India Feed Additives Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Additive Type (Amino Acids (Lysine, Methionine, Threonine, Tryptophan), Phosphates (Monocalcium Phosphate, Dicalcium Phosphate, Mono-Dicalcium Phosphate, Defluorinated Phosphate ... , Tricalcium Phosphate, Others), Vitamins (Fat-Soluble, Water-Soluble), Acidifiers (Propionic Acid, Formic Acid, Citric Acid, Lactic Acid, Sorbic Acid, Malic Acid, Acetic Acid, Others), Carotenoids (Astaxanthin, Canthaxanthin, Lutein, Beta-Carotene), Enzymes (Phytase, Protease, Others), Mycotoxin Detoxifiers (Binders, Modifiers), Flavors and Sweeteners (Flavors, Sweeteners), Antibiotics (Tetracycline, Penicillin, Others), Minerals (Potassium, Calcium, Phosphorus, Magnesium, Sodium, Iron, Zinc, Copper, Manganese, Others), Antioxidants (Bha, Bht, Ethoxyquin, Others), Non-Protein Nitrogen (Urea, Ammonia, Others), Preservatives (Mold Inhibitors, Anticaking Agents), Phytogenics (Essential Oils, Herbs and Spices, Oleoresin, Others), Probiotics (Lactobacilli, Stretococcus Thermophilus, Bifidobacteria, Yeast)), By Form (Liquid, Powder, Granules), By Livestock (Poultry, Ruminant, Swine, Aquaculture, Companion Animal), and others Read more

- Chemicals

- Feb 2026

- Pages 130

- Report Format: PDF, Excel, PPT

India Feed Additives Market

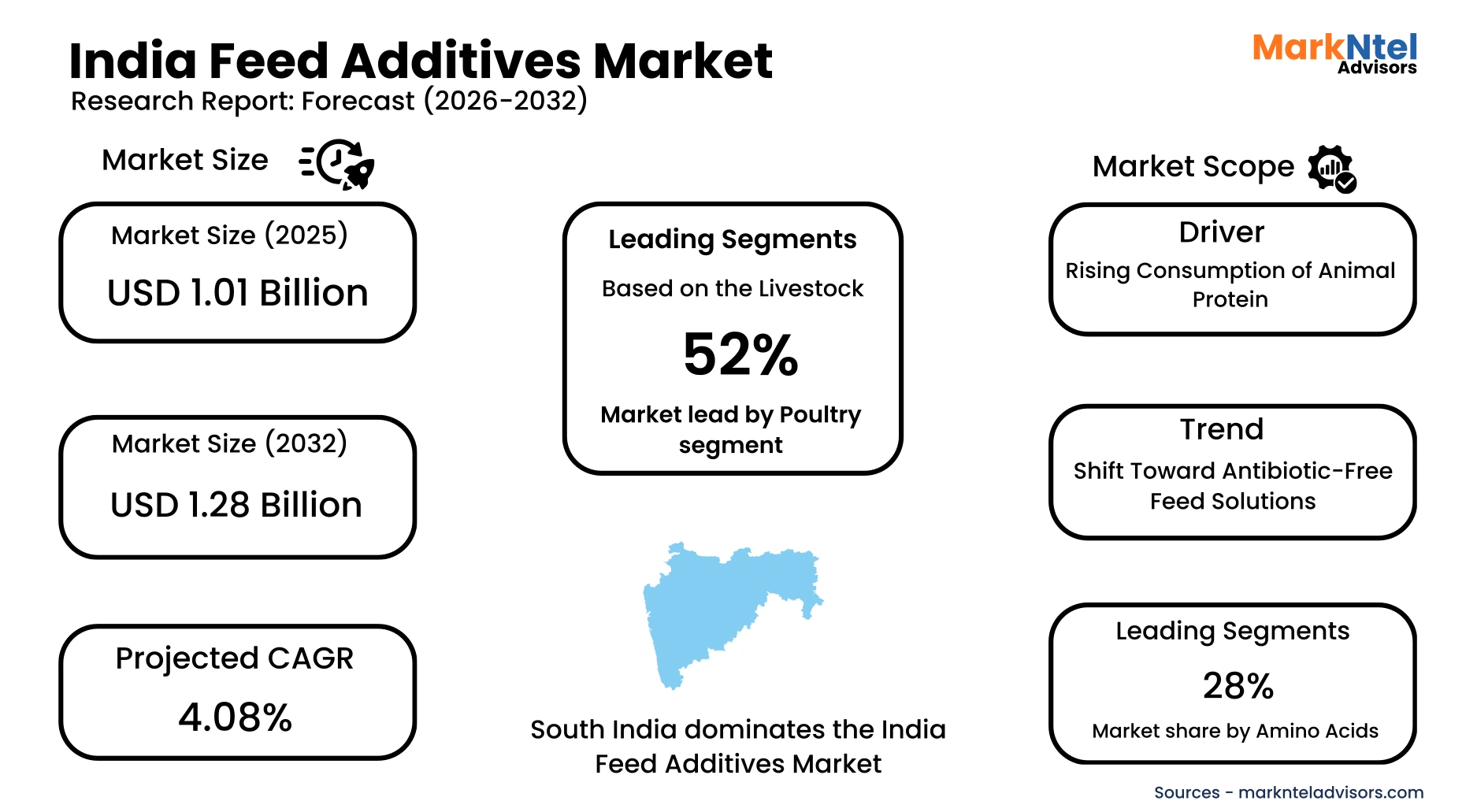

Projected 4.08% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 1.01 Billion

Market Size (2032)

USD 1.28 Billion

Base Year

2025

Projected CAGR

4.08%

Leading Segments

By Livestock: Poultry

India Feed Additives Market Report Key Takeaways:

- Market size is estimated at USD 1.01 billion in 2025 and is projected to reach USD 1.28 billion by 2032. The estimated CAGR from 2026 to 2032 is around 4.08%, indicating strong growth.

- The South India is dominating this market by accounting 35% market share in 2026.

- By Additive Type, the Amino Acid segment represented a significant share of about 28% in the India Feed Additives Market in 2026.

- By Livestock, the Poultry segment represented a significant share of about 52% in the India Feed Additives Market in 2026.

- Leading feed additives companies in India are Adisseo, Archer Daniel Midland Co., BASF SE, Alltech, Inc., Cargill Inc., DSM Nutritional Products AG, Solvay S.A., IFF (Danisco Animal Nutrition), Kerry Group Plc, SHV (Nutreco NV), Evonik Industries AG, Elanco Animal Health Inc., Novus International, Inc., and Others.

Market Insights & Analysis: India Feed Additives Market (2026-32):

The India Feed Additives Market size is estimated at USD 1.01 billion in 2026 and is projected to reach USD 1.28 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 4.08% during the forecast period, i.e., 2026-32.

India’s feed additives market has grown alongside sustained expansion in livestock production and protein consumption, with milk output increasing to nearly 248 million tonnes in 2024-25, up ~3.7% from the previous year, reinforcing India’s status as the world’s largest milk producer . This structural growth has underpinned demand for nutrient enhancers and digestive aids in commercial feed formulations to support intensification across poultry and dairy sectors. Demographic shifts towards urban diets with higher animal protein intake have further supported this trend, consistent with rising poultry, egg, and meat production reported in national livestock statistics reports.

Current market conditions in 2025–2026 reflect a more formalized and quality-driven feed environment. Government programs such as the National Livestock Mission and the Animal Husbandry Infrastructure Development Fund (AHIDF) continue to provide capital and infrastructure support aimed at enhancing productivity, biosecurity, and feed mill modernization across states. These initiatives are outlined in official policy reviews emphasizing livestock gross value added and improved distribution networks. Such policy frameworks have encouraged feed manufacturers and integrators to adopt precision nutrition solutions, driving broader uptake of additives like amino acids, enzymes, and mycotoxin binders .

End-user demand in India’s feed additives market is significantly supported by export-oriented aquaculture production. According to FY2024–25 official data, India’s total seafood exports reached USD7.38 billion, amounting to 1.78 million metric tonnes, reflecting the scale of feed-intensive aquaculture operations. Frozen shrimp remained the leading export category, contributing USD4.88 billion, accounting for 66% of total seafood export earnings. The dominance of shrimp exports reinforces sustained domestic demand for high-performance aquafeed incorporating enzymes, probiotics, amino acids, and mycotoxin detoxifiers to maintain productivity, disease resilience, and export-grade quality standards.

Looking forward, supportive policy and industry responses are expected to sustain growth beyond 2026. Recent budget allocations increased funding for animal husbandry and allied infrastructure, including veterinary services, cooperatives, and feed distribution incentives, directly strengthening rural feed markets and supply chains. Government tax incentives for cooperatives and integrated livestock enterprises further lower operational costs and promote adoption of advanced feed inputs. Coupled with ongoing private sector investments in localized manufacturing and nutrition innovation, these economic, regulatory, and demographic drivers collectively position India’s feed additives market for continued expansion in the medium term .

India Feed Additives Market Recent Developments:

- 2025 : dsm-firmenich inaugurated a new feed additive manufacturing plant in Jadcherla, Hyderabad, boosting local production of mycotoxin management solutions such as Mycofix Secure and Shield. The facility supports India’s growing demand for quality additives under the Make in India initiative.

- 2025 : Alembic Pharmaceuticals, in partnership with Amlan International, launched MinerTox-Z and MinerTox-A in India to protect poultry from toxins and enhance productivity, reinforcing sustainable poultry farming.

India Feed Additives Market Scope:

| Category | Segments |

|---|---|

| By Additive Type | (Amino Acids (Lysine, Methionine, Threonine, Tryptophan), Phosphates (Monocalcium Phosphate, Dicalcium Phosphate, Mono-Dicalcium Phosphate, Defluorinated Phosphate, Tricalcium Phosphate, Others), Vitamins (Fat-Soluble, Water-Soluble), Acidifiers (Propionic Acid, Formic Acid, Citric Acid, Lactic Acid, Sorbic Acid, Malic Acid, Acetic Acid, Others), Carotenoids (Astaxanthin, Canthaxanthin, Lutein, Beta-Carotene), Enzymes (Phytase, Protease, Others), Mycotoxin Detoxifiers (Binders, Modifiers), Flavors and Sweeteners (Flavors, Sweeteners), Antibiotics (Tetracycline, Penicillin, Others), Minerals (Potassium, Calcium, Phosphorus, Magnesium, Sodium, Iron, Zinc, Copper, Manganese, Others), Antioxidants (Bha, Bht, Ethoxyquin, Others), Non-Protein Nitrogen (Urea, Ammonia, Others), Preservatives (Mold Inhibitors, Anticaking Agents), Phytogenics (Essential Oils, Herbs and Spices, Oleoresin, Others), Probiotics (Lactobacilli, Stretococcus Thermophilus, Bifidobacteria, Yeast)), |

| By Form | (Liquid, Powder, Granules), |

| By Livestock | (Poultry, Ruminant, Swine, Aquaculture, Companion Animal), |

India Feed Additives Market Driver:

Rising Consumption of Animal Protein

Rising consumption of animal protein remains the most influential structural driver of India’s feed additives market, directly expanding livestock production and compound feed volumes. In FY2024–25, India produced nearly 248 million tonnes of milk, up 3.7% year-on-year, while egg production reached 149.11 billion units, according to official government releases. Total meat output stood at approximately 10.50 million tonnes, reflecting sustained growth in poultry and livestock sectors . These measurable increases confirm expanding protein demand rather than temporary price-driven fluctuations.

The intensification of this driver is closely linked to demographic expansion, urban dietary diversification, and improved supply-chain infrastructure. Per capita egg availability rose to around 106 eggs annually in 2024–25, indicating broader household-level dietary shifts. Poultry meat now accounts for roughly half of India’s total meat production, reinforcing the scale of feed-dependent growth. As commercial poultry integrators, dairy cooperatives, and aquaculture producers expand operations, feed production rises proportionally, increasing inclusion rates of amino acids, enzymes, vitamins, and toxin management solutions.

The volumetric impact is reinforced by supportive policy measures that expand livestock infrastructure capacity. The Government of India has extended the Animal Husbandry Infrastructure Development Fund (AHIDF) through 2025–26 with an outlay of approximately USD 3.6 billion, aimed at financing feed plants, dairy processing, and meat infrastructure with interest subvention support . This capital infusion strengthens organized feed manufacturing and cold-chain logistics, directly sustaining additive consumption. Consequently, rising animal protein demand translates into durable, system-wide increases in feed and additive volumes rather than short-term adoption cycles.

India Feed Additives Market Trend:

Shift Toward Antibiotic-Free Feed Solutions

The trend toward antibiotic-free feed solutions emerged as a defining structural shift in India’s feed additives market due to intensified regulatory action and public health concerns over antimicrobial resistance (AMR). In 2024, the Food Safety and Standards Authority of India (FSSAI) amended its Contaminants, Toxins, and Residues Regulations to prohibit antibiotic use at any stage of producing milk, meat, poultry, eggs, and aquaculture starting in 2025, banning several antibiotic classes and specific drugs such as chloramphenicol and colistin. These measures directly address rising AMR risks documented by surveillance data and enforcement directives to safeguard public health and food safety.

This shift is causing structural changes across the animal nutrition value chain, as commercial feed manufacturers and livestock producers increasingly adopt alternatives such as probiotics, phytogenics, organic acids, and enzyme-based additives to replace antibiotics. As per the Indian Network for Fishery and Animal Antimicrobial Resistance shows high resistance levels in bacteria from poultry and aquaculture sources, reinforcing the urgency of reducing antibiotic use while maintaining productivity through safer additive options. These developments are prompting firms to reformulate products and enhance biosecurity measures on farms .

The antibiotic-free trend is expected to persist long-term due to sustained regulatory enforcement and export compliance requirements. India’s joint regulatory actions, including coordinated AMR monitoring by the drug regulator, Department of Animal Husbandry, and Ministry of Fisheries, further institutionalize responsible antimicrobial use across sectors. As exporters and domestic consumers demand safer food products, the structural shift toward non-antibiotic nutrient solutions will continue to shape the feed additives market and influence industry strategies well beyond short-term cycles .

India Feed Additives Market Opportunity:

Expansion of Organized Aquafeed Industry

The rapid formalization of India’s aquaculture sector presents a compelling structural opportunity for new entrants in the feed additives market due to sustained government support and productivity gains. Under the Pradhan Mantri Matsya Sampada Yojana (PMMSY), the Government of India has approved a centrally sponsored investment of around USD 2.74 billion toward holistic development of fisheries and aquaculture, including infrastructure modernization and value-chain improvement. The scheme was extended through FY2025–26 to support organized aquaculture growth and entrepreneurial participation.

This opportunity exists because aquaculture is shifting from fragmented, small-scale operations to organized, intensively managed production systems that require scientifically formulated feeds. Enhanced productivity and traceability supported by PMMSY have increased the adoption of compound feed, directly driving demand for performance-enhancing additives such as probiotics, enzymes, amino acids, and toxin binders. Productivity gains reported under PMMSY initiatives, including improved aquaculture output and cluster development models, further strengthen commercial feed usage .

The organized aquafeed segment is particularly advantageous for emerging players because it still accommodates specialization and technical differentiation. Unlike the mature poultry feed market dominated by large incumbents, aquaculture nutrition solutions vary significantly by species, region, and production intensity. Smaller firms can compete by offering customized additive blends, localized technical support, and sector-specific innovations. With PMMSY emphasizing private sector participation and cluster-based competitiveness, new entrants can capture scalable growth opportunities in a structurally expanding segment.

India Feed Additives Market Challenge:

Low Awareness in Unorganized Livestock Sector

Low awareness and limited formalization within India’s unorganized livestock sector remain a structural barrier to feed additive market expansion. According to the Government of India’s Basic Animal Husbandry Statistics 2024, a significant proportion of dairy animals are reared by smallholder households owning two to three animals, indicating fragmented production systems. While milk output reached nearly 248 million tonnes in FY2024–25, much of this production originates from small farms with limited exposure to scientific feed practices. This structural fragmentation constrains systematic adoption of advanced nutritional inputs .

The challenge persists because extension services and technical advisory penetration remain uneven across rural regions. Although the Animal Husbandry Infrastructure Development Fund, with an allocation of approximately USD 3.6 billion through 2025–26, supports modernization of feed plants and value chains, benefits are concentrated in organized segments. Small farmers often rely on traditional feeding methods such as crop residues rather than compound feed formulations. As a result, awareness of probiotics, amino acids, and enzyme supplementation remains comparatively low outside commercial poultry and aquaculture clusters.

This constraint materially limits market scalability by reducing additive inclusion rates across a vast livestock base. Market participants face higher customer acquisition costs and slower adoption cycles when targeting dispersed rural producers. Limited purchasing power and knowledge gaps further discourage investment in premium nutritional solutions. Consequently, despite strong livestock output growth, incomplete formalization in the unorganized sector restricts full realization of additive demand potential.

India Feed Additives Market (2026-32) Segmentation Analysis:

The India Feed Additives Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Additive Type:

- Amino Acids

- Phosphates

- Vitamins

- Acidifiers

- Carotenoids

- Enzymes

- Mycotoxin Detoxifiers

- Flavors and Sweeteners

- Antibiotics

- Minerals

- Antioxidants

- Non-Protein Nitrogen

- Preservatives

- Phytogenics

- Probiotics

The Amino Acids segment dominates the India Feed Additives Market with approximately 28% market share because it is structurally embedded in high-volume poultry feed production, which represents the most commercialized livestock segment in the country. According to the Agricultural and Processed Food Products Export Development Authority (APEDA), India’s poultry product exports, including processed meat and eggs, have shown steady expansion in recent years, reinforcing the need for scientifically balanced feed. Commercial broiler systems depend on lysine and methionine supplementation to achieve optimal feed conversion and rapid weight gain .

The dominance of amino acids is further supported by feed cost optimization strategies adopted by organized integrators. The Indian Council of Agricultural Research (ICAR) has emphasized balanced protein nutrition and amino acid fortification to improve nitrogen utilization efficiency in poultry diets. By lowering crude protein inclusion while maintaining growth performance, amino acids help reduce feed formulation costs, particularly during periods of soybean and maize price volatility . This cost-efficiency mechanism drives consistent and recurring bulk demand across feed mills.

Additionally, India’s compound feed production continues to expand alongside intensification of livestock systems, especially in southern poultry clusters. Amino acids are standard inclusions across virtually all commercial feed formulations, unlike specialized additives used selectively for disease or preservation. Their universal applicability, high inclusion volume, and measurable impact on productivity and export competitiveness position amino acids as the leading additive type in the India feed additives market.

Based on the Livestock:

- Aquaculture

- Poultry

- Ruminant

- Swine

- Companion Animal

The Poultry segment dominates the India Feed Additives Market, accounting for approximately 52% of total market size, because it represents the most organized, feed-intensive, and commercially integrated livestock category in the country. Poultry production operates largely through vertically integrated systems where compound feed is standardized and nutritionally optimized, resulting in high and consistent additive inclusion rates. Unlike dairy and small ruminant farming, which still rely partly on traditional feeding practices, poultry production depends almost entirely on scientifically formulated feed, making additive consumption structurally embedded in the value chain.

India’s poultry industry continues to expand in response to rising protein consumption and urban dietary shifts. Broiler production cycles are short, typically 35–45 days, leading to multiple production batches annually and repeated feed procurement cycles. Each production cycle requires balanced formulations containing amino acids, enzymes, vitamins, probiotics, and toxin binders to achieve optimal feed conversion and weight gain. This high turnover rate generates significantly greater additive volume per animal compared to cattle or small ruminants, reinforcing poultry’s disproportionate contribution to total additive demand.

Additionally, the economies of scale and operational intensity of integrated poultry operations favor precision nutrition inputs. Large poultry integrators invest heavily in feed mill automation, quality control, and cost optimization, driving systematic and bulk procurement of additives. Earlier modernization of poultry feed infrastructure continues to support recurring demand, including reformulation, performance enhancement, and export-compliant production standards. Consequently, the combination of high feed dependency, rapid production cycles, organized industry structure, and scalable commercial operations positions poultry as the dominant livestock segment in India’s feed additives market.

India Feed Additives Market (2026-32): Regional Projection

South India dominates the India Feed Additives Market, holding around 35% of total market size, because it represents the country’s most feed-intensive and commercially organized livestock production hub. States such as Andhra Pradesh, Tamil Nadu, and Karnataka host dense clusters of integrated poultry farms, commercial feed mills, and aquaculture operations. Andhra Pradesh alone leads India’s aquaculture output, with fish production contributing significantly to the national total of 197.75 lakh tonnes in FY2024–25, reinforcing high compound feed consumption in the region. The concentration of scientifically managed farms results in structurally higher additive inclusion rates compared to other regions .

This dominance is further supported by South India’s leadership in organized poultry production. Tamil Nadu and Andhra Pradesh are among the top egg-producing states, supported by vertically integrated broiler and layer operations that depend on precision feed formulations. High commercial feed penetration ensures routine use of amino acids, enzymes, probiotics, and mycotoxin binders across production cycles. Unlike northern dairy-dominated states where traditional feeding remains prevalent, southern livestock systems rely heavily on standardized compound feed, increasing additive volumes.

Additionally, South India benefits from established feed manufacturing infrastructure and port connectivity that supports export-oriented aquaculture and poultry processing. The region’s proximity to major seafood export hubs enhances compliance-driven feed quality standards and advanced nutritional practices. Earlier investments in integrated poultry supply chains and aquaculture clusters continue to generate recurring demand for feed additives. Consequently, the combination of concentrated livestock density, organized feed manufacturing, export linkage, and high commercial adoption positions South India as the dominant regional contributor to India’s feed additives market growth.

Gain a Competitive Edge with Our India Feed Additives Market Report:

- India Feed Additives Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- India Feed Additives Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- India Feed Additives Market Policies, Regulations, and Product Standards

- India Feed Additives Market Trends & Developments

- India Feed Additives Market Dynamics

- Growth Factors

- Challenges

- India Feed Additives Market Hotspot & Opportunities

- India Feed Additives Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Additive Type- Market Size & Forecast 2022-2032, USD Million

- Amino Acids

- Lysine

- Methionine

- Threonine

- Tryptophan

- Phosphates

- Monocalcium Phosphate

- Dicalcium Phosphate

- Mono-Dicalcium Phosphate

- Defluorinated Phosphate

- Tricalcium Phosphate

- Others

- Vitamins

- Fat-Soluble

- Water-Soluble

- Acidifiers

- Propionic Acid

- Formic Acid

- Citric Acid

- Lactic Acid

- Sorbic Acid

- Malic Acid

- Acetic Acid

- Others

- Carotenoids

- Astaxanthin

- Canthaxanthin

- Lutein

- Beta-Carotene

- Enzymes

- Phytase

- Protease

- Others

- Mycotoxin Detoxifiers

- Binders

- Modifiers

- Flavors and Sweeteners

- Flavors

- Sweeteners

- Antibiotics

- Tetracycline

- Penicillin

- Others

- Minerals

- Potassium

- Calcium

- Phosphorus

- Magnesium

- Sodium

- Iron

- Zinc

- Copper

- Manganese

- Others

- Antioxidants

- Bha

- Bht

- Ethoxyquin

- Others

- Non-Protein Nitrogen

- Urea

- Ammonia

- Others

- Preservatives

- Mold Inhibitors

- Anticaking Agents

- Phytogenics

- Essential Oils

- Herbs and Spices

- Oleoresin

- Others

- Probiotics

- Lactobacilli

- Stretococcus Thermophilus

- Bifidobacteria

- Yeast

- Amino Acids

- By Form- Market Size & Forecast 2022-2032, USD Million

- Liquid

- Powder

- Granules

- By Livestock- Market Size & Forecast 2022-2032, USD Million

- Poultry

- Ruminant

- Swine

- Aquaculture

- Companion Animal

- By Region - Market Size & Forecast 2022-2032, USD Million

- North India

- East India

- West and Central India

- South India

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Additive Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Poultry Feed Additives Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Livestock- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Ruminant Feed Additives Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Livestock- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Swine Feed Additives Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Livestock- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Aquaculture Feed Additives Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Livestock- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Companion Animal Feed Additives Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Livestock- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Feed Additives Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Adisseo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Archer Daniel Midland Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alltech, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cargill Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DSM Nutritional Products AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Solvay S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IFF (Danisco Animal Nutrition)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kerry Group Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SHV (Nutreco NV)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Evonik Industries AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elanco Animal Health Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Novus International, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Adisseo

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now