets/Granules, Liquids, Cartridges/Pods, Other Forms), |

| By Pool Type | (Residential Pools, Commercial Pools, Public Pools), |

| By End User | (Hospitality Sector, Real Estate, Sports Facilities, Municipal Bodies, Other End Users), |

Italy Swimming Pool Chemicals Market Driver:

Strict Water Quality Regulations and Public Health Compliance Requirements

A key structural driver of the swimming pool chemicals market is the tightening of water quality and hygiene regulations across Europe, including Italy, aimed at safeguarding public health. The European Commission and national health authorities have reinforced compliance frameworks under directives such as the Bathing Water Directive and national pool safety standards, with updated monitoring protocols implemented through 2025. These regulations mandate strict control of microbial contamination, pH balance, and disinfectant levels, requiring continuous and standardized chemical treatment. As enforcement intensity increases, pool operators must adhere to measurable chemical usage benchmarks, directly expanding consumption volumes.

This regulatory pressure is significantly impacting demand across commercial and institutional segments, particularly in hotels, wellness centers, and public aquatic facilities. The Italian Ministry of Health requires routine water testing and documented compliance with sanitation thresholds, leading to recurring procurement of chlorine-based disinfectants, algaecides, an d balancing agents. Unlike discretionary spending, these chemical purchases are mandatory for operational continuity, ensuring consistent demand regardless of seasonal fluctuations. The expansion of compliance audits and certification requirements in 2025 has further intensified usage frequency, reinforcing volume-driven market growth rather than price-based expansion.

Moreover, the driver materially increases overall market size by creating recurring consumption cycles tied to regulatory adherence rather than one-time installations. Data from the World Health Organization emphasizes that improperly maintained pools pose infection risks, prompting governments to adopt stricter chemical treatment guidelines and monitoring systems. This institutionalization of water safety standards ensures that every operational pool becomes a continuous consumer of treatment chemicals. As regulatory frameworks evolve and enforcement strengthens, the swimming pool chemicals market benefits from sustained, non-discretionary demand embedded within public health infrastructure.

Italy Swimming Pool Chemicals Market Trend:

Adoption of Automated Pool Water Management Systems

A major structural trend in the swimming pool chemicals market is the rapid adoption of automated water management systems that optimize chemical dosing and monitoring. This shift has accelerated due to stricter compliance requirements and rising operational efficiency needs across commercial facilities. The European Commission has supported digitalization under its 2025 industrial strategy, encouraging smart infrastructure integration across sectors, including water systems. As a result, pool operators are increasingly deploying IoT-enabled sensors and automated dosing units to ensure real-time compliance with water quality standards.

This transition is fundamentally reshaping operational models by reducing manual intervention and enabling precise, data-driven chemical usage. Automated systems continuously measure parameters such as pH, chlorine levels, and oxidation-reduction potential, adjusting chemical inputs accordingly. For example, Fluidra provides connected solutions like Fluidra Connect, enabling real-time monitoring and remote control of pool systems, including water treatment and filtration. The system allows operators to diagnose, manage, and automate pool operations via digital platforms, improving efficiency and maintenance.

Automation enables energy savings of 40–70% and optimized equipment usage through smart scheduling and sensor-based control .

In Europe, the adoption of automated pool monitoring systems is expanding rapidly due to regulatory pressure, sustainability goals, and hospitality sector demand. The trend is expected to persist as digital water management aligns with broader European sustainability and efficiency goals. The European Environment Agency highlights the role of smart monitoring systems in improving water resource efficiency and reducing environmental impact. As regulatory frameworks increasingly emphasize traceability and performance monitoring, automation becomes essential rather than optional. This ensures sustained adoption across both commercial and high-end residential segments, structurally transforming procurement patterns and long-term demand dynamics in the swimming pool chemicals market.

Italy Swimming Pool Chemicals Market Opportunity:

Development of Eco-Friendly Chemical Alternatives for Pool Maintenance

A strong market opportunity is emerging in the development of eco-friendly chemical alternatives for pool maintenance, driven by increasingly stringent environmental and chemical safety regulations across Europe. The European Chemicals Agency has intensified substance evaluations and restrictions under REACH through 2025, particularly targeting hazardous compounds with environmental persistence. At the same time, the EU Chemicals Strategy for Sustainability is accelerating the transition toward biodegradable and low-toxicity formulations. These regulatory developments are creating a structural gap in the market for compliant, next-generation pool treatment solutions.

This opportunity is translating into tangible demand as commercial and institutional pool operators align procurement with sustainability and environmental compliance goals. A USD 217 million bond issuance in 2025 is financing the modernization of water infrastructure across Veneto. The program supports wastewater treatment upgrades, leakage reduction, and digital monitoring systems across 330 municipalities. These upgrades require improved treatment efficiency and reduced environmental impact, increasing the need for optimized chemical usage. This supports the shift toward high-performance and eco-efficient pool and water treatment chemicals.

The opportunity is particularly favorable for new and emerging players because eco-friendly formulations rely more on innovation, certification, and niche positioning than on large-scale production advantages. Unlike conventional disinfectants dominated by established manufacturers, this segment allows smaller firms to differentiate through rapid product development and compliance with evolving eco-label standards. Furthermore, increasing preference for transparent ingredient disclosure and sustainable sourcing reduces barriers for agile entrants. This creates a scalable pathway for growth, enabling new players to capture market share in an evolving, regulation-driven landscape.

Italy Swimming Pool Chemicals Market Challenge:

High Regulatory Compliance Costs and Environmental Restrictions

The most critical structural challenge in the Italy swimming pool chemicals market is the tightening regulatory framework governing chemical usage, safety, and environmental discharge. This challenge is driven by the European Union’s REACH regulation and the Biocidal Products Regulation (BPR), enforced by authorities such as the European Chemicals Agency and Italy’s Ministry of Health. Recent updates in 2025 have increased scrutiny on chlorine-based and algaecide formulations due to environmental and human health risks. For example, Biocidal Products Regulation (BPR) fees were increased by 19.5% in August 2025, directly impacting all companies placing chemical products on the EU market. Compliance now requires extensive toxicological testing, registration fees, and labelling modifications, significantly increasing operational complexity.

These regulatory requirements impose measurable financial and administrative burdens on manufacturers and distributors. According to European Commission data, BPR approval costs can exceed USD 3–5 million per active substance, with approval timelines extending beyond three years. In Italy, smaller regional suppliers have faced product withdrawals due to non-compliance , particularly in Northern regions with stricter environmental enforcement. Additionally, wastewater discharge standards aligned with the EU Water Framework Directive have increased monitoring costs for commercial pool operators, further constraining demand.

This challenge materially restricts market expansion by discouraging new entrants and limiting product innovation. High compliance costs reduce profit margins and delay product launches, particularly for eco-friendly alternatives that require new approvals. As a result, adoption rates slow, especially among small-scale operators, while investment decisions are increasingly cautious due to regulatory uncertainty and prolonged return timelines.

Italy Swimming Pool Chemicals Market (2026-32) Segmentation Analysis:

The Italy Swimming Pool Chemicals study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Product (Sanitizers & Treatment Types):

- Sanitizers

- Oxygen‑Based

- Bromine‑Based

- Chlorine‑Based

- pH Adjusters

- pH Reducers

- pH Increasers

- Algaecides

- Natural Algaecides

- Quaternary Ammonium‑Based

- Copper‑Based

- Water Balancers

- Stabilizers

- Total Alkalinity Adjusters

- Calcium Hardness Increasers

- Others

- Enzymes

- Flocculants

- Clarifiers

The chlorine-based sanitizers segment dominates the Italian swimming pool chemicals industry with a market share of around 45% due to its regulatory acceptance and proven disinfection efficiency. The World Health Organization continues to recommend chlorine as the primary disinfectant for public pools, as it effectively eliminates pathogens and maintains residual protection. This scientific validation has institutionalized chlorine usage across commercial and public facilities. As a result, demand remains structurally embedded rather than discretionary.

Industry adoption further reinforces this dominance, with leading manufacturers such as the Barchemicals Group developing specialized chemicals for swimming pool water treatment, disinfection, and sanitation, with strong investment in R&D and innovation. Hotels, wellness centers, and municipal pools rely heavily on chlorine due to its cost-effectiveness and compatibility with large-scale operations. This widespread usage creates consistent bulk demand across Italy’s pool infrastructure.

The impact on the market is significant, as chlorine-based products drive high-volume consumption cycles due to continuous replenishment requirements. Unlike alternative treatments, chlorine ensures both immediate and residual disinfection, making it indispensable under regulatory frameworks. This leads to recurring sales and stable revenue streams for suppliers. Consequently, the segment maintains long-term dominance supported by regulatory mandates, operational reliability, and scalable applications across end-user categories.

Based on the pool type:

- Residential Pools

- Commercial Pools

- Public Pools

The residential pools segment leads the Italy swimming pool chemicals market with a market share of 55%, driven by sustained growth in home improvement and private leisure investments. Around 88.8% of Italian households have outdoor space, creating high structural potential for private pool installations . This has directly increased installations of private pools, particularly in suburban and villa-based housing. The trend is structurally linked to lifestyle enhancement and long-term asset value creation.

Piscine Castiglione specializes in custom residential pool construction and has expanded projects across northern and central Italy. It highlights that pools are designed as lifestyle and home-integrated elements, emphasizing their role in gardens and private properties. Additionally, tax incentives for home renovation indirectly support pool construction, further boosting chemical demand. This ecosystem enables the continuous expansion of the residential customer base.

The market impact is evident in recurring, decentralized demand for sanitizers, algaecides, and balancing agents across thousands of individual households. Unlike commercial pools, which are fewer but larger, residential pools generate widespread and frequent consumption cycles. This increases overall market volume and ensures stable demand throughout the year. As residential ownership continues to expand, this segment remains the primary contributor to market growth and chemical consumption in Italy.

Italy Swimming Pool Chemicals Market (2026-32) Regional Analysis:

Northwest Italy leads the swimming pool chemicals market with a market share of 28% due to its unique intersection of climate advantage and tourism-driven infrastructure. Regions such as Liguria and Lombardy experience warmer seasonal conditions combined with extended tourism cycles, increasing pool usage intensity compared to other regions. According to the ISTAT, Italy recorded over 466 million overnight stays, with demand significantly concentrated in northern regions, which account for the highest share of tourism activity. This elevated occupancy in hospitality facilities directly increases pool utilization intensity, lea ding to more frequent chemical treatment cycles and higher overall consumption.

A distinctive factor reinforcing regional dominance is the concentration of wellness-oriented real estate and luxury hospitality investments. Northwest Italy has seen the continued expansion of spa resorts, boutique hotels, and agritourism properties integrating pools as core amenities. The Bank of Italy reported strong growth in high-end tourism infrastructure investment through 2024–2025, particularly in northern regions. These facilities require advanced water treatment standards, leading to consistent demand for specialized chemicals, including stabilizers and premium sanitization systems.

The Italian chemical industry is heavily concentrated in Northern Italy, accounting for 77% of total chemical employment according to CEFIC dat a. This industrial base ensures strong local availability of water treatment chemicals, supports innovation, and enables efficient supply chains, thereby strengthening the region’s leadership in the swimming pool chemicals market.

Gain a Competitive Edge with Our Italy Swimming Pool Chemicals Market Report:

- The Italy Swimming Pool Chemicals Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Italy Swimming Pool Chemicals Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Italy Swimming Pool Chemicals Market Policies, Regulations, and Product Standards

- Italy Swimming Pool Chemicals Market Trends & Developments

- Italy Swimming Pool Chemicals Market Dynamics

- Growth Factors

- Challenges

- Italy Swimming Pool Chemicals Market Hotspot & Opportunities

- Italy Swimming Pool Chemicals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Thousand Tons)

- Market Share & Outlook

- By Product (Sanitizers & Treatment Types)- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Sanitizers

- Oxygen-Based

- Bromine-Based

- Chlorine-Based

- pH Adjusters

- pH Reducers

- pH Increasers

- Algaecides

- Natural Algaecides

- Quaternary Ammonium Based

- Copper-Based

- Water Balancers

- Stabilizers

- Total Alkalinity Adjusters

- Calcium Hardness Increasers

- Others

- Enzymes

- Flocculants

- Clarifiers

- Sanitizers

- By Form- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Tablets/Granules

- Liquids

- Cartridges/Pods

- Other Forms

- By Pool Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Residential Pools

- Commercial Pools

- Public Pools

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Hospitality Sector

- Real Estate

- Sports Facilities

- Municipal Bodies

- Other End Users

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Northwest

- Northeast

- Center

- South

- Islands

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product (Sanitizers & Treatment Types)- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Market Size & Outlook

- Italy Residential Swimming Pool Chemicals Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Thousand Tons)

- Market Share & Outlook

- By Form- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Pool Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Market Size & Outlook

- Italy Commercial Swimming Pool Chemicals Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Thousand Tons)

- Market Share & Outlook

- By Form- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Pool Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Market Size & Outlook

- Italy Public Swimming Pool Chemicals Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Thousand Tons)

- Market Share & Outlook

- By Form- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Pool Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Market Size & Outlook

- Italy Swimming Pool Chemicals Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Lonza Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ecolab Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AkzoNobel N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kemira Oyj

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Solvay S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Clorox Pool & Spa

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fluidra S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Natural Chemistry

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nankai Chemical

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lonza Group

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now