GCC Food Waste Management Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Waste Type (Fruits & Vegetables, Dairy & Dairy Products, Cereals & Grains, Meat & Poultry, Fish & Seafood, Processed Foods, Others), By Management Process (Aerobic Digestion, An ... aerobic Digestion, Combustion/Incineration, Others), By Service Type (Collection, Transportation, Disposal/Recycling), By Source (Primary Food Producers, Food Manufacturers, Food Distributors and Suppliers, Food Service Providers, Municipalities and Households), By Application (Animal Feed, Fertilizers, Biofuel & Biogas, Power Generation, Others), By End User (Municipal Authorities / Governments, Private Waste Management Firms, Food Manufacturers & Processors, Retailers & Food Service Chains, Household Consumers), and others Read more

- Food & Beverages

- Feb 2026

- Pages 225

- Report Format: PDF, Excel, PPT

GCC Food Waste Management Market

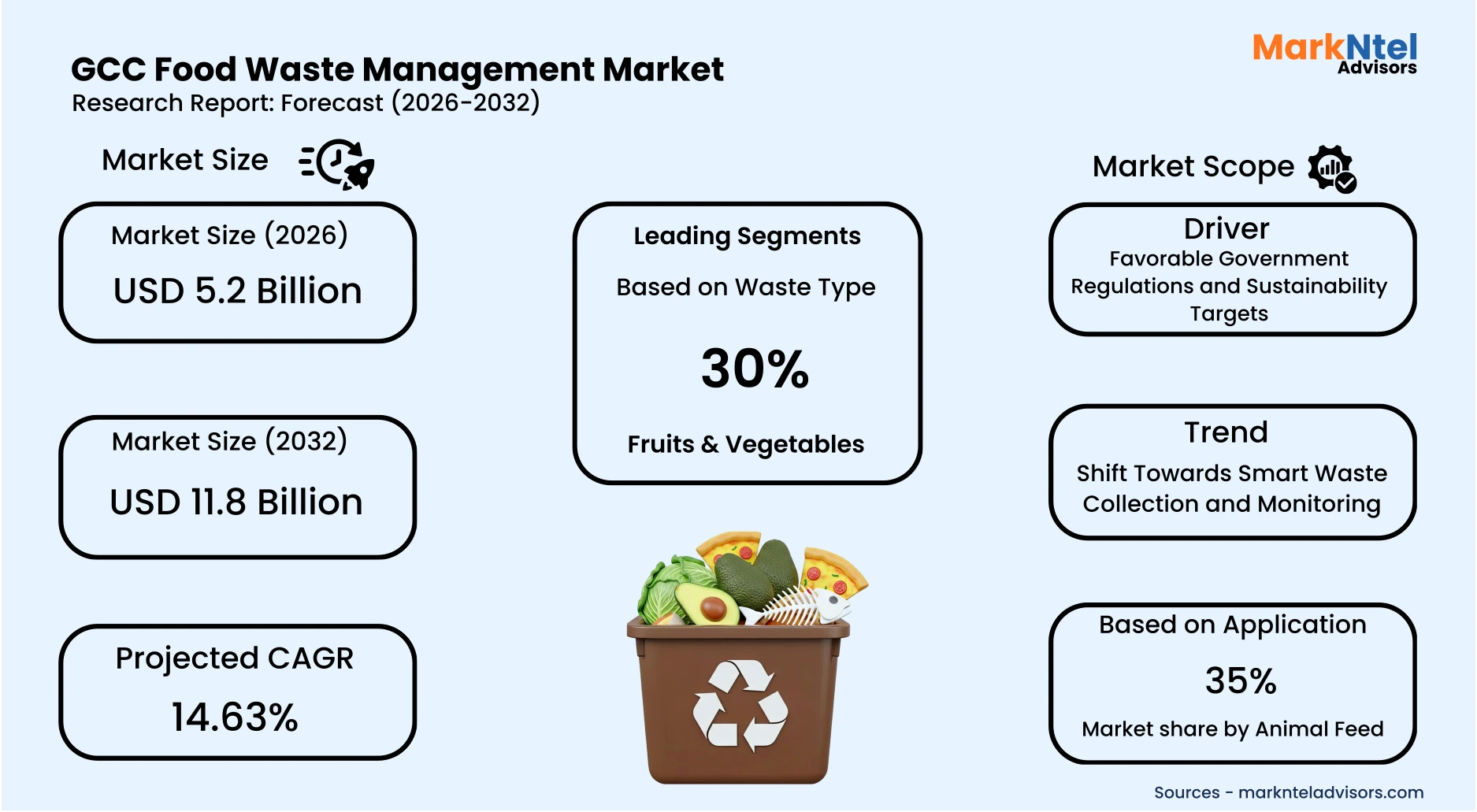

Projected 14.63% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 5.2 Billion

Market Size (2032)

USD 11.8 Billion

Base Year

2025

Projected CAGR

14.63%

Leading Segments

By Application: Animal Feed

GCC Food Waste Management Market Report Key Takeaways:

- The GCC Food Waste Management market size was valued at USD 4.8 billion in 2025 and is projected to grow from USD 5.2 billion in 2026 to USD 11.8 billion by 2032, exhibiting a CAGR of 14.63% during the forecast period.

- Saudi Arabia holds the largest market share of about 38% in the GCC Food Waste Management Market in 2026.

- By waste type, the fruits & vegetables segment represented a significant share of about 30% in the GCC Food Waste Management Market in 2026.

- By management process, the anaerobic digestion segment presented a significant share of about 32% in the GCC Food Waste Management Market in 2026.

- By application, the animal feed segment holds a significant share of about 35% in the GCC Food Waste Management Market in 2026.

- Leading food waste management companies in the GCC Market are BEEAH Group, Tadweer Group, Averda, SUEZ Middle East Recycling LLC, Veolia Middle East, Saudi Investment Recycling Company (SIRC), Dulsco Environment, Envac Middle East, Envirol, EDAMA Organic Solutions, Nanjgel Green, EroeGo, and Others.

Market Insights & Analysis: GCC Food Waste Management Market (2026-32):

The GCC Food Waste Management Market size was valued at approximately USD 4.8 billion in 2025 and is projected to grow from USD 5.2 billion in 2026 to USD 11.8 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 14.63% during the forecast period, i.e., 2026-32.

The GCC Food Waste Management Market is projected to expand steadily, driven by strengthening government regulations, ambitious sustainability targets, and the increasing adoption of smart waste collection and monitoring technologies across municipal and commercial sectors.

The GCC Food Waste Management Market is progressing toward a more structured and policy-driven growth trajectory, underpinned by national commitments to United Nations Sustainable Development Goal (SDG) 12.3, which aims to halve per-capita food waste at retail and consumer levels and reduce food losses across supply chains by 2030 . Governments across the region are embedding this target within national sustainability frameworks, reinforcing accountability through measurable benchmarks and institutional oversight.

Saudi Arabia has formally integrated SDG 12.3 into its policy architecture. Under the National Program for Reducing Food Loss and Waste, the Kingdom reported a 16% reduction in food loss and waste by September 2025, supported by the General Food Security Authority (GFSA) and aligned with Vision 2030 environmental objectives.

Similarly, in Qatar, the Food Security Strategy 2030, launched in December 2024, introduces 17 integrated initiatives spanning 2025–2026, focusing on reducing food loss and waste, enhancing supply chain efficiency, strengthening regulatory oversight, promoting sustainable consumption, advancing research partnerships, and reinforcing national food system resilience in alignment with Qatar National Vision 2030.

The UAE is reinforcing regulatory planning through data-backed policymaking. The national ne’ma initiative is conducting the country’s first food loss and waste baseline assessment involving 3,000 participants, with findings expected in the first half of 2026 to establish standardized food waste indices. Complementing this effort, the UAE Food Bank launched a nationwide awareness programme in early 2026 to encourage responsible consumption and structured surplus redistribution.

Infrastructure expansion is also accelerating. Under the GCC Waste-to-Energy cooperation framework, Bahrain’s Askar 25 MW biopower project supports methane recovery and biomass energy generation from organic waste streams.

Meanwhile, anaerobic digestion accounted for approximately 32% of the GCC Food Waste Management Market in 2026 , reflecting growing emphasis on landfill diversion and renewable energy integration.

Digitalization further strengthens the outlook, with Qatar’s TASMU Smart Qatar initiative deploying real-time smart waste monitoring systems to optimize collection efficiency and inform national waste planning.

Strengthening regulatory mandates, measurable reduction targets, renewable energy integration, and digital waste governance are collectively formalizing the GCC food waste management ecosystem. These structural advancements position the market for sustained institutional investment and long-term expansion through 2030.

GCC Food Waste Management Market Recent Developments:

- 2025: Dubai’s Tadweer Waste Management facility showcased a significant breakthrough in waste-to-energy technology, highlighting its pilot biogas plant that converts organic and food waste into renewable energy. The facility, visited by Dubai Municipality officials, demonstrates the potential of organic waste valorization to reduce landfill dependency and support the Dubai Integrated Waste Management Strategy 2021–2041 and Clean Energy Strategy 2050.

GCC Food Waste Management Market Scope:

| Category | Segments |

|---|---|

| By Waste Type | (Fruits & Vegetables, Dairy & Dairy Products, Cereals & Grains, Meat & Poultry, Fish & Seafood, Processed Foods, Others), |

| By Management Process | (Aerobic Digestion, Anaerobic Digestion, Combustion/Incineration, Others), |

| By Service Type | (Collection, Transportation, Disposal/Recycling), |

| By Source | (Primary Food Producers, Food Manufacturers, Food Distributors and Suppliers, Food Service Providers, Municipalities and Households), |

| By Application | (Animal Feed, Fertilizers, Biofuel & Biogas, Power Generation, Others), |

| By End User | (Municipal Authorities / Governments, Private Waste Management Firms, Food Manufacturers & Processors, Retailers & Food Service Chains, Household Consumers), |

GCC Food Waste Management Market Driver:

Favorable Government Regulations and Sustainability Targets

Government-backed food waste reduction targets are emerging as a key structural driver of the GCC Food Waste Management Market. In the United Arab Emirates (UAE), the Ministry of Climate Change and Environment has institutionalized its commitment to SDG 12.3 through the Ne’ma National Food Loss and Waste Initiative, which aims to reduce food waste by 50% by 2030 .

A central component of this initiative is an 18-month nationwide baseline study covering 3,000 households and businesses across all seven Emirates, with results expected in 2026. The study will establish standardized national food loss and waste indices to guide evidence-based regulatory interventions and infrastructure planning.

The UAE’s approach is integrated within its broader National Food Security Strategy 2051, reinforcing long-term government prioritization of sustainable consumption and production across supply chains. This institutional alignment ensures that food waste reduction is embedded within national economic diversification and environmental sustainability frameworks.

Similarly, Saudi Arabia has incorporated SDG 12.3 within Vision 2030, targeting a 50% reduction in food loss and waste by 2030 as part of its circular economy transition in the food sector . These measurable commitments necessitate expanded segregation systems, monitoring technologies, redistribution networks, and organic waste treatment infrastructure.

Formal national targets backed by regulatory oversight and structured measurement frameworks are accelerating investment in food waste management systems. As implementation intensifies toward 2030, these policy commitments will continue to stimulate sustained market growth across the GCC.

GCC Food Waste Management Market Trend:

Shift Towards Smart Waste Collection and Monitoring

Digital transformation of municipal waste systems is emerging as a defining trend across the GCC, strengthening efficiency and supporting long-term sustainability mandates. Governments are increasingly adopting sensor-based monitoring solutions to improve collection logistics, reduce operational expenditure, and enhance waste diversion performance.

In Qatar (2023–2024), the Ministry of Municipality deployed more than 7,000 smart waste containers integrated with fill-level sensors, alongside digital monitoring systems installed in approximately 1,000 municipal cleaning vehicles. These technologies enable real-time tracking of bin capacity and dynamic route optimization, ensuring collection occurs only when necessary. This reduces redundant vehicle movement, lowers fuel consumption, and improves service productivity within the national waste management framework.

Kuwait City has similarly introduced sensor-enabled smart bins capable of transmitting real-time data to municipal control centers . The system supports demand-based collection scheduling, contributing to improved route planning and cost efficiencies while strengthening oversight of municipal waste flows.

These initiatives are aligned with broader regional landfill diversion and recycling objectives, including the UAE’s ambition to divert up to 75% of waste away from landfills, which requires enhanced monitoring and segregation efficiency.

The expansion of smart collection infrastructure enhances transparency, operational efficiency, and data-driven policy implementation. As digital waste governance scales across the GCC, technology-enabled monitoring systems are expected to play a pivotal role in advancing food waste management efficiency and overall market development.

GCC Food Waste Management Market Opportunity:

Development of Waste-to-Energy (WtE) Projects

The development of large-scale organic waste-to-energy infrastructure presents a significant growth opportunity for the GCC food waste management market. In 2025, Oman Environmental Services Holding Company (be’ah) entered into a strategic agreement with OQ Trading to develop a national biogas project aimed at converting organic waste, including food waste disposed of in landfills, into renewable energy. The project is expected to generate approximately 20 million cubic meters of biogas annually, comprising nearly 40% biomethane suitable as a renewable fuel and 60% bio-CO₂ for industrial applications. By capturing methane from decomposing organic waste, the initiative directly reduces greenhouse gas emissions while transforming waste streams into commercially viable energy products.

This development aligns with Oman Vision 2040, which prioritizes environmental sustainability, circular economy integration, and diversification of renewable energy sources. The project roadmap includes technical feasibility assessments, infrastructure planning, and phased commercial deployment, establishing a structured foundation for expanding bioenergy capacity. Importantly, large-scale biogas generation requires improved organic waste segregation and systematic collection, reinforcing the need for advanced food waste management systems.

Oman’s biogas initiative demonstrates a clear linkage between food waste management and renewable energy development. As regulatory support and infrastructure scale up, organic waste valorization projects will significantly accelerate growth in the GCC food waste management market.

GCC Food Waste Management Market Challenge:

Fragmented Waste Collection and Segregation

A core challenge in the GCC food waste management market is the fragmentation of waste collection systems and weak segregation practices at the source, which significantly reduce the effectiveness of food and organic waste treatment.

Without consistent separation of food waste from other municipal waste streams at the household, commercial, and institutional levels, organic fractions often become contaminated, complicating downstream processing such as composting or anaerobic digestion.

Governments across the region have recognized that source segregation infrastructure remains underdeveloped; a World Bank assessment notes that existing waste management systems in Middle Eastern countries, including those of the GCC, are dominated by landfilling with limited sorting and material recovery facilities, undermining organic waste recovery efforts.

Despite ambitious recycling targets, including the UAE’s goal to recycle up to 75% of municipal waste, food waste segregation remains limited. The absence of unified collection protocols and mandatory source separation results in organic waste mixing with general waste, lowering feedstock quality and increasing processing costs for treatment facilities.

Fragmented collection and segregation practices hinder efficient capture and treatment of food waste, constraining the performance of composting and bioenergy technologies and slowing the expansion of organized food waste management infrastructure across the GCC.

GCC Food Waste Management Market (2026-32) Segmentation Analysis:

The GCC Food Waste Management Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Waste Type:

- Fruits & Vegetables

- Dairy & Dairy Products

- Cereals & Grains

- Meat & Poultry

- Fish & Seafood

- Processed Foods

- Others

The fruits & vegetables segment dominates the GCC Food Waste Management market, holding around 30% market share, primarily due to its inherent perishability and substantial contribution to overall food waste volumes.

Fresh produce is highly susceptible to spoilage caused by temperature variability, logistical inefficiencies, and extended transportation timelines. Given the GCC’s reliance on imported fruits and vegetables and exposure to extreme climatic conditions, maintaining an uninterrupted cold-chain infrastructure remains operationally critical. Any disruption in storage or distribution significantly increases product deterioration rates.

At the retail and hospitality levels, quality grading standards, aesthetic preferences, and overstocking practices further contribute to discard volumes. Unlike packaged or shelf-stable food categories such as cereals or processed goods, fresh produce has limited storage life and lower tolerance to handling stress, resulting in accelerated wastage across wholesale markets, supermarkets, and food service establishments.

From a waste processing perspective, fruits and vegetables form a substantial portion of the organic waste stream, making them a key input for composting and anaerobic digestion facilities. Their high moisture and biodegradable content facilitate rapid decomposition, increasing the need for timely collection and structured treatment systems.

Consequently, the combination of high spoilage risk, supply chain vulnerability, and dominant presence in organic waste streams underpins the leadership of the Fruits & Vegetables segment within the GCC food waste management market.

Based on Application:

- Animal Feed

- Fertilizers

- Biofuel & Biogas

- Power Generation

- Others

The animal feed segment dominates the GCC Food Waste Management market, accounting for about 35% market share, supported by the region’s strategic emphasis on livestock development and feed security.

GCC countries face structural constraints such as limited arable land, water scarcity, and high reliance on imported feed ingredients. Converting surplus and non-edible food waste into animal feed provides a cost-efficient and resource-optimized alternative that reduces dependency on external supply chains.

Substantial quantities of bakery surplus, fruit and vegetable residues, grain by-products, and food processing discards are technically suitable for feed conversion following appropriate treatment and compliance with safety standards. This pathway not only diverts organic waste from landfills but also supports agricultural productivity by supplying nutritionally viable feed inputs to poultry, dairy, and livestock operations.

Compared to capital-intensive applications such as biofuel production or large-scale power generation, food-to-feed processing generally requires relatively moderate infrastructure investment and shorter operational lead times. The established and consistent demand from the regional livestock sector further strengthens its commercial viability.

Additionally, circular economy policies and food waste reduction strategies across GCC countries encourage resource recovery models that prioritize value retention. As a result, the alignment of economic feasibility, agricultural demand, and sustainability objectives positions the Animal Feed segment as the dominant application within the GCC food waste management market.

GCC Food Waste Management Market (2026-32): Regional Projection

Saudi Arabia dominates the GCC Food Waste Management Market with an estimated 38% share, primarily due to the scale of food waste generation and its associated economic impact. Based on 2023 estimates, approximately 4 million tons of food are wasted annually in the Kingdom, reflecting a 33% food loss and waste rate. The financial implication of this wastage is substantial, with losses valued at nearly around USD 10.6 billion per year, highlighting the significant resource inefficiency embedded within the food value chain.

Staple commodities account for a considerable proportion of discarded volumes. Core food items such as rice, flour, and bread contribute materially to national waste figures, with per capita annual food waste exceeding 184 kg. High consumption patterns, large hospitality and catering sectors, and traditional practices associated with food abundance further amplify waste levels across residential and commercial segments.

The magnitude of these losses has prompted the integration of food waste reduction within broader sustainability and circular economy frameworks under Vision 2030. This has accelerated investments in structured collection systems, redistribution networks, recycling initiatives, and organic waste treatment technologies.

Given its population size, economic capacity, and quantified waste burden, Saudi Arabia commands the largest addressable opportunity for food waste mitigation solutions, reinforcing its leadership position within the GCC market.

Gain a Competitive Edge with Our GCC Food Waste Management Market Report:

- GCC Food Waste Management Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- GCC Food Waste Management Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Food Waste Management Market Policies, Regulations, and Product Standards

- GCC Food Waste Management Market Trends & Developments

- GCC Food Waste Management Market Dynamics

- Growth Factors

- Challenges

- GCC Food Waste Management Market Hotspot & Opportunities

- GCC Food Waste Management Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- Fruits & Vegetables

- Dairy & Dairy Products

- Cereals & Grains

- Meat & Poultry

- Fish & Seafood

- Processed Foods

- Others

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- Aerobic Digestion

- Anaerobic Digestion

- Combustion/Incineration

- Others

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- Collection

- Transportation

- Disposal/Recycling

- Landfill

- Incineration

- Composting

- Others

- By Source - Market Size & Forecast 2022-2032, USD Million

- Primary Food Producers

- Food Manufacturers

- Food Distributors and Suppliers

- Food Service Providers

- Municipalities and Households

- By Application - Market Size & Forecast 2022-2032, USD Million

- Animal Feed

- Fertilizers

- Biofuel & Biogas

- Power Generation

- Others

- By End User- Market Size & Forecast 2022-2032, USD Million

- Municipal Authorities / Governments

- Private Waste Management Firms

- Food Manufacturers & Processors

- Retailers & Food Service Chains

- Household Consumers

- By Country

- The UAE

- Saudi Arabia

- Qatar

- Kuwait

- Oman

- Bahrain

- Rest of GCC

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- The UAE Food Waste Management Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Food Waste Management Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Qatar Food Waste Management Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kuwait Food Waste Management Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Oman Food Waste Management Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Bahrain Food Waste Management Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- GCC Food Waste Management Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- BEEAH Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tadweer Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Averda

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SUEZ Middle East Recycling LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Veolia Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saudi Investment Recycling Company (SIRC)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dulsco Environment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Envac Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Envirol

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EDAMA Organic Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nanjgel Green

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EroeGo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BEEAH Group

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now