India Diagnostic Labs Market Research Report: Forecast (2026-2032)

India Diagnostic Labs Market - By Test Type (Pathology, Radiology & Imaging), By Pathology Test Type (Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopath ... ology & Cytopathology, Molecular Diagnostics, Genetic Testing), By Radiology Type (X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others), By Service Delivery Mode (Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units), By Disease Type (Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others), By End-User (Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions), and others Read more

- Healthcare

- Feb 2026

- Pages 138

- Report Format: PDF, Excel, PPT

India Diagnostic Labs Market

Projected 10.42% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 18.55 Billion

Market Size (2032)

USD 37.13 Billion

Base Year

2025

Projected CAGR

10.42%

Leading Segments

By End-User: Hospitals

India Diagnostic Labs Market Report Key Takeaways:

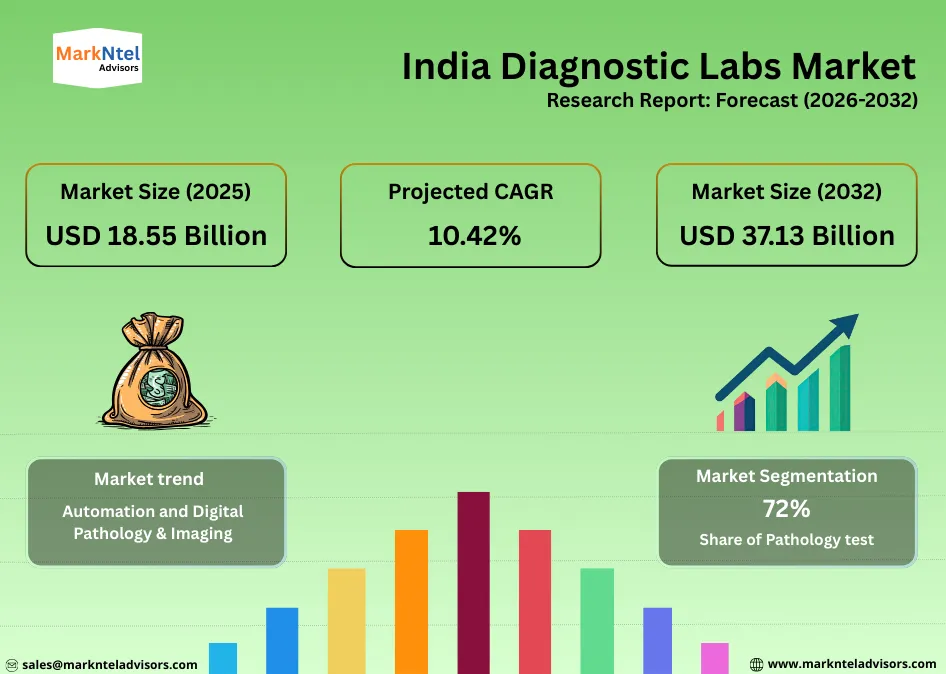

- Market size was valued at around USD18.55 billion in 2025 and is projected to reach USD37.13 billion by 2032. The estimated CAGR from 2026 to 2032 is around 10.42%, indicating strong growth.

- North India holds the largest market share of about 33% in the India Diagnostic Labs Market in 2025. Delhi NCR holds a substantial market share of about 16%.

- By Test Type, the Pathology Test segment seized a significant share of about 72% in 2025.

- By End-User, the Independent Diagnostic Centers captured a market share of around 42% in 2025.

- Leading Diagnostic Labs Companies in the India Market are Dr. Lal PathLabs, Thyrocare Technologies, Metropolis Healthcare, SRL Diagnostics, Apollo Diagnostics, Vijaya Diagnostic Centre, Pathkind Labs, Healthians, Aarthi Scans & Labs, Oncquest Laboratories, Suburban Diagnostics, Max Lab, Redcliffe Labs, Lifeline Diagnostics, Lucid Medical Diagnostics, and Others.

Market Insights & Analysis: India Diagnostic Labs Market (2026-32):

The India Diagnostic Labs Market size was valued at around USD18.55 billion in 2025 and is projected to reach USD37.13 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 10.42% during the forecast period, i.e., 2026-32.

The growth trajectory reflects rapid urban diagnostics penetration combined with a structural shift in healthcare utilization. Diagnostic demand is increasingly moving away from episodic, symptom-driven testing toward preventive, bundled, and long-term disease monitoring services. Volume-led pricing models adopted by organized lab chains have simultaneously improved affordability and expanded access across Tier II and Tier III cities.

Market dynamics are fundamentally anchored in disease prevalence, infrastructure expansion, and digital enablement. According to the Ministry of Health and Family Welfare, non-communicable diseases account for over 60% of total mortality in India , directly increasing recurring demand for pathology and imaging diagnostics. This disease burden is further amplified by public healthcare programs, as Ayushman Bharat-linked diagnostics coverage continues to channel higher patient volumes toward empaneled private laboratories. In parallel, widespread adoption of LIS platforms and home-collection logistics has structurally reduced per-test costs while improving turnaround time and patient convenience.

Moreover, between 2023 and 2025, organized diagnostic chains announced cumulative capital expenditure worth billions of dollars, focused on greenfield laboratories, automated pathology hubs, and regional reference facilities. Complementing private investments, state governments in Maharashtra, Tamil Nadu, Telangana, and Gujarat have expanded PPP-based diagnostic centers under district hospital modernization initiatives, allowing capacity scale-up without proportional increases in public capital spending.

The sustainability of the market growth is reinforced by rising test intensity per patient, growing adoption of preventive health packages, and long-term corporate wellness contracts. Additionally, import substitution in diagnostic reagents and consumables has improved cost stability and margin resilience for large operators. The convergence of radiology digitization, AI-assisted imaging workflows, and high-throughput pathology automation enables scalable expansion without linear growth in manpower, strengthening the long-term structural outlook of the Indian diagnostic labs market.

India Diagnostic Labs Market Recent Developments:

- 2025 : Dr. Lal PathLabs expanded its network by adding 18 new laboratories and nearly 900 sample-collection centers across India, and announced plans for further expansion with around 15–20 new labs and 700–800 centers to boost diagnostic access.

India Diagnostic Labs Market Scope:

| Category | Segments |

|---|---|

| By Test Type | Pathology, Radiology & Imaging |

| By Pathology Test Type | Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopathology & Cytopathology, Molecular Diagnostics, Genetic Testing |

| By Radiology Type | X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others |

| By Service Delivery Mode | Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units |

| By Disease Type | Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others |

| By End-User | Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions |

India Diagnostic Labs Market Driver:

Rising Chronic Disease Burden

India’s expanding chronic disease burden is rapidly shaping the diagnostic labs market. According to the Indian Council of Medical Research, India has over 101 million diabetics and 315 million hypertensive patients , creating continuous demand for pathology-led diagnostics, including blood chemistry, endocrinology, and cardiac panels. This transforms diagnostics from episodic testing into a recurring healthcare necessity.

Additionally, cancer diagnostics are equally influential. As per the National Cancer Registry Programme, India records over 1.4 million new cancer cases annually , driving demand for histopathology, molecular diagnostics, and imaging-based screening. Diagnostic laboratories are investing heavily in oncology-focused platforms to support early detection and treatment monitoring, especially in urban and semi-urban regions.

Moreover, public health policy further reinforces testing volumes. Ayushman Bharat has expanded coverage to over 550 million beneficiaries , increasing government-funded diagnostic utilization across empaneled private labs. Furthermore, national screening programs for tuberculosis, hepatitis, and non-communicable diseases are systematically increasing sample inflows into organized diagnostic networks.

India Diagnostic Labs Market Trend:

Automation and Digital Pathology & Imaging

Automation and digital pathology are reshaping lab economics in India by driving higher throughput, better accuracy, and faster turnaround times across core diagnostic workflows. In recent years, leading diagnostic chains have invested heavily in high-throughput automated analyzers to handle rising test volumes. For instance, in 2024, one of India’s largest diagnostic networks announced the commissioning of robotic sample processing systems capable of handling over 100,000 tests per day , significantly reducing manual handling errors and turnaround times.

Digital pathology adoption has also accelerated, particularly for oncology and specialized diagnostics. In 2025, large diagnostic players deployed AI-enabled digital slide scanning platforms to enable remote expert review and scalable reporting. These systems allow pathology slides to be digitized, stored, and shared across reference centers, improving diagnostic consensus and reducing reporting times from days to hours.

Government healthcare programs and hospital networks are further driving tech adoption. The Ministry of Health’s initiatives to integrate electronic medical records (EMRs) with lab data have encouraged laboratories to adopt LIS and cloud-based reporting platforms by 2023–2025, enabling real-time access to diagnostic reports and analytics.

Moreover, automation extends into sample collection and logistics. Home-collection models, launched by several major labs in 2024, leverage digital scheduling, barcoding, and real-time tracking to ensure sample integrity and faster processing. These innovations are particularly impactful in Tier II and Tier III cities, where conventional lab access was limited.

India Diagnostic Labs Market Opportunity:

Rising Government Incentives Offering Lucrative Opportunities

Corporate wellness programs and health-insurance partnerships are emerging as a structurally stable growth avenue for India’s diagnostic labs by converting discretionary testing into contract-backed volumes. According to the Ministry of Finance, India’s health and general insurers covered approximately 573 million lives in 2023–24 , creating a large insured population that routinely requires diagnostics for underwriting, renewals, and preventive assessments. This expanding insured base directly increases baseline demand for pathology panels and imaging tests.

Insurers are also embedding diagnostics into policy benefits to control long-term claims. As reported by national financial disclosures, annual health checkups and preventive screening are increasingly included in insurance plans, encouraging repeat diagnostic utilization rather than episodic testing. This shift strengthens demand visibility for empaneled labs while reducing payment risk through insurer-backed reimbursement mechanisms.

On the corporate side, employer-funded outpatient and wellness benefits are expanding rapidly. According to employer benefits disclosures reported by national business media, average OPD diagnostic coverage increased from approximately USD120 per employee per year to nearly USD 180 per employee , reflecting rising employer spend on preventive healthcare. At scale, large enterprises covering tens of thousands of employees translate this into multi-million-USD annual diagnostic contracts.

India Diagnostic Labs Market Challenge:

Skilled Workforce and Radiologist Availability Constraints

Despite market expansion, skilled manpower scarcity remains a structural bottleneck for India’s diagnostic ecosystem. As per the National Medical Commission, India has fewer than one radiologist per 100,000 individuals , far below the demand generated by rising CT, MRI, and PET-CT installations. For instance, multiple state health departments flagged imaging report backlogs of 24–72 hours in district hospitals during 2023–2024 audits, directly impacting turnaround times in PPP-operated diagnostic centers and limiting scalability in metro-adjacent and tier-II cities.

Pathology services face parallel constraints due to uneven workforce distribution. According to the Association of Clinical Biochemists of India, certified pathologists and senior lab technologists remain heavily concentrated in metropolitan clusters. For instance, organized diagnostic chains expanded centralized reference labs in Maharashtra and Tamil Nadu during 2024 to offset shortages in eastern and northeastern states, increasing logistics dependency. While automation improves throughput, statutory mandates still require qualified sign-offs, elevating compliance costs and constraining decentralized expansion.

Additionally, price sensitivity under government reimbursement frameworks restricts margin flexibility. According to state health authority tender documents from Gujarat, Rajasthan, and Uttar Pradesh, reimbursement rates for routine pathology panels and radiology scans have seen minimal upward revision since 2022. For instance, capped CT and MRI tariffs under public health schemes have discouraged fresh imaging investments by smaller labs, slowing consolidation and limiting service penetration in semi-urban and rural markets.

India Diagnostic Labs Market (2026-32) Segmentation Analysis:

The India Diagnostic Labs Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the India level. Based on the analysis, the market has been further classified as;

Based on Test Type:

- Pathology

- Radiology & Imaging

Pathology holds the largest share of about 72% in India because it is high-frequency, preventive in nature, and deeply embedded across routine clinical care and public health programs. Conditions such as diabetes, hypertension, anemia, kidney disease, and lipid disorders require regular blood, urine, and biochemical testing multiple times each year, inherently favoring pathology over imaging.

This dominance is further reinforced by government healthcare programs. Under the National Health Mission, population-based screening initiatives for diabetes, hypertension, anemia, and selected cancers rely primarily on laboratory pathology tests to identify and track at-risk individuals. The Indian Council of Medical Research identifies anemia and diabetes as among the most prevalent health conditions in the country, both of which are diagnosed and monitored almost entirely through pathology markers such as hemoglobin, fasting glucose, and HbA1c.

Together, high test frequency, policy alignment, and preventive healthcare priorities position pathology as the dominant diagnostic modality in India compared with radiology.

Based on End-User:

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers (IDCs)

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

Independent Diagnostic Centers (IDCs) lead the end-use landscape in the India Diagnostic Labs Market, accounting for about 42% because of scale, accessibility, and specialized services tailored to routine and preventive care. India has over 300,000 diagnostic laboratories spread across the country, making diagnostics among the most accessible healthcare services outside traditional hospital settings. This extensive base encompasses standalone centers, hub-and-spoke networks, and reference labs, reflecting deep market fragmentation where standalone and private labs form a large majority of facilities.

IDCs’ dominance stems from their ability to offer affordable, quick, and community-proximate services. Patients increasingly prefer diagnostic centers for routine tests and preventive checkups, with as high as 82% of individuals choosing diagnostic centers over hospitals for preventive health screenings due to speed and convenience .

India Diagnostic Labs Market (2026-32): Regional Projection

North India, anchored by Delhi NCR, dominates India’s Diagnostic Labs Market with a market share of about 33%, out of which Delhi NCR having 16%, because demand, capacity, and policy mechanisms reinforce each other in a single, tightly connected ecosystem. The region serves a huge population base, while also acting as a referral hub for patients from Uttar Pradesh, Haryana, Rajasthan, and Uttarakhand, concentrating testing volumes far beyond local demand. This sustained inflow explains why government empanelment records list 571 healthcare organizations across Delhi NCR , reflecting dense diagnostic and hospital infrastructure supporting high daily sample throughput.

That demand is matched by accredited capacity. Delhi alone hosts around 174 NABL-accredited laboratories, one of the highest concentrations in the country, enabling advanced pathology, molecular diagnostics, and specialized testing to be performed locally rather than outsourced. As a result, national diagnostic chains preferentially locate reference labs and high-end testing facilities in the region, further reinforcing scale advantages.

Gain a Competitive Edge with Our India Diagnostic Labs Market Report:

- India Diagnostic Labs Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- India Diagnostic Labs Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- India Diagnostic Labs Market Policies, Regulations, and Product Standards

- India Diagnostic Labs Market Trends & Developments

- India Diagnostic Labs Market Dynamics

- Growth Factors

- Challenges

- India Diagnostic Labs Market Hotspot & Opportunities

- India Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Pathology

- Radiology & Imaging

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- Clinical Chemistry

- Hematology

- Immunology & Serology

- Microbiology

- Histopathology & Cytopathology

- Molecular Diagnostics

- Genetic Testing

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- X-Ray

- Ultrasound

- CT Scan

- MRI

- Mammography

- PET-CT

- Nuclear Imaging

- Others

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- Walk-in Testing

- Home Sample Collection

- Mobile Diagnostic Units

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- Infectious Diseases

- Oncology

- Diabetes & Endocrinology

- Cardiology

- Neurology

- Nephrology

- Gastroenterology

- Gynecology & Obstetrics

- Respiratory Disorders

- Orthopedics

- Others

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

- By Region- Market Size & Forecast 2022-2032, USD Million

- North

- National Capital Region (Delhi NCR)

- Uttar Pradesh

- Punjab

- Rajasthan

- South

- Karnataka

- Tamil Nadu

- Telangana

- Kerala

- East

- West Bengal

- Odisha

- West

- Maharashtra

- Gujarat

- Madhya Pradesh

- North

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Pathology Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Radiology & Imaging Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Diagnostic Labs Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Dr. Lal PathLabs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thyrocare Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Metropolis Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SRL Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Apollo Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vijaya Diagnostic Centre

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pathkind Labs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Healthians

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aarthi Scans & Labs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Oncquest Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Suburban Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Max Lab

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Redcliffe Labs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lifeline Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lucid Medical Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dr. Lal PathLabs

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now