India Vehicle-to-Vehicle Communication Market Research Report: Forecast (2026-2032)

India Vehicle-to-Vehicle Communication Market - By Vehicle Type (Passenger Cars, Commercial Vehicles), By Connectivity Type (Cellular-Based Technology, Dedicated Short), By Deploym ... ent Type (Original Equipment Manufacturer (OEM) devices, Aftermarket devices), By Application (Traffic Safety, Traffic Efficiency, Infotainment, Payments, Other Applications), and others Read more

- Automotive

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

India Vehicle-to-Vehicle Communication Market

Projected 10.29% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 0.64 Billion

Market Size (2032)

USD 1.28 Billion

Base Year

2025

Projected CAGR

10.29%

Leading Segments

By Connectivity Type: Cellular-Based Technology

India Vehicle-to-Vehicle Communication Market Report Key Takeaways:

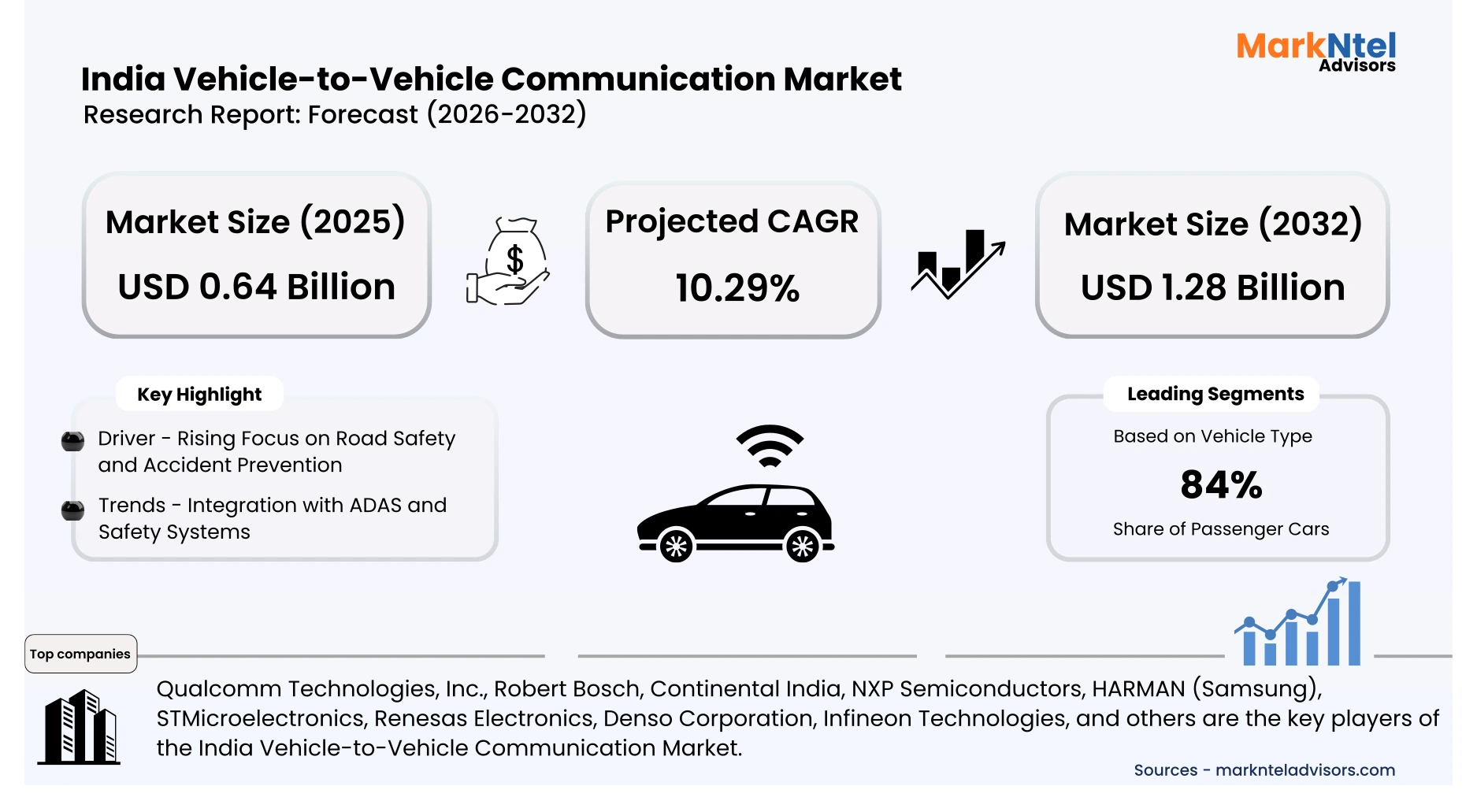

- The India Vehicle-to-Vehicle Communication Market size was valued at around USD 0.64 billion in 2025 and is projected to reach USD 1.28 billion by 2032. The estimated CAGR from 2026 to 2032 is around 10.29%, indicating strong growth.

- By vehicle type, the passenger cars represented 84% of the India Vehicle-to-Vehicle Communication Market size in 2025.

- By connectivity type, the cellular-based technology represented 76% of the India Vehicle-to-Vehicle Communication Market size in 2025.

- The leading vehicle-to-vehicle communication companies are Qualcomm Technologies, Inc., Robert Bosch, Continental India, NXP Semiconductors, HARMAN (Samsung), STMicroelectronics, Renesas Electronics, Denso Corporation, Infineon Technologies, and others.

Market Insights & Analysis: India Vehicle-to-Vehicle Communication Market (2026- 2032):

The India Vehicle-to-Vehicle Communication Market size was valued at around USD 0.64 billion in 2025 and is projected to reach USD 1.28 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 10.29% during the forecast period, i.e., 2026-32. The India Vehicle-to-Vehicle Communication Market is poised for significant growth as the nation intensifies efforts to enhance road safety and reduce traffic fatalities. India’s road accident burden remains substantial, with over 48 0,000 crashes and more than 170,000 deaths reported annually, underscoring a persistent need for advanced safety technologies. In the first half of 2025 alone, 29,018 deaths occurred on national highways, which comprise only about 2 % of the road network but account for over 30 % of fatal accidents, highlighting risks on high‑speed corridors and the potential impact of connected vehicle systems .

In response, the Ministry of Road Transport and Highways (MoRTH) is preparing to mandate V2V communication devices as standard equipment, enabling vehicles to exchange real‑time alerts on speed, braking, and hazard proximity to avert collisions. Technical standards are under finalisation, and once notified, on‑board units (OBUs) estimated at roughly USD 60–85 per vehicle will support direct communication without reliance on mobile networks. Additionally, the Department of Telecommunications has allocated dedicated 30 GHz spectrum to facilitate reliable V2V connectivity, a foundational step toward nationwide deployment .

Parallel safety initiatives, such as mandatory Advanced Emergency Braking Systems (AEBS) and lane departure warning systems from April 2026, and the Bharat NCAP 2.0 programme including ADAS evaluation from October 2027 are further strengthening the ecosystem in which V2V will operate. By integrating V2V with existing safety technologies and rolling out enabling infrastructure, India is aligning with global intelligent transportation trends, creating a conducive environment for adoption.

Overall, growing government commitment, clear regulatory direction, and harmonisation with vehicle safety standards position the market for robust growth through 2032 as connected mobility becomes mainstream.

India Vehicle-to-Vehicle Communication Market Recent Developments:

- January 2025: Qualcomm Technologies teamed up with MapMyIndia to develop connected vehicle technologies tailored for India, combining Snapdragon platforms with hyper-local maps to support affordable connectivity and safety features in mass-market vehicles.

- January 2026: The Department of Telecommunications has allocated dedicated 30 GHz radio spectrum for V2V communication, enabling direct wireless exchanges between vehicles without network dependency. This regulatory move is foundational for commercial deployment across passenger vehicles and commercial fleets.

India Vehicle-to-Vehicle Communication Market Scope:

| Category | Segments |

|---|---|

| By Vehicle Type | Passenger Cars, Commercial Vehicles |

| By Connectivity Type | Cellular-Based Technology, Dedicated Short |

| By Deployment Type | Original Equipment Manufacturer (OEM) devices, Aftermarket devices |

| By Application | Traffic Safety, Traffic Efficiency, Infotainment, Payments, Other Applications |

India Vehicle-to-Vehicle Communication Market Driver:

Rising Focus on Road Safety and Accident Prevention

India’s grave road safety situation is a principal driver of the Vehicle-to-Vehicle (V2V) communication market. According to data from the Ministry of Road Transport and Highways (MoRTH), India recorded over 480,000 road accidents and approximately 172,000 fatalities in 2023, marking a year-on-year increase in both incidents and deaths. On average, this translates to about 1,317 crashes and 474 deaths per day, or roughly 55 accidents and 20 fatalities every hour. Pedestrians and two-wheeler users accounted for nearly half of the fatalities, illustrating vulnerability among road users. India’s reported road death rate of 250 per 10,000 km surpasses that of the United States, China, and Australia, underscoring systemic safety gaps and reflecting the urgency of preventive solutions .

The Government of India has committed to reducing road fatalities by 50% by 2030 under various national road safety strategies, including enforcement, infrastructure improvement, and intelligent transport system deployment . Investment plans beyond 2025 include scaling emergency response networks, digital traffic enforcement, and advanced driver assistance technologies, which amplify the relevance of V2V systems in future mobility frameworks.

Overall, persistent high accident and fatality rates, alongside strong national safety targets and investment plans, are forcing stakeholders to adopt V2V technologies as a critical intervention. These factors are expected to significantly accelerate market growth in the coming years.

India Vehicle-to-Vehicle Communication Market Trend:

Integration with ADAS and Safety Systems

A major trend in the India Vehicle‑to‑Vehicle (V2V) Communication Market is its integration with Advanced Driver Assistance Systems (ADAS) and related safety technologies, driven by rising safety priorities and supportive policy outlooks. Government‑linked reports and analyses indicate that ADAS adoption in India is rapidly increasing; penetration rose from approximately 6.2 % in H1 2024 to 8.3 % in H1 2025 in passenger vehicles, reflecting a 33 % year‑on‑year increase as manufacturers equip more models with lane departure warnings, collision alerts, and adaptive cruise control systems . These driver assistance features provide crucial real‑time monitoring and hazard mitigation capabilities that complement and enhance V2V communication by sharing contextual safety data between vehicles.

National think‑tank NITI Aayog projects that ADAS presence in new vehicle sales could reach 90 % by 2030, supported by regulatory encouragement and consumer demand for safer mobility . Governmental emphasis on road safety has also elevated connected safety standards as part of broader intelligent mobility ecosystems. The combined deployment of ADAS with V2V communication increases predictive awareness, automates risk response, and reduces the likelihood of serious crashes. Consequently, this technological convergence is expected to accelerate market growth as OEMs and regulators prioritize integrated safety solutions in future vehicle platforms.

India Vehicle-to-Vehicle Communication Market Challenge:

High Implementation Costs

One of the foremost challenges confronting the India Vehicle-to-Vehicle (V2V) communication market is the high cost of implementation in a price-sensitive automotive ecosystem. Government advisories estimate that fitting each vehicle with an On-Board Unit (OBU) for V2V communication will cost roughly USD 60–85, excluding installation and integration expenses for manufacturers. This hardware cost, when added to other connected technologies such as Advanced Driver Assistance Systems (ADAS), raises the overall vehicle price, which can deter buyers, especially in the mass market where affordability is key .

Beyond per-vehicle costs, broader rollout demands significant program investment. Reports indicate the nationwide V2V implementation project could reach an estimated USD 600 million. outlay to develop standards, infrastructure, and phased deployment . Such upfront public and private sector investment underscores the financial barriers at scale.

Additionally, integrating V2V with existing vehicle systems and ensuring interoperability across brands demands further R&D and testing outlays, which can strain smaller OEMs and suppliers. Until technology costs decline through economies of scale or policy incentives, these financial burdens will continue to restrain accelerated adoption.

In summary, substantial equipment and program costs challenge widespread implementation, particularly in budget vehicle segments, potentially slowing market expansion.

India Vehicle-to-Vehicle Communication Market (2026-32) Segmentation Analysis:

The India Vehicle-to-Vehicle Communication Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Vehicle Type:

- Passenger Cars

- Commercial Vehicles

Passenger cars dominate the market with an estimated 84% share due to their high production volumes and faster adoption of connected vehicle technologies. Automakers increasingly integrate advanced connectivity solutions in passenger vehicles to enhance safety, navigation, infotainment, and overall driving experience. Growing consumer demand for features such as real-time traffic updates, emergency assistance, vehicle diagnostics, and in-car digital payments has accelerated deployment in this segment.

In addition, rising urbanization, increasing disposable income, and supportive government regulations related to road safety and intelligent transportation systems have further strengthened passenger car adoption. Compared to commercial vehicles, passenger cars also experience shorter technology upgrade cycles, enabling quicker penetration of new connectivity solutions across mass-market models.

Based on Connectivity Type:

- Cellular-Based Technology

- Dedicated Short- Range Communication(DSRC)

Cellular-based technology leads with a 76% share owing to its wide coverage, scalability, and compatibility with existing telecom infrastructure. Unlike DSRC, cellular connectivity supports long-range communication, real-time data exchange, and seamless integration with cloud platforms. The rapid rollout of 4G and 5G networks has significantly improved latency, reliability, and data transmission speeds, making cellular solutions ideal for connected and autonomous vehicle applications. Moreover, strong backing from telecom operators, automakers, and technology providers has accelerated commercialization. Cellular-based systems also enable over-the-air updates, advanced infotainment, and V2X communication, reinforcing their dominance in the market.

India Vehicle-to-Vehicle Communication Market (2026-32): Regional Projection

The India vehicle-to-vehicle communication market is dominated by Tier-1 urban regions, particularly Delhi-NCR, Bengaluru, Mumbai, Chennai, and Pune. These regions lead adoption due to high vehicle density, advanced road infrastructure, and a stronger presence of connected mobility pilots. Major automotive OEMs, technology providers, and telecom operators actively test V2V and V2X solutions in these cities to address congestion, accident reduction, and traffic management challenges. Government-backed smart city initiatives and intelligent transport system projects further support deployment in metro regions.

In addition, higher penetration of premium and mid-segment passenger vehicles equipped with advanced driver assistance systems accelerates V2V integration. Cities such as Bengaluru and Pune also benefit from strong automotive R&D ecosystems and proximity to manufacturing hubs. Compared to Tier-2 and rural regions, Tier-1 cities have better 4G and emerging 5G connectivity, which is critical for low-latency communication. As a result, these regions currently account for the majority of market demand nationwide.

Gain a Competitive Edge with Our India Vehicle-to-Vehicle Communication Market Report:

- India Vehicle-to-Vehicle Communication Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- India Vehicle-to-Vehicle Communication Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- India Vehicle-to-Vehicle Communication Market Policies, Regulations, and Product Standards

- India Vehicle-to-Vehicle Communication Market Supply Chain Analysis

- India Vehicle-to-Vehicle Communication Market Trends & Developments

- India Vehicle-to-Vehicle Communication Market Dynamics

- Growth Drivers

- Challenges

- India Vehicle-to-Vehicle Communication Market Hotspot & Opportunities

- India Vehicle-to-Vehicle Communication Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Vehicle Type- Market Size & Forecast 2022-2032F, USD Million

- Passenger Cars

- Commercial Vehicles

- By Connectivity Type- Market Size & Forecast 2022-2032F, USD Million

- Cellular-Based Technology

- Dedicated Short- Range Communication(DSRC)

- By Deployment Type- Market Size & Forecast 2022-2032F, USD Million

- Original Equipment Manufacturer (OEM) devices

- Aftermarket devices

- By Application- Market Size & Forecast 2022-2032F, USD Million

- Traffic Safety

- Traffic Efficiency

- Infotainment

- Payments

- Other Applications

- By Region

- North

- South

- West

- East

- North-East

- By Company

- Company Revenue Shares

- Competitor Characteristics

- By Vehicle Type- Market Size & Forecast 2022-2032F, USD Million

- Market Size & Outlook

- Cellular-Based Technology Vehicle-to-Vehicle Communication Market Outlook, 2022-2032

- Market Size & Analysis

- Market Share & Analysis

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Deployment Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- Dedicated Short- Range Vehicle to Vehicle Communication Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Million)

- Market Share & Analysis

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Deployment Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- India Vehicle-to-Vehicle Communication Market Key Strategic Imperatives for Success & Growth

- Competition Outlook

- Company Profiles

- Qualcomm Technologies, Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Robert Bosch

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Continental India

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- NXP Semiconductors

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- HARMAN (Samsung)

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- STMicroelectronics

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Renesas Electronics

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Denso Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Infineon Technologies

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Qualcomm Technologies, Inc.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now