GCC Non-Alcoholic Wine Market Research Report: Growth Drivers & Forecast (2026-2032)

By Product Type (Sparkling Wine, Still Wine), By Packaging (Bottles, Cans), By Distribution Channel (Off-Trade, On-Trade), and others ... Read more

- Food & Beverages

- Mar 2026

- Pages 175

- Report Format: PDF, Excel, PPT

GCC Non-Alcoholic Wine Market

Projected 7.47% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 185 Million

Market Size (2032)

USD 285 Million

Base Year

2025

Projected CAGR

7.47%

Leading Segments

By Product Type: Sparkling Wine

GCC Non-Alcoholic Wine Market Report Key Takeaways:

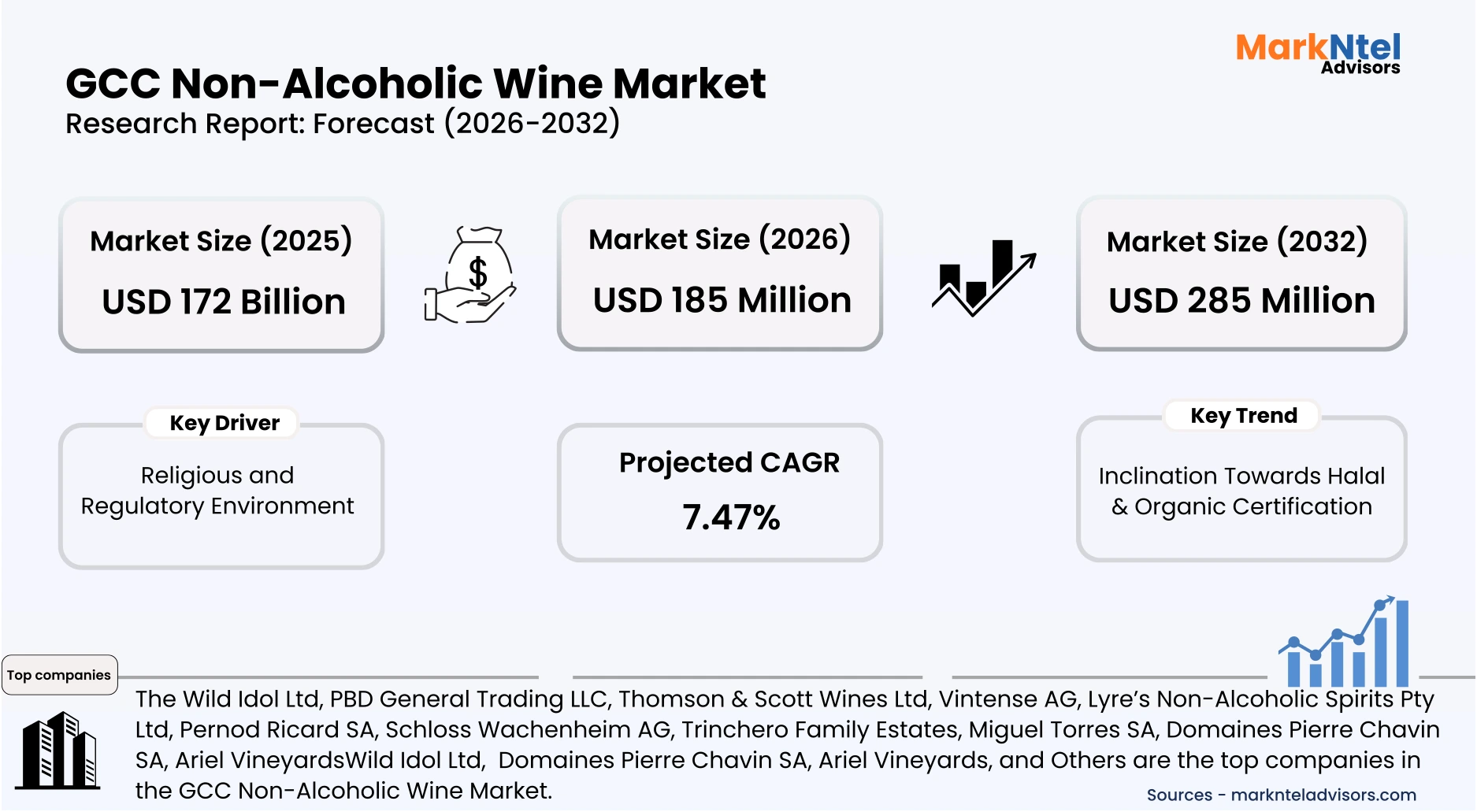

- The GCC Non-Alcoholic Wine Market size was valued at USD 172 million in 2025 and is projected to grow from USD 185 million in 2026 to USD 285 million by 2032, exhibiting a CAGR of 7.47% during the forecast period.

- The UAE holds the largest market share of about 40% in the GCC Non-Alcoholic Wine Market in 2026.

- By product type, the sparkling wine segment represented a significant share of about 38% in the GCC Non-Alcoholic Wine Market in 2026.

- By alcohol by volume (ABV) (%), the ABV (0.0%) segment presented a significant share of about 50% in the GCC Non-Alcoholic Wine Market in 2026.

- Leading non-alcoholic wine companies in the GCC market are Wild Idol Ltd, PBD General Trading LLC, Thomson & Scott Wines Ltd, Vintense AG, Lyre’s Non-Alcoholic Spirits Pty Ltd, Pernod Ricard SA, Schloss Wachenheim AG, Trinchero Family Estates, Miguel Torres SA, Domaines Pierre Chavin SA, Ariel Vineyards, and Others.

Market Insights & Analysis: GCC Non-Alcoholic Wine Market (2026-32):

The GCC Non-Alcoholic Wine Market size was valued at around USD 172 million in 2025 and is projected to grow from USD 185 million in 2026 to USD 285 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 7.47% during the forecast period, i.e., 2026-32.

The GCC Non-Alcoholic Wine Market is projected to expand steadily, driven by strong religious compliance norms and evolving regulatory frameworks, alongside rising adoption of halal and organic certifications that enhance consumer trust and expand product acceptance across the region. Across Gulf countries, alcohol consumption is subject to strict legal oversight, creating a controlled environment in which non-alcoholic wine serves as a culturally compatible alternative.

In the United Arab Emirates, alcohol sales and consumption are regulated at both federal and emirate levels, with retail and service permitted only in licensed venues such as hotels, clubs, and designated outlets under strict age-verification requirements. Dubai’s reinstatement of a 30% municipality tax on alcohol in 2025, after a temporary suspension in 2023, underscores the government’s careful balancing of economic objectives with social norms. This structured oversight sustains a hospitality landscape where non-alcoholic wine provides an acceptable substitute for consumers seeking wine-style beverages within legal and cultural boundaries.

Qatar maintains even tighter controls. Public drinking is prohibited and punishable by imprisonment of up to six months and fines reaching approximately USD 825. Alcohol purchases are restricted to non-Muslim residents holding permits issued through the state-controlled Qatar Distribution Company (QDC), and sales occur only in licensed venues . Such legal stringency enhances the relevance of non-alcoholic wine, which avoids compliance risks while aligning with Islamic values.

Fiscal measures are further shaping beverage demand. For instance, from the beginning of January 2026, both Saudi Arabia and the UAE transitioned from a flat 50% excise tax on sweetened beverages to a tiered system based on sugar concentration per 100 ml. By linking taxation directly to sugar content, authorities are incentivizing reformulation and reduced-sugar product development. Low-sugar non-alcoholic wine variants may therefore benefit from a more favorable tax positioning relative to higher-sugar beverage categories.

Certification trends also strengthen consumer confidence. For example, halal-certified 0.0% wine-style products, including organic variants such as Lussory’s Merlot, Rosé, and Chardonnay, illustrate how formal halal authentication can broaden market acceptance among observant Muslim consumers and institutional buyers.

Looking ahead, major aviation and infrastructure projects, including Dubai’s Al Maktoum International Airport and Saudi Arabia’s King Salman International Airport, are designed to significantly expand passenger handling capacity before 2030 . These developments will stimulate hospitality growth, luxury retail expansion, and diversified beverage portfolios catering to global travelers.

The interplay of strict alcohol governance, sugar-based taxation reforms, halal certification adoption, and large-scale tourism infrastructure investment establishes a structurally supportive environment for non-alcoholic wine. Collectively, these factors are expected to reinforce steady, policy-aligned market expansion across the GCC in the coming years.

GCC Non-Alcoholic Wine Market Recent Developments:

- 2025: Pernod Ricard has introduced a premium non-alcoholic portfolio in the Middle East, targeting the UAE, Saudi Arabia, and Kuwait. The range includes botanical and 0.0% offerings like Ceder’s and Jacob’s Creek Sparkling 0.0, aimed at expanding refined alcohol-free alternatives in regional social occasions.

- 2025: Premium non-alcoholic wine brand Noughty has introduced 200 ml single-serve “Noughty Minis” of its Sparkling Chardonnay (0.0 % ABV), offering the same award-winning flavor in a portable format. The mini bottles enhance accessibility for events, travel, and retail, expanding options in the non-alcoholic wine category .

GCC Non-Alcoholic Wine Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Sparkling Wine, Still Wine), |

| By Packaging | (Bottles, Cans), |

| By Distribution Channel | (Off-Trade, On-Trade), |

GCC Non-Alcoholic Wine Market Driver:

Religious and Regulatory Environment

Alcohol prohibition under Islamic law remains a core structural driver of the GCC non-alcoholic wine market. Under Sharia, intoxicants are classified as haram, leading to strict regulatory controls across Gulf countries. In Saudi Arabia, alcohol has been banned since the early 1950s, reinforcing strong cultural and legal preferences for alcohol-free beverages and positioning non-alcoholic wine as a compliant and socially acceptable alternative.

Recent regulatory developments under Saudi Arabia’s Vision 2030 reform agenda illustrate a calibrated policy shift designed to support tourism diversification without undermining cultural norms. By 2026, alcohol sales are expected to be permitted at approximately 600 licensed tourist establishments, including select five-star hotels, luxury resorts, and flagship giga-projects such as NEOM, Sindalah Island, and the Red Sea Project.

The reform remains tightly controlled, excluding public consumption, retail sales, and spirits, thereby maintaining regulatory oversight and safeguarding domestic sensitivities. These measures are strategically aligned with upcoming global events, including Expo 2030 and the 2034 FIFA World Cup, which aim to elevate the Kingdom’s global tourism footprint.

This dual regulatory environment, with strict prohibition for the broader population alongside limited hospitality liberalization, reinforces demand for premium non-alcoholic wine offerings that can cater to mixed consumer segments within compliant settings.

Enduring religious norms combined with structured tourism reforms create a distinctive demand ecosystem for non-alcoholic wine in the GCC. This balance between cultural preservation and economic diversification is expected to support sustained category expansion in the years ahead.

GCC Non-Alcoholic Wine Market Trend:

Inclination Towards Halal & Organic Certification

Halal certification has become a strategic growth lever within the GCC non-alcoholic wine market, reflecting both regulatory enforcement and heightened consumer scrutiny regarding product compliance.

Across Gulf economies, halal accreditation is not merely a marketing attribute but a formal requirement in many food and beverage categories, reinforcing traceability, ingredient transparency, and Sharia adherence.

According to the i-CAS Halal Certification, more than 1,600 halal certificates have been issued globally, with 331 certifications recorded in the UAE and 126 in Saudi Arabia. This volume underscores the institutionalization of halal governance across diverse product segments, including beverages.

Within the non-alcoholic wine category, producers are increasingly integrating halal certification to strengthen credibility and facilitate market entry. For example, products such as Pierre Chavin Perle Rosé (0.0% ABV) are explicitly marketed as halal-certified, with clear labeling confirming zero alcohol content. Although manufactured in France, the product complies with recognized Islamic dietary standards and is distributed through retail channels serving GCC consumers, illustrating how international suppliers adapt to regional regulatory expectations.

This certification-driven positioning enhances acceptance among observant Muslim consumers while also supporting procurement decisions in hotels, airlines, and institutional catering environments where halal compliance is mandatory. As governments continue tightening food safety and halal verification protocols, certified non-alcoholic wine offerings are expected to gain a competitive advantage, reinforcing long-term market expansion across the GCC.

GCC Non-Alcoholic Wine Market Opportunity:

Expansion of Tourism and Mega Events

Tourism acceleration and mega-event programming across the GCC are creating measurable expansion avenues for the non-alcoholic wine market, particularly within premium hospitality and event-driven consumption channels.

Under the GCC Tourism Strategy 2023–2030, the region welcomed 68.1 million international tourists in 2023, generating approximately USD 110.4 billion in tourism receipts. This performance signals structural recovery and long-term policy commitment to tourism as a diversification pillar beyond hydrocarbons.

Saudi Arabia represents a central growth engine within this regional landscape. The Kingdom recorded 116 million visitors in 2024 and an estimated 122 million in 2025, contributing nearly USD 81 billion in tourism spending. Guided by Vision 2030, Saudi Arabia aims to attract 150 million annual visitors by 2030, prompting significant expansion in hotel infrastructure, entertainment districts, and destination projects .

As visitor demographics diversify, hotels, resorts, airlines, and event operators increasingly require inclusive beverage portfolios that cater to varying religious and cultural preferences. Premium non-alcoholic wine aligns with this demand by delivering a wine-style sensory experience without regulatory or religious restrictions.

Sustained tourism growth, giga-project development, and event-led hospitality expansion are expected to structurally elevate demand for sophisticated alcohol-free beverage options. Consequently, non-alcoholic wine is well-positioned to gain stronger institutional adoption and premium placement across GCC markets through 2030.

GCC Non-Alcoholic Wine Market Challenge:

Taste Perception Gaps Impeding Market Growth

A major challenge for the GCC non-alcoholic wine market is the taste perception gap between consumer expectations and the sensory experience of dealcoholized wine. Scientific research shows that removing alcohol significantly alters key aroma and flavor compounds, reducing fruity, floral, and complex sensory notes that define traditional wine.

Alcohol’s role as a flavor carrier and contributor to mouthfeel is significant; removing it often results in less body, imbalanced acidity, and muted aroma, which many consumers perceive as inferior to alcoholic counterparts.

Recent studies highlight that loss of volatile compounds during alcohol removal can diminish overall sensory quality, particularly fruity and floral characteristics essential to wine enjoyment, making non-alcoholic wine appear less satisfying to palate expectations.

Comparative sensory analyses indicate that even advanced dealcoholization methods struggle to fully replicate the complexity and persistence of aromas and flavor profiles found in traditional wines, reinforcing taste dissatisfaction among consumers familiar with conventional wine.

This sensory gap is compounded by consumer comparison bias, where non-alcoholic wines are directly judged against alcoholic versions rather than appreciated on their own merits, slowing acceptance and repeat purchases.

Unless producers can narrow the sensory divide through technological innovation and tailored flavor engineering, perception challenges will continue to limit broader adoption and mainstream growth of non-alcoholic wine in the GCC market.

GCC Non-Alcoholic Wine Market (2026-32) Segmentation Analysis:

The GCC Non-Alcoholic Wine Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Sparkling Wine

- Red

- White

- Rosé

- Still Wine

- Brut

- Blanc

- Rosé

- Prosecco-style

The sparkling wine segment dominates the GCC Non-Alcoholic Wine Market, accounting for approximately 38% of the total market size, driven by its strong alignment with celebration culture, premium hospitality formats, and experiential dining trends.

In a region where alcohol consumption is restricted or culturally sensitive, sparkling non-alcoholic wine offers a sophisticated alternative that preserves the ceremonial and visual attributes associated with traditional sparkling beverages.

Within the hospitality sector, upscale hotels, fine-dining restaurants, airlines, and large-scale event venues prioritize sparkling variants to enhance guest experience while maintaining regulatory compliance.

White and rosé sparkling formats are especially prominent due to their lighter flavor profiles and versatility in pairing with Middle Eastern and international cuisines. In addition, sparkling products typically command stronger gifting demand, supported by premium packaging and festive positioning during Eid and other cultural occasions.

From a consumer acceptance standpoint, sparkling non-alcoholic wine faces fewer direct comparisons with traditional alcoholic red wines, reducing taste expectation disparities and encouraging trial among new users. Its lighter mouthfeel and refreshing character also align with growing interest in moderation and wellness-oriented consumption. Collectively, premium positioning, hospitality-driven demand, and cultural suitability reinforce sparkling wine’s leadership within the GCC non-alcoholic wine market.

Based on Alcohol by Volume (ABV) (%):

- ABV (0.0%)

- ABV (Up to 0.5%)

- ABV (Up to 1.2%)

The ABV (0.0%) segment dominates the GCC Non-Alcoholic Wine Market, accounting for about 50% of the total market volume, primarily due to its clear alignment with religious, regulatory, and institutional requirements.

In Gulf countries where Islamic principles shape consumption norms, beverages containing any measurable alcohol content may face scrutiny among observant consumers. Products labeled 0.0% ABV provide unequivocal assurance of complete alcohol absence, strengthening trust and broadening acceptance across conservative households and family-oriented consumption settings.

From a regulatory perspective, 0.0% formulations offer greater clarity in labeling, import approvals, and distribution. Hospitality operators, airlines, and large-scale event venues often prioritize absolute alcohol-free beverages to avoid compliance ambiguity when serving mixed guest demographics.

Halal certification processes are also more straightforward for 0.0% ABV products, as the absence of residual alcohol eliminates interpretational concerns regarding permissible thresholds. This facilitates procurement by government institutions, supermarkets, and premium hotels that require documented compliance.

Furthermore, rising health awareness and moderation trends across urban GCC populations reinforce demand for beverages that explicitly guarantee zero alcohol content. The 0.0% designation resonates strongly with wellness-oriented consumers seeking premium yet responsible alternatives.

Collectively, religious sensitivity, regulatory certainty, certification advantages, and evolving lifestyle preferences solidify the leadership of the 0.0% ABV segment within the GCC non-alcoholic wine market.

GCC Non-Alcoholic Wine Market (2026-32): Regional Projection

The UAE dominates the GCC Non-Alcoholic Wine Market with an estimated 40% share, supported by its mature hospitality ecosystem, diversified population base, and advanced retail infrastructure.

As a regional commercial and tourism hub, the UAE attracts substantial international visitor flows and maintains a large expatriate community, generating sustained demand for premium, culturally adaptable beverage options.

Dubai and Abu Dhabi anchor the country’s dominance, with dense concentrations of luxury hotels, upscale dining establishments, event venues, and international airlines. These institutions increasingly integrate non-alcoholic wine into beverage programs to accommodate mixed consumer demographics, including Muslim residents, wellness-oriented consumers, and global travelers seeking alcohol-free alternatives. The structured regulatory framework governing alcohol service further encourages operators to maintain inclusive beverage portfolios that align with compliance standards and social norms.

The UAE’s sophisticated retail landscape, including hypermarkets, gourmet specialty stores, duty-free outlets, and robust e-commerce platforms, facilitates wide product availability and strong brand penetration. Additionally, the country’s strategic position as a regional logistics and re-export center enables efficient importation and redistribution of international non-alcoholic wine brands across neighboring GCC markets.

High disposable income levels, a strong premium gifting culture, and consumer openness to global lifestyle trends further reinforce market depth. Collectively, institutional demand, regulatory clarity, infrastructure maturity, and purchasing power consolidate the UAE’s leadership within the GCC non-alcoholic wine segment.

Gain a Competitive Edge with Our GCC Non-Alcoholic Wine Market Report:

- GCC Non-Alcoholic Wine Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- GCC Non-Alcoholic Wine Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Non-Alcoholic Wine Market Policies, Regulations, and Product Standards

- GCC Non-Alcoholic Wine Market Trends & Developments

- GCC Non-Alcoholic Wine Market Dynamics

- Growth Factors

- Challenges

- GCC Non-Alcoholic Wine Market Hotspot & Opportunities

- GCC Non-Alcoholic Wine Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Liters)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million & Million Liters

- Sparkling Wine

- Red

- White

- Rosé

- Still Wine

- Brut

- Blanc

- Rosé

- Prosecco-style

- Sparkling Wine

- By Alcohol by Volume (ABV) (%) - Market Size & Forecast 2022-2032, USD Million & Million Liters

- ABV (0.0%)

- ABV (Up to 0.5%)

- ABV (Up to 1.2%)

- By Packaging- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Bottles

- Cans

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million & Million Liters

- Off-Trade

- Supermarkets & Hypermarkets

- Specialty Stores

- E-commerce

- Convenience Stores

- On-Trade

- Restaurants

- Hotels

- Bars & Pubs

- Off-Trade

- By Country

- The UAE

- Saudi Arabia

- Qatar

- Kuwait

- Oman

- Bahrain

- Rest of GCC

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- The UAE Non-Alcoholic Wine Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Liters)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Alcohol by Volume (ABV) (%) - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Saudi Arabia Non-Alcoholic Wine Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Liters)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Alcohol by Volume (ABV) (%) - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Qatar Non-Alcoholic Wine Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Liters)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Alcohol by Volume (ABV) (%) - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Kuwait Non-Alcoholic Wine Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Liters)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Alcohol by Volume (ABV) (%) - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Oman Non-Alcoholic Wine Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Liters)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Alcohol by Volume (ABV) (%) - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Bahrain Non-Alcoholic Wine Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Liters)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Alcohol by Volume (ABV) (%) - Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- GCC Non-Alcoholic Wine Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Wild Idol Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PBD General Trading LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thomson & Scott Wines Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vintense AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lyre’s Non-Alcoholic Spirits Pty Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pernod Ricard SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schloss Wachenheim AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Trinchero Family Estates

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Miguel Torres SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Domaines Pierre Chavin SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ariel Vineyards

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wild Idol Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now