GCC Color Cosmetics Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Product Type (Face, Lip, Eye, Nail Cosmetics, Others), By Distribution Channel (Offline Retail, Online Retail, Direct Selling), By Price Product (Mass-Market Products, Prestige ... Premium Products), By Product Formulation (Powder, Cream, Gel, Stick, Liquid), By Value -Proposition (Long Wear, Hydrating, Matte, Natural Finish, Buildable), and others Read more

- FMCG

- Feb 2026

- Pages 180

- Report Format: PDF, Excel, PPT

GCC Color Cosmetics Market

Projected 6.72% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 1.93 Billion

Market Size (2032)

USD 2.77 Billion

Base Year

2025

Projected CAGR

6.72%

Leading Segments

By Price Product: Mass-Market Products

GCC Color Cosmetics Market Report Key Takeaways:

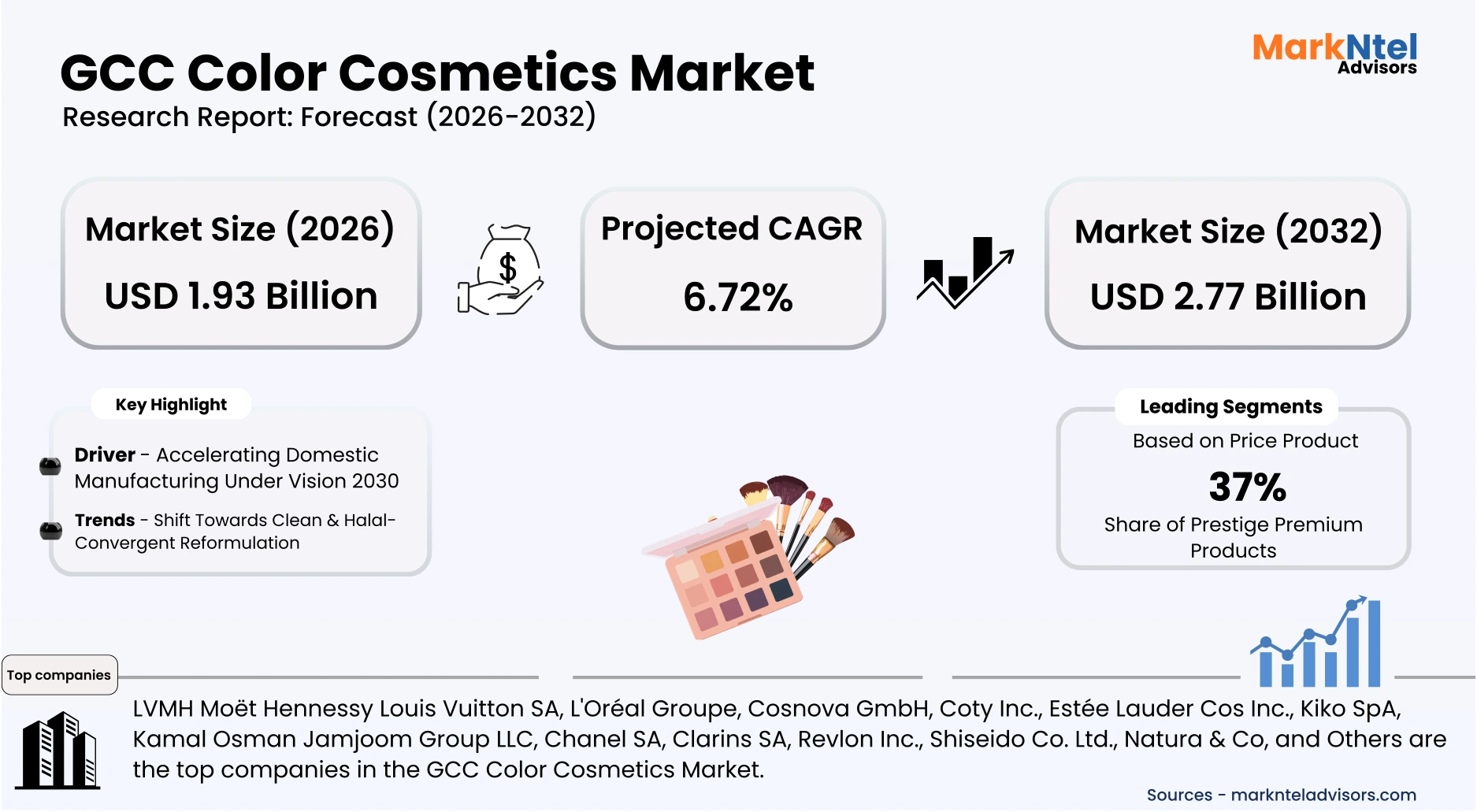

- The GCC Color Cosmetics Market size was valued at USD 1.84 billion in 2025 and is projected to grow from USD 1.93 billion in 2026 to USD 2.77 billion by 2032, exhibiting a CAGR of 6.72%during the forecast period.

- Saudi Arabia is leading the GCC Color Cosmetics Market with a significant share of about 51% in 2026.

- By Product type, the Eyes segment represented a significant share of about 34% in the GCC Color Cosmetics Market in 2026.

- By Price Product, Prestige premium products seized a significant share of about 37% in the GCC Color Cosmetics Market in 2026.

- Leading GCC Cosmetics Companies in the Market are LVMH Moët Hennessy Louis Vuitton SA, L'Oréal Groupe, Cosnova GmbH, Coty Inc., Estée Lauder Cos Inc., Kiko SpA, Kamal Osman Jamjoom Group LLC, Chanel SA, Clarins SA, Revlon Inc., Shiseido Co. Ltd., Natura & Co, and Others.

Market Insights & Analysis: The GCC Color Cosmetics Market (2026-32):

The GCC Color Cosmetics market size was valued at USD 1.84 billion in 2025 and is projected to grow from USD 1.93 billion in 2026 to USD 2.77 billion by 2032, exhibiting a CAGR of 6.72% during the forecast period. i.e., 2026-2032.

The GCC Color Cosmetics Market has demonstrated sustained expansion, supported by resilient non-oil economic growth and favorable demographics across the Gulf Cooperation Council. The World Bank reported continued non-hydrocarbon GDP growth in Saudi Arabia and the UAE in 2025, reinforcing discretionary household expenditure. With urbanization exceeding 85% in the UAE, as indicated by the United Nations, organized retail and e-commerce channels have deepened penetration. Residential end users remain the primary demand base, while premium malls and online platforms have elevated per-capita cosmetics spending.

Government-led diversification strategies have indirectly accelerated beauty sector activity through tourism, entertainment, and retail infrastructure expansion. Saudi Arabia’s Vision 2030 continues to drive private-sector growth and female workforce participation, expanding the addressable consumer base. Regulatory oversight by the Saudi Food and Drug Authority and the Emirates Authority for Standardization and Metrology strengthens product safety compliance and formalizes imports. Commercial and institutional end users, including duty-free operators, hospitality groups, and licensed salons, benefit from rising international visitor arrivals reported by Saudi Arabia’s Ministry of Tourism in 2025.

Industry players are reinforcing regional supply chains and omnichannel capabilities to capture expanding demand. L'Oréal enhanced Middle East distribution operations through its UAE hub, while Estée Lauder Companies scaled digital commerce investments targeting GCC consumers. Regional conglomerate Chalhoub Group continues integrating data analytics and experiential retail across luxury beauty portfolios. These initiatives are consistent with the UAE’s industrial strategy objectives, which prioritize domestic manufacturing expansion, supply chain integration, and higher in-country value creation.

Looking ahead, IMF 2026 growth projections for major GCC economies indicate stable macroeconomic conditions conducive to sustained retail expansion. Population growth, rising female labor participation, and continued mall development are expected to maintain residential consumption momentum. Regulatory modernization and halal-compliant product certification are likely to facilitate cross-border trade within the bloc. Collectively, demographic resilience, infrastructure investment, and coordinated industry-government initiatives position the GCC Color Cosmetics Market for steady medium-term growth.

GCC Color Cosmetics Market Recent Developments:

- 2025: The global cosmetics brand Buxom released its Full-On Lip Satin collection across GCC markets, with availability at major retailers like Sephora Middle East. The range features 10 vibrant satin lip Colors formulated with biomimetic peptides and hyaluronic acid, combining rich pigmentation with hydration and lip-health benefits — an example of hybrid makeup that merges cosmetic performance with skincare-style ingredient benefits.

- 2026: Moonglaze, a Saudi beauty brand founded by makeup artist and influencer Yara Alnamlah, officially launched its full Color cosmetics range at Sephora Middle East, becoming the first Saudi brand to enter Sephora’s GCC retail ecosystem. This historic debut includes blush sticks, bronze pods, highlighter sticks, FEELS lip liners, and MOODS water lip tints products crafted with a skin-first philosophy, emphasizing lightweight, glow-enhancing makeup that suits the region’s climate and beauty demands.

GCC Color Cosmetics Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Face, Lip, Eye, Nail Cosmetics, Others), |

| By Distribution Channel | (Offline Retail, Online Retail, Direct Selling), |

| By Price Product | (Mass-Market Products, Prestige Premium Products), |

| By Product Formulation | (Powder, Cream, Gel, Stick, Liquid), |

| By Value -Proposition | (Long Wear, Hydrating, Matte, Natural Finish, Buildable), |

GCC Color Cosmetics Market Driver:

Accelerating Domestic Manufacturing Under Vision 2030

A key structural driver of the GCC Color Cosmetics Market is the acceleration of domestic manufacturing under Saudi Arabia’s Vision 2030 and related industrial policies. In 2025, the Saudi Ministry of Industry and Mineral Resources supported the launch of automated personal care production lines valued at approximately USD 16 million in the Jeddah First Industrial Zone, expanding blending and packaging capacity for beauty products. Such investments reduce import dependency, shorten distribution lead times, and enhance supply chain resilience for Color cosmetics brands operating in the Kingdom.

The establishment of a halal cosmetics ecosystem further strengthens localized value creation. The Halal Products Development Company announced investment initiatives to develop domestic halal beauty manufacturing capabilities, positioning Saudi Arabia as a regional export hub for compliant personal care products. This aligns with growing demand for certified halal cosmetics across GCC markets and supports cross-border trade within the bloc. By anchoring production locally, manufacturers benefit from industrial incentives, access to logistics infrastructure, and proximity to high-consumption urban centers.

In the UAE, industrial diversification strategies encourage in-country value addition across consumer goods segments, including personal care. Expanded free zone manufacturing ecosystems and advanced logistics infrastructure, particularly in Dubai and Abu Dhabi, facilitate re-export activity and efficient regional distribution. These infrastructure-driven efficiencies directly support commercial end users such as department stores, beauty chains, and duty-free operators by ensuring faster inventory replenishment and broader product assortments.

GCC Color Cosmetics Market Trend:

Shift Towards Clean & Halal-Convergent Reformulation

The GCC Color cosmetics market is undergoing a structural transition toward Clean and Halal-Compliant Hybridization, moving from elective preferences to a regulated baseline. This shift accelerated following the 2025-2026 rollout of stringent Saudi Food and Drug Authority (SFDA) guidelines and Indonesia’s October 2026 mandatory halal certification deadline, which influenced regional trade standards. Consumers now demand "skin-safe" formulations that exclude parabens and silicones, replacing them with breathable, water-permeable ingredients suitable for religious observance and the extreme Gulf climate.

Structurally, this trend is reshaping the entire value chain by forcing a move away from traditional synthetic pigments toward ethically sourced, plant-derived alternatives. Manufacturers are re-engineering operating models to achieve "performance parity," ensuring that organic products match the long-wear capabilities of conventional makeup. For instance, INIKA Organic Full Coverage Liquid Foundation is actively marketed across the UAE and GCC as a high-coverage organic base, available through regional retailers and e-commerce platforms. Formulated with botanical ingredients such as hyaluronic acid and argan oil, it promotes full coverage and long-wear performance, positioning it as a clean alternative to conventional long-wear foundations suited to the Gulf’s hot climate. This demonstrates how organic formulations are being re-engineered to meet performance expectations traditionally associated with mainstream makeup products.

This evolution is expected to persist as a permanent market fixture, driven by a youthful, affluent population with the world's highest per-capita beauty spend.

GCC Color Cosmetics Market Opportunity:

Digital Commerce and Beauty-Tech Integration Accelerating Market Expansion

Digital transformation presents a high-impact opportunity for the GCC Color cosmetics market, supported by strong connectivity infrastructure and consumer readiness. According to the International Telecommunication Union, internet penetration across GCC economies exceeds 95%, enabling widespread access to online retail platforms . The UAE’s Telecommunications and Digital Government Regulatory Authority reports near-universal smartphone adoption, reinforcing mobile-first purchasing behavior. This infrastructure foundation allows cosmetics brands to scale efficiently through direct-to-consumer channels and marketplace platforms.

E-commerce growth is further supported by national digital economy strategies such as Saudi Arabia’s Vision 2030 digital transformation pillar and the UAE’s Digital Economy Strategy. These frameworks promote fintech integration, secure digital payments, and advanced logistics networks, reducing transaction friction and delivery timelines. For cosmetics brands, this environment enhances cross-border sales within the GCC and lowers market entry barriers for niche and independent labels.

Beauty-tech innovation is reshaping online conversion dynamics. Virtual try-on tools, AI-based shade matching, and personalized product recommendations reduce return rates and improve customer confidence in purchasing Color cosmetics digitally. Regional retailers and distributors are investing in data analytics to optimize assortment planning and targeted marketing campaigns. Social commerce, particularly influencer-driven product launches on short-form video platforms, is increasingly influencing purchasing decisions among Gen Z and millennial consumers.

GCC Color Cosmetics Market Challenge:

Regulatory Pressure and Registration Complexity

A key structural challenge in the GCC color cosmetics market stems from country-specific product registration and compliance requirements, despite the presence of harmonized regional standards under the GCC Standardization Organization (GSO) framework.

In practice, cosmetics must undergo separate notification or registration processes with national regulators in each market, including Saudi Food and Drug Authority (SFDA) – Saudi Arabia, Dubai Municipality, United Arab Emirates, Kuwait Ministry of Health – Kuwait, Qatar Ministry of Public Health – Qatar, Oman Ministry of Health – Oman, National Health Regulatory Authority (NHRA) – Bahrain. Each authority typically mandates Arabic-language labelling, Country-specific importer/distributor details, Ingredient disclosure and safety documentation, and separate registration for product variants or shade extensions.

As a result, brands often cannot use a single unified GCC packaging format. Minor differences in regulatory wording, barcode registration, or importer identification necessitate country-differentiated SKUs, even when the formulation remains identical. This regulatory fragmentation creates increased SKU proliferation and production complexity, Higher warehousing and working capital requirements, Limited flexibility to redistribute inventory across GCC markets, and greater risk of overstocking slow-moving shades in specific countries.

For color cosmetics, particularly fast-cycle segments such as lipsticks, foundations, and limited-edition launches, this compliance-driven segmentation reduces supply chain agility and raises operational costs. Consequently, regulatory management capability becomes not only a compliance function but a critical determinant of margin protection and regional scalability.

GCC Color Cosmetics Market (2026-32) Segmentation Analysis:

The GCC Color Cosmetics Market study of MarkNtel Advisors evaluates and highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as follows:

Based on Product Type:

- Face

- Lip

- Eye

- Nail Cosmetics

- Others

The eye cosmetics segment in the GCC market demonstrates robust growth with a market share of 34%, driven by evolving beauty norms and increasing consumer focus on expressive makeup styles. Demand for mascaras, eyeliners, and eyeshadows has outpaced several other categories due to a cultural emphasis on eye-focused beauty, especially in regions where face coverings have historically elevated the importance of eye makeup in daily wear. Rising social media influence and influencer-led tutorials have educated end-users on advanced eye makeup techniques, expanding both product usage frequency and variety. This heightened consumer sophistication has encouraged retailers to widen assortments, particularly in premium and long-wear formulations.

On the policy and regulatory front, GCC governments have streamlined import standards for cosmetic pigments and preservatives, reducing barriers for international eye makeup brands to enter and scale. Harmonized Gulf Conformity Mark (G-Mark) requirements have improved supply chain predictability, encouraging multinationals to increase regional investments in product launches tailored to GCC preferences. These regulatory efficiencies , combined with rising foreign direct investment into beauty retail infrastructure, have enhanced product availability across urban and secondary markets. As a result, market players are allocating larger shares of marketing spend to eye cosmetic sub-segments, further stimulating consumer demand.

End-user segmentation shows strong adoption among younger demographics and working professionals who value both expressive and long-lasting formulations. Retailer data indicate that color-intensive products with multifunctional benefits (e.g., lash-care infused mascaras, smudge-resistant eyeliners) command higher repeat purchase rates. Together with seasonal demand peaks tied to cultural events and festival gifting, these trends underpin sustained growth in the eye cosmetics segment. Continued innovation and targeted regional marketing initiatives are expected to reinforce this trajectory over the forecast period.

Based on Price Product:

- Mass-Market Products

- Prestige Premium Products

Across the GCC, prestige premium Color cosmetics retain the highest value share with a market share of 37%, driven by high disposable incomes, luxury retail orientation, and aspirational consumer behaviors. The International Monetary Fund’s 2025 regional outlook highlights robust per-capita income levels in Saudi Arabia, the UAE, and Qatar, underpinning discretionary spending on luxury and premium categories. Premium brands command a strong presence in high-traffic retail environments such as The Avenues (Kuwait), The Pearl (Qatar), and Mall of Arabia (Saudi Arabia), where luxury cosmetics boutiques and multi-brand chains dominate shelf space. Additionally, GCC tourism expansion, evidenced by documented increases in international arrivals to Riyadh and Dubai, fuels demand for prestige products via duty-free and travel retail channels. Retailers in the region increasingly host exclusive launches and limited-edition releases from global beauty conglomerates, reinforcing premium positioning and driving higher customer acquisition costs.

GCC Color Cosmetics Market (2026-32) Regional Analysis:

Saudi Arabia has become the leading Color cosmetics market in the GCC with a market share of 51% due to its very high import volumes, strong regulatory frameworks, and extensive distribution networks that support consumer access and market intensity. According to World Bank data, Saudi Arabia imported beauty, make-up, skin-care, and similar products in 2023 among the highest import values on record for a single country in the region. France, the UAE, the United States, and Italy were the top exporters supplying those products to Saudi Arabia, indicating broad global sourcing for makeup and related Color cosmetics.

The Saudi Food and Drug Authority (SFDA) tightly regulates cosmetics imports and sales. All cosmetic products must be listed and certified via SFDA’s eCosma/FASEH systems before clearance, ensuring safety, standardized labelling, and ingredient compliance. This regulatory rigor has attracted major international brands that adhere to SFDA standards, reinforcing Saudi Arabia’s leadership role.

Saudi Arabia’s Color cosmetics leadership in the GCC isn’t just about consumption; it is backed by strong corporate presence, local operations by global beauty giants, e.g., L’Oréal’s Saudi subsidiary, and widespread retail infrastructure capturing both mass and premium makeup demand. This combination differentiates Saudi Arabia from neighboring GCC states in market intensity and strategic importance for global brands.

Because local large-scale Color pigment or cosmetics chemical production remains limited, the Kingdom relies on global suppliers for raw materials and finished products, but its strong trade connectivity and regulatory infrastructure continue to support high demand and market dominance in the GCC for Color cosmetics.

Gain a Competitive Edge with Our GCC Color Cosmetics Market Report:

- The GCC Color Cosmetics Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The GCC Color Cosmetics Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Color Cosmetics Market Policies, Regulations, and Product Standards

- GCC Color Cosmetics Market Trends & Developments

- GCC Color Cosmetics Market Dynamics

- Growth Factors

- Challenges

- GCC Color Cosmetics Market Hotspot & Opportunities

- GCC Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Face

- Lip

- Eye

- Nail Cosmetics

- Others

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- Offline Retail

- Online Retail

- Direct Selling

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- Mass-Market Products

- Prestige Premium Products

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- Powder

- Cream

- Gel

- Stick

- Liquid

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Long Wear

- Hydrating

- Matte

- Natural Finish

- Buildable

- By Country

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates (UAE)

- Rest of GCC

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Bahrain Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kuwait Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Oman Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Qatar Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- United Arab Emirates (UAE) Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- GCC Color Cosmetics Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- LVMH Moët Hennessy Louis Vuitton SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- L'Oréal Groupe

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cosnova GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coty Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Estée Lauder Cos Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kiko SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kamal Osman Jamjoom Group LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chanel SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Clarins SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Revlon Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shiseido Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Natura & Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LVMH Moët Hennessy Louis Vuitton SA

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now