India Built-in Kitchen Appliances Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Product (Hoods, Refrigerators, Ovens & Microwaves, Hobs, Dishwashers, Others), By Application (Residential, Commercial), By Price Range (Mass, Premium), By Sales Channel (Retail ... Online, Retail Offline), and others Read more

- FMCG

- Mar 2026

- Pages 135

- Report Format: PDF, Excel, PPT

India Built-in Kitchen Appliances Market

Projected 10.01% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 492 Million

Market Size (2032)

USD 872 Million

Base Year

2025

Projected CAGR

10.01%

Leading Segments

By Product: Hobs

India Built-in Kitchen Appliances Market Report Key Takeaways:

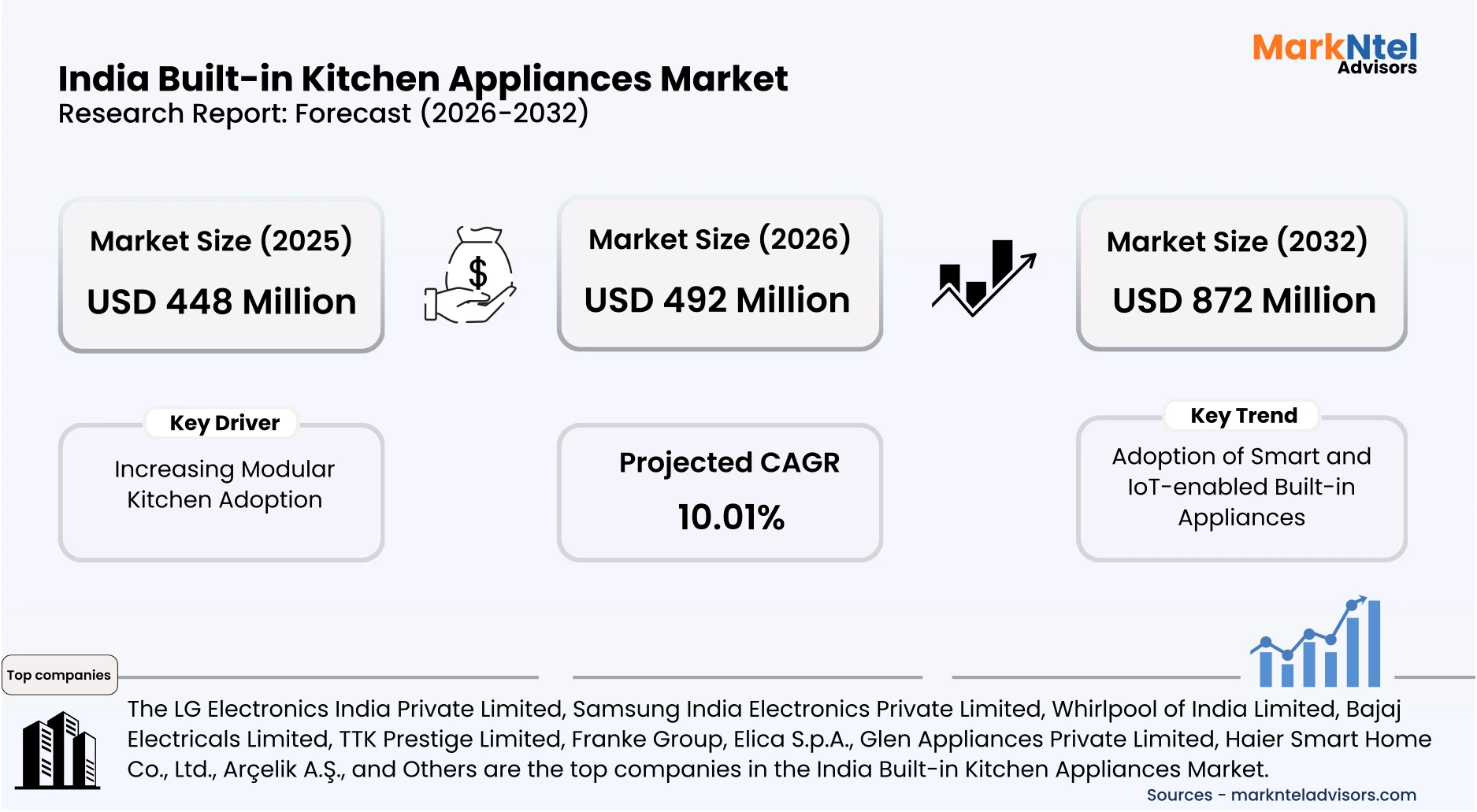

- The India Built-in Kitchen Appliances market size was valued at USD 448 million in 2025 and is projected to grow from USD 492 million in 2026 to USD 872 million by 2032, exhibiting a CAGR of 10.01% during 2026-32.

- By product, the hobs represented a significant share of about 30% in the India Built-in Kitchen Appliances Market in 2026.

- By application, the residential sector seized a significant share of about 87% in the India Built-in Kitchen Appliances Market in 2026.

- Leading Built-in kitchen appliances companies in India are LG Electronics India Private Limited, Samsung India Electronics Private Limited, Whirlpool of India Limited, Bajaj Electricals Limited, TTK Prestige Limited, Franke Group, Elica S.p.A., Glen Appliances Private Limited, Haier Smart Home Co., Ltd., Arçelik A.Ş., and Others.

Market Insights & Analysis: India Built-in Kitchen Appliances Market (2026-32):

The India Built-in Kitchen Appliances Market size was valued at around USD 448 million in 2025 and is projected to grow from USD 492 million in 2026 to USD 872 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 10.01% during the forecast period, i.e., 2026-32.

The India Built-in Kitchen Appliances Market is projected to expand steadily, driven by increasing modular kitchen adoption and the rising integration of smart and IoT-enabled appliances, reflecting evolving consumer preferences toward convenience, automation, and modern kitchen infrastructure.

Government-backed housing initiatives continue to play a pivotal role in shaping demand. Under the Pradhan Mantri Awas Yojana–Urban (PMAY-U), nearly 9.665 million houses had been completed by 2025 out of 12.2 million sanctioned units, highlighting the significant scale of urban housing development across the country. This growing housing base is directly fostering the integration of modular kitchens, where built-in appliances are increasingly becoming standard features. Further strengthening this trajectory, PMAY-Urban 2.0 approved an additional 147,000 houses across 14 states in 2025, indicating continued expansion of organized urban housing .

State-level developments reinforce this momentum. For instance, Odisha has completed over 136,000 urban houses, reflecting rising adoption of customized interiors, including modular kitchens.

Similarly, West Bengal has allocated over 4.56 million houses, with 3.41 million completed by mid-2025, demonstrating substantial residential growth in eastern India . Meanwhile, in western India, Maharashtra’s Beed district alone delivered more than 50,000 houses within months, supported by government funding exceeding USD 120 million, underscoring rapid execution at the regional level.

Leading states such as Andhra Pradesh and Gujarat have emerged as key contributors to PMAY-Urban, collectively driving nationwide housing completions toward nearly 9.6 million units by 2026. This widespread expansion across regions is significantly increasing the adoption of modular kitchens and, consequently, built-in appliances.

In parallel, the growing penetration of smart and IoT-enabled technologies is transforming kitchen environments. Increasing internet access, rising smart home adoption, and evolving consumer preferences for automation and energy efficiency are accelerating demand for connected built-in appliances. These innovations enhance convenience and support premiumization, particularly in urban households.

Looking ahead, the outlook remains highly favorable. The Government of India has approved the construction of an additional 20 million rural houses under PMAY-G for 2024–2029, ensuring sustained housing expansion across states. Moreover, state-specific initiatives such as Uttar Pradesh’s target of over 6 million houses in 2025–26 will further amplify demand for modern kitchen infrastructure.

The convergence of large-scale housing development and increasing adoption of smart, modular kitchens is expected to significantly drive demand for built-in appliances. This structural growth in residential infrastructure will remain a key catalyst for long-term market expansion in India.

India Built-in Kitchen Appliances Market Recent Developments:

- 2025: Hindware Smart Appliances has expanded its kitchen portfolio with a new range of smart chimneys, built-in ovens, and hobs designed for modern modular kitchens. The launch includes 12 BLDC motor-based chimneys with motion sensor controls and over 20 advanced hobs, alongside multifunction ovens offering up to 16 cooking modes. These products emphasize energy efficiency, automation, and enhanced cooking performance.

- 2025: Liebherr Appliances India has commenced production of fully integrated refrigerators, freezers, and combination units in India, marking its first manufacturing base outside Europe. The move strengthens its presence in the country’s premium appliance segment, with locally produced, climate-adapted products ensuring faster availability and catering to rising demand for high-performance built-in kitchen solutions.

India Built-in Kitchen Appliances Market Scope:

| Category | Segments |

|---|---|

| By Product | (Hoods, Refrigerators, Ovens & Microwaves, Hobs, Dishwashers, Others), |

| By Application | (Residential, Commercial), |

| By Price Range | (Mass, Premium), |

| By Sales Channel | (Retail Online, Retail Offline), |

India Built-in Kitchen Appliances Market Driver:

Increasing Modular Kitchen Adoption

The expansion of modular kitchens in India is being significantly driven by state-level housing development programs, supported by large-scale government initiatives. Under PMAY-Gramin (2024–25), state-wise allocations across major regions, including Uttar Pradesh, Bihar, Madhya Pradesh, Maharashtra, Rajasthan, Tamil Nadu, Karnataka, and Assam, collectively account for over 8.43 million houses in a single year. This substantial pipeline of residential construction is creating widespread demand for modern housing infrastructure, where modular kitchens are increasingly being integrated as a standard feature.

These states represent some of the largest contributors to India’s housing growth, spanning both high-population and emerging regions. As new homes are constructed under organized government schemes, there is a gradual shift toward improved living standards, including better-designed kitchen spaces. This transition is encouraging the adoption of built-in appliances that align with modular kitchen layouts, particularly in urbanizing and semi-urban areas.

At the regional level, implementation progress further reinforces this trend. For instance, Jammu & Kashmir has achieved approximately 323,000 completed houses with around 97% target fulfillment by 2026, demonstrating rapid housing expansion even in developing regions. Such high completion rates highlight the effectiveness of state-led execution and the growing penetration of modern housing designs.

State-driven housing expansion is structurally increasing the adoption of modular kitchens across India. This widespread residential growth will significantly accelerate demand for built-in kitchen appliances, supporting sustained market expansion.

India Built-in Kitchen Appliances Market Trend:

Adoption of Smart and IoT-enabled Built-in Appliances

The integration of smart and IoT-enabled technologies into built-in kitchen appliances is emerging as a prominent trend in India, driven by rapid digital infrastructure expansion and evolving consumer preferences.

According to the Press Information Bureau, India’s internet subscriber base reached approximately 954 million by March 2024, creating a strong foundation for connected home ecosystems and enabling seamless operation of smart appliances.

This growing digital penetration is translating into increased adoption of IoT-enabled devices across households. News reports indicate that usage of connected devices rose by nearly 30% in 2025, supported by a young, tech-savvy population and rising demand for automation, convenience, and energy efficiency in everyday living . As consumers become more comfortable with smart technologies, the demand for integrated kitchen solutions with remote control and intelligent features is accelerating.

Industry developments further validate this shift. For instance, Häfele India introduced its Midora Full Steam Oven and smart hobs, featuring touch-based controls and multifunctional capabilities. Such product innovations highlight the transition toward digitally controlled, built-in appliances designed to enhance user experience and optimize cooking processes within modular kitchens .

The rapid growth in digital connectivity and IoT adoption is reshaping kitchen environments in India. This trend will significantly accelerate the demand for smart built-in appliances, driving innovation and long-term market expansion.

India Built-in Kitchen Appliances Market Opportunity:

Growth in Real Estate and Premium Housing Projects

India’s robust real estate expansion is creating a significant structural opportunity for the built-in kitchen appliances market, particularly within urban and premium housing segments. Government-supported housing initiatives continue to drive large-scale residential development, with over 11.6 million homes sanctioned and approximately 9.27 million completed by May 2025, underscoring the sustained addition of new housing stock across the country. This growth is directly supporting the integration of modular kitchens, where built-in appliances are increasingly incorporated as standard features in modern homes.

Regulatory advancements have improved transparency in India’s real estate sector. With over 138,000 projects registered under RERA by January 2025, a strong and organized housing pipeline has emerged, encouraging developers to integrate advanced, space-efficient modular kitchens and built-in appliances to enhance project value.

Additionally, the market is witnessing a clear shift toward premium housing. Recent insights suggest residential property prices are expected to increase at a ~5% annual rate through 2028, driven by rising disposable incomes and evolving consumer preferences for high-quality living spaces. Premium developments typically emphasize fully integrated modular kitchens, thereby accelerating demand for built-in appliances.

The convergence of large-scale housing development and premiumization trends is embedding built-in appliances into modern residential design. This will substantially enhance market penetration and position real estate growth as a critical long-term opportunity.

India Built-in Kitchen Appliances Market Challenge:

High Initial Cost and Affordability Constraints

Affordability constraints remain a significant barrier to the widespread adoption of built-in kitchen appliances in India. The high upfront cost of these appliances, driven by customization, installation, and integration within modular kitchens, limits their accessibility, particularly among middle-income households. This challenge is further intensified by broader housing affordability pressures across urban markets.

In major Indian cities, the price-to-income ratio is approximately 7.5, considerably above the globally accepted benchmark of 5, indicating that residential properties are relatively expensive compared to household earnings.

Additionally, EMI-to-income levels have reached around 61%, exceeding the recommended threshold of 50%, thereby reducing disposable income available for non-essential upgrades such as premium kitchen solutions.

As a result, homebuyers often prioritize core housing expenses over additional investments like built-in appliances. This trend is especially evident in mid-income housing segments, where budget constraints limit the adoption of integrated kitchen systems despite growing awareness and aspiration.

Overall, elevated housing costs and financial burden significantly restrict consumer spending capacity. This affordability gap will continue to hinder large-scale adoption of built-in kitchen appliances, limiting market expansion beyond premium segments.

India Built-in Kitchen Appliances Market (2026-32) Segmentation Analysis:

The India Built-in Kitchen Appliances Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Product:

- Hoods

- Refrigerators

- Ovens & Microwaves

- Hobs

- Dishwashers

- Others

The hobs segment dominates the India Built-in Kitchen Appliances market, with 30% market share. Market dominance is due to its indispensable role in everyday cooking and strong alignment with domestic culinary requirements. As a core cooking appliance, hobs witness consistent demand across residential categories, making them a foundational component of modular kitchen setups.

The transition from traditional freestanding stoves to built-in hobs has accelerated with the growing adoption of modular kitchens. Built-in hobs offer seamless integration, optimized space utilization, and superior aesthetics, which are increasingly valued in modern urban housing. Furthermore, their availability across a broad pricing spectrum enables penetration beyond premium segments into mid-income households.

Product innovation is also contributing to segment growth. Advanced features such as auto-ignition systems, flame safety mechanisms, multi-burner configurations, and durable glass finishes enhance both functionality and safety, catering to the diverse cooking practices prevalent in India.

Additionally, expanding piped natural gas (PNG) infrastructure in urban regions is facilitating greater adoption of built-in hobs over conventional alternatives. Compared to other built-in appliances, hobs involve relatively lower initial investment and higher usage frequency, resulting in quicker replacement cycles and sustained demand.

The combination of essential utility, affordability, and compatibility with evolving kitchen designs firmly establishes hobs as the dominant segment, supporting sustained growth in the India built-in kitchen appliances market.

Based on Application:

- Residential

- Commercial

The residential segment dominates the India Built-in Kitchen Appliances Market, with 87% market share, supported by sustained growth in housing construction and evolving consumer preferences toward modern living environments.

Rapid urbanization and increasing household incomes are driving the adoption of modular kitchens, where built-in appliances are becoming integral components of contemporary home design.

Government-led housing initiatives and the continuous addition of residential units across urban and semi-urban regions are further reinforcing this dominance. Newly constructed homes increasingly incorporate modular kitchen layouts, encouraging the installation of integrated appliances such as hobs, ovens, and dishwashers.

Lifestyle transformation also plays a crucial role. The growing prevalence of nuclear families and dual-income households has increased the need for efficient, space-saving, and technologically advanced kitchen solutions. Built-in appliances address these requirements by offering enhanced functionality, convenience, and aesthetic appeal.

In comparison, the commercial segment remains relatively niche, with demand concentrated in hospitality and institutional applications. The residential sector, by contrast, benefits from a significantly broader consumer base and consistent replacement demand.

Overall, the convergence of housing expansion, lifestyle evolution, and modular kitchen adoption positions the residential segment as the primary contributor to the built-in kitchen appliances market growth in India.

Gain a Competitive Edge with Our India Built-in Kitchen Appliances Market Report:

- India Built-in Kitchen Appliances Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- India Built-in Kitchen Appliances Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Built-in Kitchen Appliances Market Policies, Regulations, and Standards

- India Built-in Kitchen Appliances Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Built-in Kitchen Appliances Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Hoods- Market Insights and Forecast 2022-2032, USD Million

- Refrigerators- Market Insights and Forecast 2022-2032, USD Million

- Ovens & Microwaves- Market Insights and Forecast 2022-2032, USD Million

- Hobs- Market Insights and Forecast 2022-2032, USD Million

- Dishwashers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- By Price Range

- Mass- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Direct Sale- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Stores- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- India Hoods Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Refrigerators Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Ovens & Microwaves Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Hobs Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Dishwashers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- LG Electronics India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samsung India Electronics Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Whirlpool of India Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bajaj Electricals Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TTK Prestige Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Franke Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elica S.p.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Glen Appliances Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haier Smart Home Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arçelik A.Ş.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Electronics India Private Limited

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now