GCC Jewelry Market Research Report: Growth Drivers & Forecast (2026-2032)

By Type (Rings, Necklaces, Chains, Bangles, Bracelets, Earrings, Pendants, Anklets, Brooches, Cufflinks, Charms, Coins, Bars, Others), By Material Type (Gold, Diamond, Gemstone, Pe ... arl, Platinum, Silver, Fashion / Costume), By Distribution Channel (Offline, Online), By Price Range (Ultra-Luxury (Above USD 50,000), Luxury (USD 10,000 – USD 50,000), Premium (USD 2,500 – USD 10,000), Mass Market (Below USD 500)), By End-Use (Bridal & Wedding, Festive & Cultural, Daily Wear, Gifting, Investment), and others Read more

- FMCG

- Feb 2026

- Pages 235

- Report Format: PDF, Excel, PPT

GCC Jewelry Market

Projected 5.34% CAGR from 2026 to 2032

Study Period

2026-2032

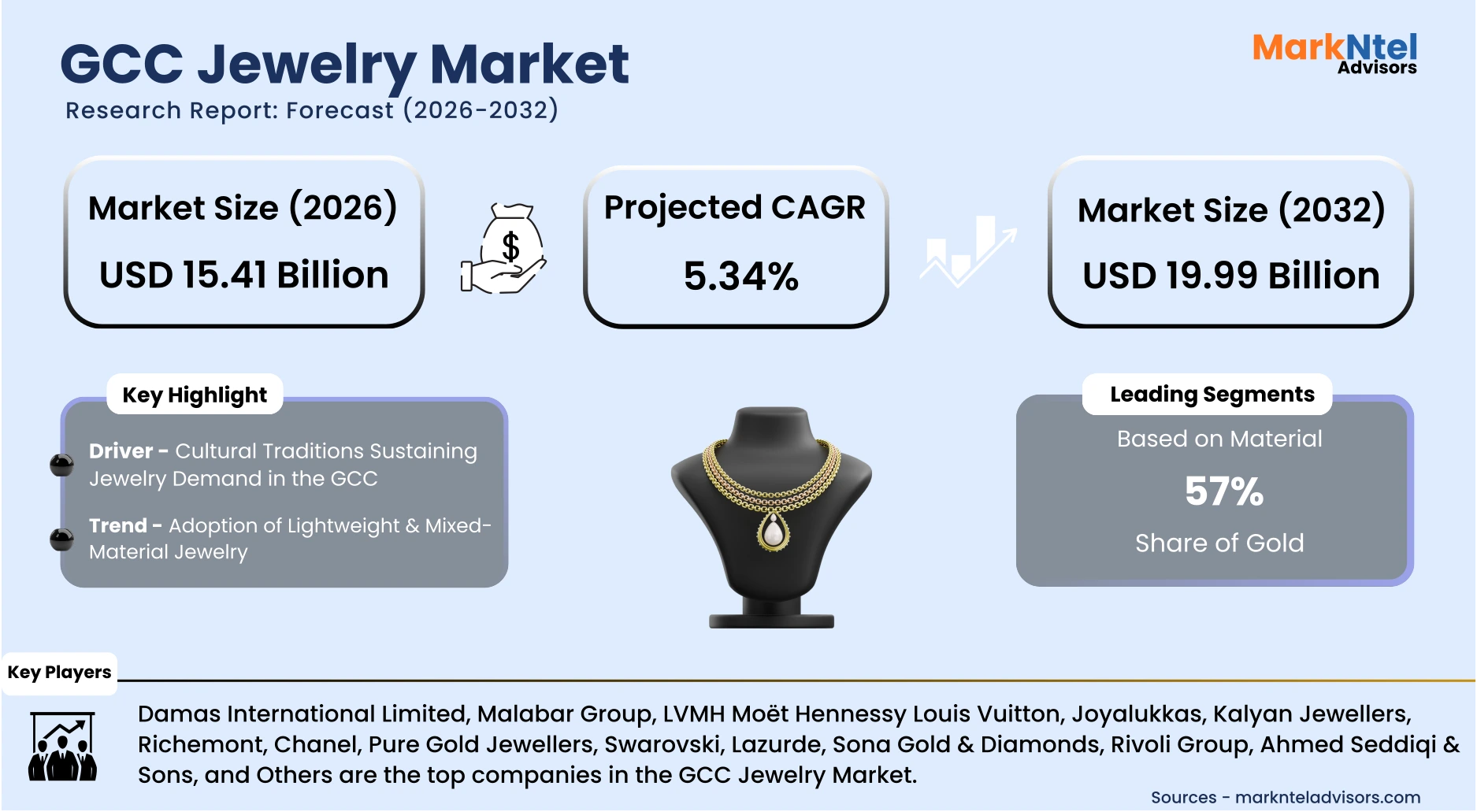

Market Size (2026)

USD 15.41 Billion

Market Size (2032)

USD 19.99 Billion

Base Year

2025

Projected CAGR

5.34%

Leading Segments

By Material: Gold

GCC Jewelry Market Report Key Takeaways:

- Market size was valued at around USD 14.63 billion in 2025 and is projected to grow from USD 15.41 billion in 2026 to USD 19.99 billion by 2032, exhibiting a CAGR of 5.34% during the forecast period.

- Saudi Arabia holds the largest market share of about 44% in the GCC Jewelry Market in 2026.

- By Material, the Gold segment represented a significant share of about 57% in the GCC Jewelry Market in 2026.

- By End-User, the Bridal & Weddings segment presented a significant share of about 36% in the GCC Jewelry Market in 2026.

- Leading Jewelry Companies in the GCC are Damas International Limited, Malabar Group, LVMH Moët Hennessy Louis Vuitton, Joyalukkas, Kalyan Jewellers, Richemont, Chanel, Pure Gold Jewellers, Swarovski, Lazurde, Sona Gold & Diamonds, Rivoli Group, Ahmed Seddiqi & Sons, and others.

Market Insights & Analysis: GCC Jewelry Market (2026-32):

The GCC Jewelry Market size was valued at approximately USD 14.63 billion in 2025 and is projected to grow from USD 15.41 billion in 2026 to USD 19.99 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 5.34% during the forecast period, i.e., 2026-32.

The market expansion is structurally supported by sustained gold trade flows, rising luxury tourism, and culturally anchored bridal expenditure across Saudi Arabia and the UAE. According to the World Gold Council, Middle East gold jewelry demand reached nearly 190 tons in 2023, with GCC economies accounting for a substantial share of this volume. At the same time, Dubai Customs reported the UAE’s gold trade surpassed USD 129 billion in 2023, reinforcing the region’s position as a global bullion redistribution hub.

Together, strong consumption demand and high trade liquidity create a balanced ecosystem that supports both retail growth and supply stability. Building upon this trade foundation, upstream mining and refining investments are now strengthening regional supply security. Saudi Arabia’s Ministry of Industry and Mineral Resources accelerated mining licensing reforms in 2024 under Vision 2030 to expand domestic gold production capacity. For instance, Ma’aden’s Mansourah–Massarah mine is designed to produce approximately 250,000 ounces of gold annually, directly supporting downstream fabrication and reducing reliance on imported doré.

As a result, deeper vertical integration is improving value capture within the GCC while stabilizing raw material availability for jewelers. Moreover, the emirate welcomed over 17 million international visitors in 2023, significantly boosting luxury retail turnover.

Similarly, Saudi Arabia recorded over 100 million domestic and international visits in 2023, which directly stimulated bridal, gifting, and festive jewelry purchases . Consequently, tourism-driven factor is not merely increasing sales volumes but also elevating average transaction values in the gold and diamond segments. To sustain profitability amid rising competition and bullion price volatility, manufacturers and retailers are accelerating digitization and operational modernization. For instance, Lazurde initiated production optimization measures in 2024 to enhance fabrication efficiency and cost control in Saudi Arabia.

In parallel, leading retailers are integrating real-time gold pricing mechanisms and omnichannel inventory systems to improve transparency and customer trust. Collectively, this alignment between trade liquidity, mining expansion, tourism inflows, and digital transformation forms a cohesive growth framework underpinning the market growth through 2032.

GCC Jewelry Market Recent Developments:

- 2025 : Titan Company announced the acquisition of a 67% stake in Dubai-based Damas Jewelry for approximately USD 283.2 million to strengthen its GCC jewelry foothold, gaining access to Damas’ 146 stores across six Gulf Cooperation Council countries.

- 2025 : Malabar Gold & Diamonds announced an expansion phase to open 48 showrooms globally, including new retail experiences and revamped stores, reinforcing its presence in the UAE, Oman, and other key markets.

GCC Jewelry Market Scope:

| Category | Segments |

|---|---|

| By Type | (Rings, Necklaces, Chains, Bangles, Bracelets, Earrings, Pendants, Anklets, Brooches, Cufflinks, Charms, Coins, Bars, Others), |

| By Material Type | (Gold, Diamond, Gemstone, Pearl, Platinum, Silver, Fashion / Costume), |

| By Distribution Channel | (Offline, Online), |

| By Price Range | (Ultra-Luxury (Above USD 50,000), Luxury (USD 10,000 – USD 50,000), Premium (USD 2,500 – USD 10,000), Mass Market (Below USD 500)), |

| By End-Use | (Bridal & Wedding, Festive & Cultural, Daily Wear, Gifting, Investment), |

GCC Jewelry Market Driver:

Cultural Traditions Sustaining Jewelry Demand in the GCC

Cultural customs remain a central force shaping jewelry demand across Saudi Arabia, the UAE, and Oman. Gold jewelry is closely associated with weddings, dowry exchanges, and festive gifting, ensuring repeated purchases throughout the year. In many GCC households, bridal ceremonies involve the presentation of multiple gold sets and bangles, reinforcing high transaction values during marriage seasons. These traditions create structurally recurring demand rather than purely discretionary luxury spending.

Additionally, according to the World Gold Council, gold jewelry demand in the Middle East accounted for a significant share of global jewelry consumption in recent years, with Gulf economies contributing meaningfully to regional volumes. This demonstrates how cultural practices continue to anchor buying behavior even during periods of economic uncertainty. Moreover, the GCC’s role as a global bullion hub supports this tradition. The Dubai Multi Commodities Centre (DMCC) has consistently highlighted the UAE’s position among the world’s leading gold trading centers, ensuring stable access to refined gold for retail markets.

GCC Jewelry Market Trend:

Adoption of Lightweight & Mixed-Material Jewelry

The rapid adoption of lightweight and mixed-material jewelry is reshaping the GCC Jewelry Market due to the rise of lightweight and mixed-material jewelry, designs that blend lighter gold content with diamonds, gemstones, and contemporary styling to meet evolving consumer preferences. This trend reflects changing purchase behavior among younger, style-oriented buyers in Saudi Arabia, the UAE, and Oman, who increasingly prioritize design versatility and everyday wearability over sheer gold weight.

For instance, in 2025, Damas International Limited expanded its 18K diamond-accented “Signature Lace” collection, featuring delicate motifs and reduced gold weight for versatile wear. Similarly, in 2025, Joyalukkas introduced the Evora diamond collection, characterized by fluid diamond arrangements integrated with lighter gold structures across rings, necklaces, and bracelets. In Saudi Arabia, Lazurde increased production of its “Layali” mixed-metal series in 2025, combining 18K gold with platinum and colored gemstones in lightweight daily-wear pieces.

These product innovations illustrate how GCC retailers are diversifying offerings to enhance aesthetic appeal while maintaining cultural relevance. By prioritizing design quality and stone integration over gold weight, industry players are expanding their market reach across lifestyle and premium segments, marking a sustained trend toward contemporary jewelry consumption.

GCC Jewelry Market Opportunity:

Government-Led Local Manufacturing Scale-Up

Government-driven industrial strategies across the GCC are increasingly aligning upstream mining, bullion trade, and downstream jewelry fabrication to strengthen domestic value creation. In Saudi Arabia, the Ministry of Industry and Mineral Resources launched a USD 182 million mineral exploration incentive program in 2024 to accelerate gold exploration and reduce long-term import dependence. For instance, subsequent licensing rounds attracted additional private commitments exceeding USD 90 million, reinforcing the upstream pipeline. This directly supports domestic jewelers by ensuring greater raw material security and price stability.

Simultaneously, the UAE continues to function as the regional bullion backbone. Dubai Multi Commodities Centre reported that the UAE’s precious-metals trade reached approximately USD 170 billion in 2024, reflecting strong inflows of raw gold for refining and re-export. This high-volume throughput enables free-zone manufacturers to scale fabrication efficiently and supply both domestic retailers and neighboring GCC markets with shorter lead times.

GCC Jewelry Market Challenge:

Heavy Reliance on Imported Diamonds and Precious Gemstones

A fundamental challenge in this market is its deep reliance on imported diamonds and gemstones, as domestic mining of these stones remains extremely limited across GCC countries like Saudi Arabia, the UAE, and Oman. Consequently, the region depends on global extraction and trading hubs to sustain bridal and luxury demand. For instance, according to 2024 international trade data, the United Arab Emirates imported approximately USD 10.2 billion worth of diamonds, ranking among the world’s largest diamond importers. These diamonds are primarily sourced from Botswana, Russia, South Africa, and Canada, linking GCC retail performance directly to African and Eurasian mining output.

Beyond rough stones, the supply chain extends to international cutting and polishing centers. For reference, India exported about USD 7.3 billion worth of pearls, precious stones, and precious metals to the UAE in 2024, reflecting the GCC’s dependence on Indian diamond processing facilities. Additionally, gemstones such as rubies and sapphires are routed through trading hubs including Thailand, Sri Lanka, Hong Kong, and Belgium (Antwerp), etc., which further create high margin-sensitive and supply-risk challenges across the regional jewelry ecosystem.

GCC Jewelry Market (2026-32) Segmentation Analysis:

The GCC Jewelry Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Material:

- Gold

- 24 Karat

- 22 Karat

- 21 Karat

- 18 Karat

- Below 18 Karat

- Diamond

- Gemstone

- Precious Stones

- Ruby

- Emerald

- Sapphire

- Others

- Semi-Precious Stones

- Precious Stones

- Pearl

- Natural Pearl

- Cultured Pearl

- Platinum

- Silver

- Fashion / Costume

Gold dominates the GCC jewelry market because consumption is widespread across all member states. Gold represents 57% of total material revenue in the region, supported by strong cultural and investment-driven demand. According to the World Gold Council, the UAE consumed 39.7 tons of gold jewelry in 2023, placing it among the leading global markets . Similarly, Saudi Arabia also recorded significant jewelry demand, reflecting strong bridal and festive purchases.

Smaller GCC markets also contribute meaningfully. In 2023, Kuwait consumed approximately 8.5 tons, Qatar around 6.4 tons, Oman about 5.3 tons, and Bahrain roughly 3.0 tons of gold jewelry, according to the World Gold Council. Although these volumes are lower than in the UAE and Saudi Arabia, high per-capita ownership levels and strong wedding traditions sustain consistent demand across these markets.

This broad-based regional consumption feeds into the UAE’s bullion trade ecosystem, where large-scale refining and re-export operations ensure steady gold availability. Together, high physical demand across all GCC countries reinforces gold’s structural dominance in the regional jewelry market.

Based on End-Use:

- Bridal & Wedding

- Festive & Cultural

- Daily Wear

- Gifting

- Investment

- Others (Corporate, Institutional, etc.)

The bridal and weddings segment is the structural backbone of the GCC Jewelry Market, with a market share of about 36% because gold jewelry is deeply embedded in marriage customs, dowry traditions, and wealth preservation practices across Gulf societies. For instance, the Middle Eastern jewelry demand reached 171 tons in 2023, with Saudi Arabia alone contributing a high share, making it the region’s largest gold jewelry consumer. This scale is significant relative to population size and is largely supported by wedding-related purchases.

For reference, in Q1 2025, Saudi gold jewelry demand increased 35% year-on-year , despite high global gold prices. This resilience indicates that wedding-linked buying is culturally non-discretionary rather than purely price-sensitive. Additionally, in GCC countries such as the UAE and Qatar, 21-22 karat bridal gold sets are traditionally purchased as part of marriage settlements and ceremonial gifting, reinforcing high-value transactions per wedding.

Similarly, official Saudi point-of-sale data frequently show jewelry among the top retail categories during peak wedding and festive seasons. The consistent linkage between cultural obligation, financial security, and ceremonial spending makes bridal jewelry not a seasonal niche but the dominant and recurring revenue driver across the GCC jewelry market.

GCC Jewelry Market (2026-32): Regional Projection

Saudi Arabia dominates the GCC Jewelry Market with a market share of about 44% due to its scale of gold consumption, expanding mining capacity, strong import flows, and structurally high bridal demand. For instance, as per the World Gold Council, Saudi Arabia’s gold jewelry demand reached approximately 38 tons in 2023, positioning it among the largest markets in the Middle East. Additionally, despite gold prices exceeding thousands of dollars per ounce in 2024, Saudi demand remained resilient, underscoring the cultural centrality of gold in weddings and festive occasions.

Additionally, Saudi Arabia holds approximately 323 tons of official gold reserves , as reported by the World Gold Council and reflected in central bank data, strengthening macroeconomic stability and consumer confidence in gold ownership.

Similarly, World Bank trade statistics show Saudi exports of jewelry articles to the UAE reached roughly USD 445 million in 2024, highlighting its leadership in intra-GCC trade flows. Together, high domestic consumption, sovereign reserve strength, upstream mining expansion, and tourism-driven luxury retail activity consolidate Saudi Arabia’s leading position within the GCC jewelry ecosystem.

Gain a Competitive Edge with Our GCC Jewelry Market Report:

- GCC Jewelry Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- GCC Jewelry Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Jewelry Market Policies, Regulations, and Product Standards

- GCC Jewelry Market Trends & Developments

- GCC Jewelry Market Dynamics

- Growth Factors

- Challenges

- GCC Jewelry Market Hotspot & Opportunities

- GCC Jewelry Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Rings

- Necklaces

- Chains

- Bangles

- Bracelets

- Earrings

- Pendants

- Anklets

- Brooches

- Cufflinks

- Charms

- Coins

- Bars

- Others

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- Gold

- 24 Karat

- 22 Karat

- 21 Karat

- 18 Karat

- Below 18 Karat

- Diamond

- Gemstone

- Precious Stones

- Ruby

- Emerald

- Sapphire

- Others

- Semi-Precious Stones

- Precious Stones

- Pearl

- Natural Pearl

- Cultured Pearl

- Platinum

- Silver

- Fashion / Costume

- Gold

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- Offline

- Exclusive Brand Boutiques

- Multi-Brand Jewelry Retailers

- Traditional Gold Souks

- Department Stores

- Hypermarkets

- Online

- Brand-Owned E-commerce Platforms

- Third-Party Marketplaces

- Social Commerce

- Offline

- By Price Range- Market Size & Forecast 2022-2032, USD Million

- Ultra-Luxury (Above USD 50,000)

- Luxury (USD 10,000 – USD 50,000)

- Premium (USD 2,500 – USD 10,000)

- Mass Market (Below USD 500)

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Bridal & Wedding

- Festive & Cultural

- Daily Wear

- Gifting

- Investment

- Others (Corporate, Institutional, etc.)

- By Country

- UAE

- Saudi Arabia

- Oman

- Kuwait

- Qatar

- Bahrain

- Rest of GCC

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Jewelry Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Range- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Jewelry Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Range- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Oman Jewelry Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Range- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kuwait Jewelry Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Range- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Qatar Jewelry Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Range- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Bahrain Jewelry Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Range- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- GCC Jewelry Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Damas International Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Malabar Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LVMH Moët Hennessy Louis Vuitton SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Joyalukkas Holdings

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kalyan Jewellers

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Richemont SA, Cie Financière

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chanel SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pure Gold Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Swarovski AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lazurde

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sona Gold & Diamonds

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rivoli Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ahmed Seddiqi & Sons

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Damas International Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now