GCC Cash Management Services Market Research Report: Forecast (2026-2032)

By Type (Hardware & Software Maintenance & Upgrades, Managed Services, 24/7 Incident & Helpdesk Management, ATM Monitoring, Site Identification & Preparation, Cash Management, Reco ... nciliation, Cash Optimization), By Deployment Location (Bank Branches, Retail Stores / Shopping Malls, Airports & Transportation Hubs, Petrol Stations, Hotels & Entertainment Venues), By Industry Vertical (Banking & Financial Services, Retail, Healthcare, Government, Transportation & Logistics), By End-User (Banks, Independent ATM Deployers), and others Read more

- FinTech

- Mar 2026

- Pages 250

- Report Format: PDF, Excel, PPT

GCC Cash Management Services Market

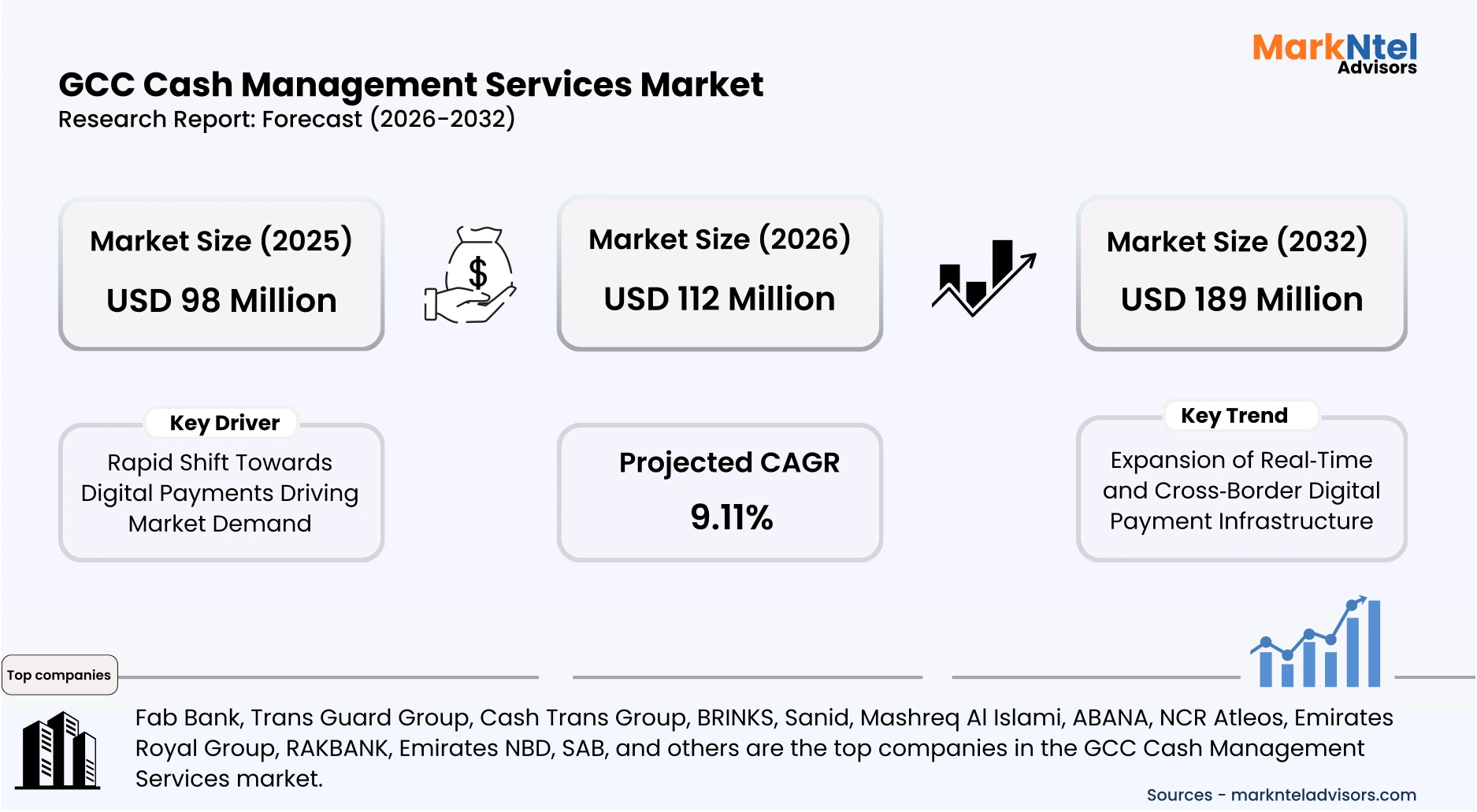

Projected 9.11% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 112 Million

Market Size (2032)

USD 189 Million

Base Year

2025

Projected CAGR

9.11%

Leading Segments

By Type: Cash Management

GCC Cash Management Services Market Report Key Takeaways:

- The GCC Cash Management Services market size was valued at USD 98 million in 2025 and is projected to grow from USD 112 million in 2026 to USD 189 million by 2032, exhibiting a CAGR of 9.11% during the forecast period.

- UAE is the leading country with a significant share of 45% in 2026.

- By end user, the banks represented a significant share of about 60% in the GCC Cash Management Services market in 2026.

- By type, the cash management segment seized a significant share of about 35% in the GCC Cash Management Services market in 2026.

- Leading cash management services companies in the GCC are Fab Bank, Trans Guard Group, Cash Trans Group, BRINKS, Sanid, Mashreq Al Islami, ABANA, NCR Atleos, Emirates Royal Group, RAKBANK, Emirates NBD, SAB, and Others.

Market Insights & Analysis: GCC Cash Management Services Market (2026-32):

The GCC Cash Management Services Market size was valued at USD 98 million in 2025 and is projected to grow from USD 112 million in 2026 to USD 189 million by 2032, exhibiting a CAGR of 9.11% during the forecast period. i.e., 2026-32.

The GCC cash management services market has expanded steadily alongside structural economic diversification and rapid financial sector transformation, reflecting broad regional priorities for resilient financial ecosystems. According to the World Bank’s Gulf Economic Update for late 2025, non‑hydrocarbon GDP drivers such as financial services and logistics are showing sustained expansion, with the UAE’s economy forecast to grow by approximately 4.8 % and Saudi Arabia by 3.8 % in 2025, underscoring a supportive macroeconomic backdrop that lifts ancillary services, including cash handling and treasury operations.

Rising demand from institutional and enterprise clients, particularly across commercial and industrial end users, has strengthened markets for sophisticated cash logistics as businesses streamline working capital and optimize treasury functions. The maturation of cross‑border payment corridors in the GCC is enhancing multinational liquidity management, enabling faster same‑day settlements that narrow operational frictions for regional corporations and financial service providers.

Regulatory frameworks are also driving the modernization of cash infrastructure. The UAE and Saudi central banks have implemented digital payment, and interoperability mandates that support both digital and physical cash circulation controls, while Kuwait’s recent prohibition of cash transactions for precious metal purchases has incentivized electronic transaction ecosystems. These measures align with broader policy objectives to improve traceability and financial integrity in commerce.

Technological transformation within the region’s banking sector has accelerated service delivery in cash operations. Across the GCC, financial institutions are adopting open banking platforms that promote API‑based data sharing and embedded cash management tools, enabling corporate clients to access real‑time liquidity insights and automated reconciliation. Dubai and Bahrain, for instance, have pioneered open data frameworks that enhance integration between traditional banks and fintech partners, increasing efficiency and reducing manual processing in treasury services.

GCC Cash Management Services Market Scope:

| Category | Segments |

|---|---|

| By Type | (Hardware & Software Maintenance & Upgrades, Managed Services, 24/7 Incident & Helpdesk Management, ATM Monitoring, Site Identification & Preparation, Cash Management, Reconciliation, Cash Optimization), |

| By Deployment Location | (Bank Branches, Retail Stores / Shopping Malls, Airports & Transportation Hubs, Petrol Stations, Hotels & Entertainment Venues), |

| By Industry Vertical | (Banking & Financial Services, Retail, Healthcare, Government, Transportation & Logistics), |

| By End-User | (Banks, Independent ATM Deployers), |

GCC Cash Management Services Market Driver:

Rapid Shift Towards Digital Payments Driving Market Demand

The most influential driver augmenting the GCC cash management services market is the accelerated adoption of digital payment systems by consumers, businesses, and financial institutions across member states. This phenomenon has emerged as a structural force rather than a cyclical trend, anchored by regulatory mandates and deep shifts in transaction behavior. Over recent years, strong national cadres of initiatives have embedded digital payments into core financial and commercial activity, reflecting intentional public policy to innovate payment rails. Saudi Arabia’s central bank has licensed and integrated global digital wallets such as Google Pay and Alipay+ by 2026, expanding consumer options and reducing friction in cash transactions .

Meanwhile, the UAE’s launch of platforms and digital tools such as SIB Pay with QR and smartphone tap‑to‑pay capabilities exemplifies how banking sector modernization directly alters transactional behavior, shifting volumes toward electronic methods. These regulatory actions reduce traditional cash use, expand digital payment bandwidth, and increase demand for complex liquidity and treasury services that underpin cash management ecosystems.

Critically, this trend materially expands market volume rather than merely influencing price levels or adoption spikes because it reshapes the underlying transactional base across all large end‑use segments, commerce, retail, remittances, and corporate finance. The GCC’s total digital payment value was projected to surpass USD 227 billion by 2025, indicating that electronic transactions are now a dominant force in economic life, and require integrated back ‑office cash flow and liquidity solutions to balance digital inflows with physical cash requirements in banking operations.

This structural shift creates enduring demand for advanced cash management services to support complex settlement cycles, reconciliation, and treasury operations. As digital channels proliferate, the role of cash services becomes more sophisticated, not obsolete, entrenching demand for hybrid liquidity tools that manage both digital and residual physical cash flows integral to the GCC’s expanding financial landscape.

GCC Cash Management Services Market Trend:

Expansion of Real‑Time and Cross‑Border Digital Payment Infrastructure

The most structurally significant trend reshaping the GCC cash management services market is the rapid expansion of real‑time and interoperable digital payment infrastructure, which has emerged from coordinated regulatory reforms and technology deployments across the region. Countries, including the UAE and Saudi Arabia, have prioritized instantaneous settlement capabilities.

For example, Saudi Arabia’s SARIE real‑time payments system processed substantially more transfers in 2024, contributing to faster settlement cycles that directly support treasury and liquidity services. This acceleration reflects intentional policy decisions to modernize core financial rails, not short‑term adoption volatility.

These developments are driving structural change across the entire market value chain by redefining how funds are moved, reconciled, and managed. For businesses, instant payment capabilities reduce working‑capital tied up in delayed settlements and enable suppliers and institutional clients to optimize cash conversion cycles.

For financial service providers, integrated digital rails facilitate API‑based liquidity management tools and more efficient reconciliation practices, reducing dependency on manual processing in back‑office cash operations.

Central banks are synchronizing open‑finance and token‑service regulations to streamline wallet provisioning and data portability, consolidating ecosystem connectivity and further embedding real‑time infrastructure into operational norms. For instance, Pay10 became the first fintech to go live under the CBUAE’s Open Finance framework in April 2025, receiving regulatory authorization to provide payment initiation services, including real‑time bank account connectivity. This production launch is a clear example of the framework moving from policy to measurable use, supporting interoperability and next‑generation payments.

This trend is expected to endure and transform long‑term market evolution because regulatory mandates and infrastructure investments create permanent operational standards, not transitory behaviors.

Vision‑driven public strategies, such as Saudi digital economy initiatives, anchor instant settlement as a baseline requirement for financial transactions across retail, corporate, and cross‑border use cases. As real‑time rails converge with regional payment interoperability and API‑driven platforms, cash management functions increasingly rely on these foundational systems to deliver liquidity optimization, risk management, and automated reconciliation at scale, ensuring the trend’s persistence and structural impact.

GCC Cash Management Services Market Opportunity:

Entry of FinTech via Open Finance and Digital Payment Infrastructure

The GCC market presents a significant opportunity for new entrants due to the rapid expansion of open finance frameworks and regulatory support for fintech innovation. Saudi Arabia, UAE, Bahrain, and Oman have introduced standardized API-based data access mandates and regulatory sandboxes that allow third-party providers to offer financial services. This structural shift lowers entry barriers for startups, enabling them to compete alongside traditional banks without the need for extensive legacy infrastructure.

Technological and infrastructural investments further reinforce this opportunity. The UAE Central Bank’s Financial Infrastructure Transformation (FIT) Programme provides real-time payment rails, eKYC standardization, and open banking protocols. Startups and emerging players can leverage these systems to provide automated treasury solutions, hybrid cash-digital management tools, and payment aggregation services, translating regulatory facilitation directly into measurable market demand.

Rising consumer and corporate adoption of digital payments reinforces the scalability potential for new entrants. In the UAE, the government targets 90 % cashless transactions by 2026, while fintech events such as Money20/20 Middle East in Riyadh gathered over 38,000 participants and 150 startups in 2025. These factors combine to create a structurally favorable market that prioritizes agility, innovation, and niche solutions, offering smaller players competitive differentiation and long-term growth potential.

GCC Cash Management Services Market Challenge:

Escalating Cybersecurity Threats and Data Vulnerabilities

A critical structural challenge for GCC cash management services is the rising frequency and sophistication of cyberattacks targeting financial and treasury operations. With digital payment rails, real-time settlement systems, and integrated cash management platforms, sensitive financial data is increasingly exposed. In 2025, the UAE reported a 45 % increase in attempted cyber intrusions against banking and payment infrastructure compared to 2024, demonstrating that escalating threats are not short-term but systemic in nature.

The challenge impacts operational efficiency and trust across end-user segments. Banks and corporate treasury departments must implement advanced threat detection, continuous monitoring, and secure data protocols, incurring high additional costs. A June 2025 Khaleej Times article reports that the UAE’s banking and financial sector is facing increasingly sophisticated cyberattacks, including AI‑driven spear‑phishing and “triple extortion” tactics, highlighting that the risk landscape is becoming more advanced and targeted, including real-time monitoring of critical payment systems and annual penetration testing, creating operational overhead that slows system integration and innovation for smaller or new market entrants.

These cybersecurity threats materially restrict market growth by affecting adoption and investor confidence. Corporations may delay implementing advanced cash management solutions due to perceived risk, and emerging fintechs may face barriers in acquiring clients or integrating with existing bank systems. The requirement for ongoing cybersecurity investments reduces available capital for expansion, training, or service differentiation, ultimately constraining the scalability and overall evolution of the GCC cash management services market. For instance, Coverage from GISEC Global 2025 underscores that banks and financial services in the Middle East are repeatedly targeted by cyber incidents, with ransomware attacks up by 32 % in the UAE in 2024, emphasizing persistent risk for core financial systems.

GCC Cash Management Services Market (2026-32) Segmentation Analysis:

The GCC Cash Management Services Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on End-User:

- Banks

- Independent ATM Deployers

Banks dominate the GCC cash management services market with a market share of 60% due to their extensive branch networks and high transaction volumes. Regulatory mandates from central banks encourage the adoption of sophisticated cash management solutions, ensuring operational efficiency and compliance. Investment in digital and automated systems has enhanced banks’ ability to handle large-scale cash flows while reducing manual errors. These factors collectively reinforce banks’ position as the primary end-user segment.

Rising customer demand for seamless transaction services and faster settlement cycles drives banks to prioritize advanced cash handling and optimization solutions. Strategic partnerships with cash management solution providers further amplify banks’ operational capabilities. Government incentives supporting digitalization in the financial sector also boost adoption rates.

For instance, large UAE banks like Emirates NBD maintain extensive branch and ATM networks across the Emirates, with over 200 branches and 900 ATMs/Cash Deposit Machines offering a wide range of cash management, payments, liquidity, and reconciliation services to both retail and corporate clients. This broad physical infrastructure supports frequent and high‑volume cash transactions, which in turn drives demand for professional cash handling and optimized cash flow solutions. Consequently, banks maintain a structural advantage over independent ATM deployers and other segments in the region.

The segment’s dominance is further strengthened by consistent capital allocation toward technology-driven enhancements. Banks’ ability to integrate predictive analytics and reconciliation systems enhances cash visibility across branches. End-user demand for security, transparency, and efficiency ensures sustained leadership. With favorable regulatory support, high investment flows, and continuous innovation, banks are expected to remain the foremost beneficiaries of GCC cash management services.

Based on Type:

- Hardware & Software Maintenance & Upgrades

- Managed Services

- 24/7 Incident & Helpdesk Management

- ATM Monitoring

- Site Identification & Preparation

- Cash Management

- Reconciliation

- Cash Optimization

The cash management segment leads with a market share of 35% due to its critical role in optimizing liquidity and controlling operational costs for financial institutions. Rising transactional volumes across retail, hospitality, and transport sectors drive demand for end-to-end cash handling solutions. Banks and corporates increasingly rely on sophis ticated cash management systems to minimize idle cash and improve forecasting accuracy.

Policy initiatives promoting secure and transparent cash circulation have incentivized investments in automation and smart vault solutions. The segment benefits from high adoption of technologies like real-time cash monitoring, AI-driven demand prediction, and automated reconciliation. End-user emphasis on operational efficiency and risk mitigation further strengthens segment growth.

Significant capital flows into integrated cash management solutions underscore their strategic importance in the GCC market. Strong adoption by banks, supported by regulatory encouragement and technology upgrades, ensures the segment’s continued dominance. As demand for secure, efficient, and fully automated cash operations rises, the Cash Management segment is projected to maintain its leading market position throughout 2026–32.

GCC Cash Management Services Market (2026-32) Regional Analysis:

The UAE continues to grow strongly, with a market share of 45%, with projected growth of 4.4% in 2025 and 5.4% in 2026, outpacing many regional peers, reflecting diversified growth beyond oil into services, trade, and tech sectors. This growth enhances demand for financial infrastructure and services, including payments and cash management capabilities. The UAE’s non‑oil GDP expansion, driven by sectors like tourism, logistics, financial services, and communications, amplifies transaction volumes and business activity.

The UAE has implemented forward‑looking financial policy reforms that directly enable market leadership. These measures improve regulatory clarity, reduce barriers for fintech and banking innovations, and elevate market competitiveness. The adoption of Federal Decree‑Law No. 6 of 2025 further modernizes financial regulation by embedding digital currency (Digital Dirham) as legal tender, expanding licensed fintech operations, and reinforcing compliance and risk management.

The UAE’s advanced infrastructure and global business environment attract a high concentration of major financial institutions, fintech firms, and multinational corporations. The integrated digital financial ecosystem supported by sandboxes, API‑driven open finance, and unified licensing reforms encourages rapid adoption of digital banking, AI‑driven analytics , and innovative payment solutions. Rising digital payment activity (e.g., cashless strategies aiming for high adoption by 2026) reflects both consumer and institutional demand for advanced financial services.

Gain a Competitive Edge with Our GCC Cash Management Services Market Report:

- The GCC Cash Management Services Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The GCC Cash Management Services Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Cash Management Services Market Policies, Regulations, and Product Standards

- GCC Cash Management Services Market Trends & Developments

- GCC Cash Management Services Market Dynamics

- Growth Factors

- Challenges

- GCC Cash Management Services Market Hotspot & Opportunities

- GCC Cash Management Services Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Hardware & Software Maintenance & Upgrades

- Managed Services

- 24/7 Incident & Helpdesk Management

- ATM Monitoring

- Site Identification & Preparation

- Cash Management

- Reconciliation

- Cash Optimization

- By Deployment Location- Market Size & Forecast 2022-2032, USD Million

- Bank Branches

- Retail Stores / Shopping Malls

- Airports & Transportation Hubs

- Petrol Stations

- Hotels & Entertainment Venues

- By Industry Vertical- Market Size & Forecast 2022-2032, USD Million

- Banking & Financial Services

- Retail

- Healthcare

- Government

- Transportation & Logistics

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Banks

- Independent ATM Deployers

- By Country

- UAE

- Saudi Arabia

- Qatar

- Kuwait

- Bahrain

- Oman

- Rest of GCC

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Cash Management Services Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Deployment Location- Market Size & Forecast 2022-2032, USD Million

- By Industry Vertical- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Cash Management Services Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Deployment Location- Market Size & Forecast 2022-2032, USD Million

- By Industry Vertical- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Qatar Cash Management Services Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Deployment Location- Market Size & Forecast 2022-2032, USD Million

- By Industry Vertical- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kuwait Cash Management Services Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Deployment Location- Market Size & Forecast 2022-2032, USD Million

- By Industry Vertical- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Bahrain Cash Management Services Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Deployment Location- Market Size & Forecast 2022-2032, USD Million

- By Industry Vertical- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Oman Cash Management Services Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Deployment Location- Market Size & Forecast 2022-2032, USD Million

- By Industry Vertical- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- GCC Cash Management Services Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Fab Bank

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Trans Guard Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cash Trans Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BRINKS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanid

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mashreq Al Islami

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ABANA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NCR Atleos

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Emirates Royal Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- RAKBANK

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Emirates NBD

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SAB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fab Bank

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now