Europe Pet Food Market Research Report: Growth Drivers & Forecast (2026-2032)

By Product Type (Dry Pet Food, Wet Pet Food, Semi-moist Pet Food, Snacks & Treats), By Pet Type (Dog, Cat, Bird), By Form (Pellets, Crumbles, Mesh, Flakes), By Specialty (Prescript ... ion or Therapeutic Diets, Weight Management Diets, Hypoallergenic Diets), By Ingredients (Animal-based, Plant-based), By Distribution Channel (Offline, Online), and others Read more

- Food & Beverages

- Mar 2026

- Pages 220

- Report Format: PDF, Excel, PPT

Europe Pet Food Market

Projected 4.32% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 45.87 Billion

Market Size (2032)

USD 59.11 Billion

Base Year

2025

Projected CAGR

4.32%

Leading Segments

By Pet Type: Dog

Europe Pet Food Market Report Key Takeaways:

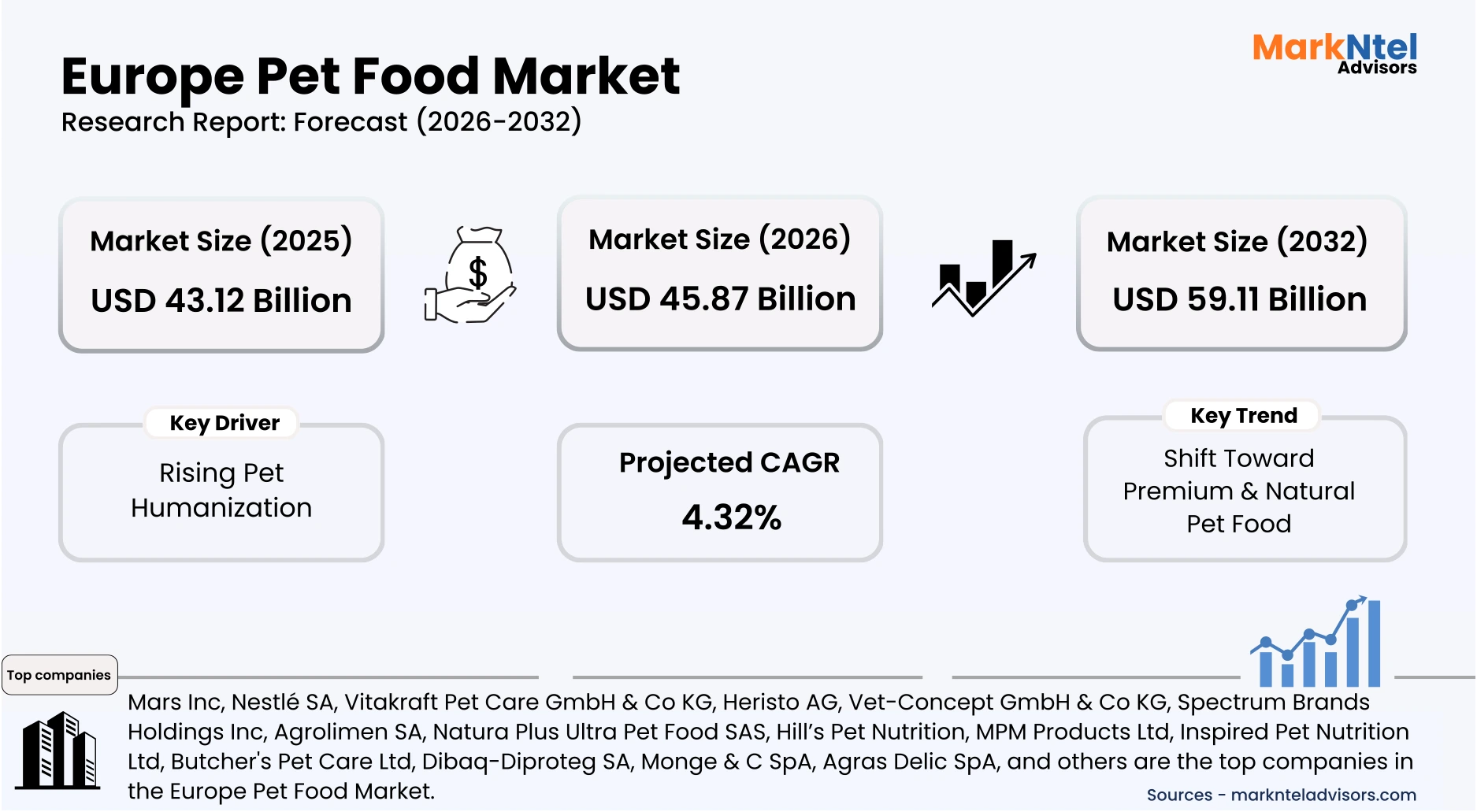

- The Europe Pet Food Market size was valued at around USD 43.12 billion in 2025 and is projected grow from USD 45.87 billion in 2026 to USD 59.11 billion by 2032, exhibiting a CAGR of 4.32% during the forecast period.

- Germany holds the largest market share of about 24.7% in the Europe Pet Food Market in 2026.

- By Product Type, the Dry Pet Food segment represented a significant share of about 56% in the Europe Pet Food Market in 2026.

- By Pet Type, the Dog segment represented a significant share of about 43% in the Europe Pet Food Market in 2026.

- Leading companies in the market are Mars Inc, Nestlé SA, Vitakraft Pet Care GmbH & Co KG, Heristo AG, Vet-Concept GmbH & Co KG, Spectrum Brands Holdings Inc, Agrolimen SA, Natura Plus Ultra Pet Food SAS, Hill’s Pet Nutrition, MPM Products Ltd, Inspired Pet Nutrition Ltd, Butcher's Pet Care Ltd, Dibaq-Diproteg SA, Monge & C SpA, Agras Delic SpA, and Others.

Market Insights & Analysis: Europe Pet Food Market (2026-32):

The Europe Pet Food Market size was valued at around USD 43.12 billion in 2025 and is projected grow from USD 45.87 billion in 2026 to USD 59.11 billion by 2032, exhibiting a CAGR of 4.32% during the forecast period, i.e., 2026-32.

Europe’s pet food market has demonstrated steady and resilient expansion, supported by high pet ownership levels and consistent consumer spending across major economies such as Germany, France, and the United Kingdom. According to the European Pet Food Industry Federation (FEDIAF), the market was valued at approximately USD 33.7 billion in 2023, as reported in its 2025 Facts & Figures publication . Historical growth has been driven by the increasing humanization of pets, alongside rising disposable incomes and urban living patterns. These factors have supported sustained demand for premium, functional, and specialized pet nutrition products across the region.

Current market conditions are strongly influenced by residential end users, with FEDIAF reporting that over 90 million European households owned pets in 2023, ensuring stable consumption volumes . Commercial segments, including veterinary clinics, pet specialty retailers, and animal care facilities, are also expanding and contributing to higher-value product demand, particularly for therapeutic and condition-specific diets. The European Commission’s Regulation (EC) No 767/2009 on feed marketing and labeling ensures strict compliance with product safety and transparency. This regulatory framework enhances consumer trust while enabling manufacturers to innovate within clearly defined standards.

Sustainability and regulatory initiatives are increasingly shaping production practices and long-term market positioning. The European Union’s Farm to Fork Strategy, a core component of the European Green Deal, promotes sustainable sourcing, reduced environmental impact, and improved traceability across food systems, including pet food. In line with these objectives, companies such as Nestlé Purina announced expansions of regenerative agriculture initiatives in 2025 to strengthen sustainable ingredient sourcing . Industry players are also investing in recyclable packaging and energy-efficient manufacturing technologies, aligning with EU climate targets and evolving consumer expectations for environmentally responsible products.

Looking ahead, structural demographic trends and evolving retail infrastructure are expected to sustain market growth across Europe. Eurostat’s 2025 housing data indicates a continued rise in single-person households and smaller living units, particularly in urban areas, reflecting changing lifestyle patterns. These trends are associated with increased pet ownership as individuals seek companionship, supporting consistent spending on premium pet care products. Additionally, the expansion of e-commerce platforms and subscription-based delivery models is improving accessibility and repeat purchasing behavior. Combined with strong regulatory oversight and ongoing product innovation, these factors position the market for stable long-term expansion.

Europe Pet Food Market Recent Developments:

- 2025 : Hill’s Pet Nutrition strengthened its Prescription Diet portfolio across Europe, focusing on scientifically formulated products addressing pet health conditions such as obesity and kidney disease. The expansion reflects growing veterinary adoption of therapeutic nutrition solutions.

- 2026 : Vafo Group expanded production capabilities across Europe, enhancing output for premium and super-premium pet food brands. The company continues to invest in regional facilities to meet rising demand for high-quality and natural pet nutrition products.

Europe Pet Food Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Dry Pet Food, Wet Pet Food, Semi-moist Pet Food, Snacks & Treats), |

| By Pet Type | (Dog, Cat, Bird), |

| By Form | (Pellets, Crumbles, Mesh, Flakes), |

| By Specialty | (Prescription or Therapeutic Diets, Weight Management Diets, Hypoallergenic Diets), |

| By Ingredients | (Animal-based, Plant-based), |

| By Distribution Channel | (Offline, Online), |

Europe Pet Food Market Driver:

Rising Pet Humanization

Pet humanization in Europe has strengthened due to measurable demographic and socioeconomic changes, particularly the rise in single-person households and aging populations. According to Eurostat, single-adult households account for a significant and growing share across EU countries. This shift has increased emotional reliance on companion animals, transforming pets into integral household members and structurally elevating spending priorities toward their health, nutrition, and well-being.

This behavioral transformation is directly translating into higher pet-related expenditure and consumption volumes across residential end users. According to Reuters (2026), pet-related spending in the United Kingdom reached approximately USD 15.5 billion in 2023, increasing nearly fourfold since 2005. This sustained rise reflects not only higher product value but also increased purchase frequency, diversified product usage, and greater adoption of specialized pet food categories across European households.

Unlike short-term premiumization trends, pet humanization drives measurable volume expansion through increased feeding intensity and lifecycle-based nutrition. Pet owners are purchasing multiple product types, including daily meals, treats, and condition-specific diets, resulting in higher per-pet consumption. Regulatory reinforcement from the European Commission, including updated animal welfare and labeling frameworks, further strengthens consumer confidence, ensuring that this demand driver remains structurally embedded and continues to expand the Europe pet food market over the long term.

Europe Pet Food Market Trend:

Shift Toward Premium & Natural Pet Food

The shift toward premium and natural pet food in Europe has accelerated due to evolving consumer expectations around pet health, ingredient transparency, and sustainability. According to FoodNavigator (2026), demand growth is increasingly driven by preference for clean-label, minimally processed, and high-quality formulations. This reflects broader dietary patterns across Europe, where consumers prioritize traceability, ethical sourcing, and nutritional value in both human and pet food consumption.

This trend is structurally transforming the value chain through innovation in ingredients, product development, and sourcing strategies. For instance, Tribal Pet Foods introduced grain-free cat food formulations containing 70% fresh meat and no artificial additives, reflecting strong demand for natural nutrition. Additionally, the emergence of plant-based Omega-3 ingredients, insect-protein pet food, and cultivated meat-based products highlights a shift toward sustainable and functional alternatives . The European Commission has further reinforced this shift through Product Environmental Footprint frameworks introduced in 2025.

The persistence of this trend is supported by regulatory alignment, sustained consumer willingness to spend, and continued industry investment in premium product lines. Companies are increasingly adopting novel ingredients and localized production to meet evolving expectations for quality and sustainability. Veterinary endorsement of functional and specialized diets further strengthens consumer trust in higher-value offerings. As these structural changes continue, premium and natural pet food will remain a defining trend shaping long-term market evolution in Europe.

Europe Pet Food Market Opportunity:

Expansion of the Veterinary and Prescription Diet Segment

The expansion of veterinary and prescription pet diets in Europe presents a structural opportunity driven by rising clinical integration of nutrition into pet healthcare. The increasing prevalence of chronic conditions such as renal disorders, obesity, and allergies is accelerating demand for condition-specific diets. Regulatory frameworks, including EU Regulation 2019/4 on medicated feed, are enabling innovation in therapeutic nutrition while ensuring safety and compliance across the region.

This opportunity is translating into tangible market demand through product innovation and clinical adoption. For instance, Wynwood Dog Food launched fresh prescription diets targeting renal health, allergies, and weight management, reflecting growing demand for functional, condition-specific nutrition . Similarly, Virbac introduced the first medicated cat food in Europe, combining therapeutic diets with veterinary drugs, marking the emergence of a new integrated treatment category within pet nutrition.

The segment is particularly advantageous for new entrants due to its specialized, innovation-driven nature and relatively lower commoditization. Emerging players can differentiate through fresh, clinically positioned formulations and partnerships with veterinary professionals. As therapeutic nutrition becomes embedded in routine pet care, this segment offers scalable, high-margin opportunities for smaller companies to establish a strong foothold in the evolving Europe pet food market.

Europe Pet Food Market Challenge:

Rising Raw Material Prices and Production Costs

Rising raw material prices and production costs have become a structural constraint in the Europe pet food market due to persistent inflation, energy price volatility, and supply disruptions. According to the European Central Bank (2025), food prices in the Eurozone have increased by approximately 34% since 2019, driven by higher commodity and energy costs. Additionally, Reuters (2026) reports that European industries continue to face significant cost pressures from raw materials and energy inputs.

These cost pressures are measurably impacting manufacturers by compressing margins and forcing price increases across the value chain. For instance, chemical producer BASF announced price hikes of up to 30% in response to rising input and energy costs, reflecting broader industrial trends affecting downstream sectors such as pet food. S maller manufacturers are particularly vulnerable due to limited procurement leverage, resulting in reduced operational flexibility and increased reliance on passing costs to consumers.

This challenge materially restricts market expansion by reducing affordability and slowing the adoption of premium and specialized pet food products. Higher retail prices limit demand in price-sensitive segments, particularly in emerging European markets. Additionally, elevated production and compliance costs increase capital requirements, discouraging new entrants and investment. As these pressures persist, rising input costs continue to constrain scalability, profitability, and overall market growth across the Europe pet food industry.

Europe Pet Food Market (2026-32) Segmentation Analysis:

The Europe Pet Food market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Dry Pet Food

- Wet Pet Food

- Semi-moist Pet Food

- Snacks & Treats

The dry pet food segment dominates the Europe Pet Food Market, accounting for approximately 56% of total demand, primarily because it aligns with the region’s large-scale, cost-efficient, and convenience-driven pet feeding patterns. Europe’s pet population exceeds 300 million animals across nearly 139 million households, reflecting high-frequency, everyday feeding requirements that favor bulk and shelf-stable formats. This scale of consumption naturally supports dry pet food, as it allows pet owners to purchase in larger quantities at lower per-unit costs while eliminating the need for refrigeration, making it particularly suitable for urban and dual-income households.

Production efficiency and supply chain advantages further strengthen this dominance. Dry pet food is manufactured using standardized extrusion technologies, enabling consistent, high-volume output with controlled nutritional composition. Europe’s well-established agri-food and feed processing infrastructure ensures steady access to essential raw materials such as cereals, meat derivatives, and plant-based proteins, allowing manufacturers to maintain competitive pricing and reliable distribution across the region. In comparison to wet and fresh alternatives, dry food offers longer shelf life and lower transportation and storage costs, which is especially important amid rising input and logistics expenses across Europe.

Additionally, dry pet food benefits from strong alignment with veterinary-backed nutrition and functional health benefits. Many kibble-based formulations are designed to support dental health, weight management, and digestive balance, which resonates with increasingly health-conscious pet owners. This is further supported by recent industry developments, such as the 2025 launch of a veterinarian-endorsed pet food range by DIA in Spain, where dry formulations formed a core component of balanced, science-based diets . As a result, the combination of affordability, scalability, long shelf life, and growing clinical validation continues to position dry pet food as the leading product type in the European market.

Based on Pet Type:

- Dog

- Cat

- Bird

- Others (Fish, Small Mammals, Reptiles, etc.)

The dog segment dominates the Europe Pet Food Market, accounting for the largest share, 43% in both volume and value, primarily because dogs require higher daily food intake and generate greater per-pet expenditure compared to other companion animals. Across Europe, dog ownership remains deeply embedded in household structures, with millions of households relying on consistent, high-volume feeding routines. This results in significantly higher consumption levels than cats and other pets, as dogs typically consume larger portion sizes and more calorie-dense diets, directly driving overall market volume.

Spending behavior further reinforces this dominance. Dog owners in Europe exhibit a stronger willingness to invest in premium and specialized nutrition, including breed-specific diets, functional health formulas, and treats. This has led to a broader and more diversified product ecosystem for dogs, spanning dry food, wet food, snacks, and therapeutic nutrition, which collectively contributes to higher market value generation. In contrast, while cat ownership is widespread, feeding patterns are relatively lower in volume and less diversified in terms of product variety.

Additionally, ongoing premiumization and pet humanization trends are more pronounced in the dog segment, with owners increasingly seeking high-protein, natural, and veterinarian-recommended formulations. This is supported by continuous product innovation and retail expansion across Europe, where manufacturers prioritize dog-focused portfolios to capture higher margins and repeat purchase cycles. As a result, the combination of higher consumption intensity, elevated spending patterns, and stronger premiumization trends continues to position the dog segment as the leading pet type in the European pet food market.

Europe Pet Food Market (2026-32): Regional Projection

Germany dominates the Europe Pet Food Market, accounting for approximately 24.7% of total regional demand, primarily because it represents the largest and most structurally established pet ownership base in Europe. As of 2023, approximately 45% of German households own at least one pet, with 14% owning two or more, resulting in a total pet population of around 34.3 million animals. This high penetration of pet ownership creates a broad and stable consumer base that drives consistent, high-volume demand for commercial pet food products across the country.

The dominance is further reinforced by the concentration of high-consumption pet types. Cats and dogs account for the majority of pets in German households, with 25% of households owning cats and 21% owning dogs . These two categories are the primary drivers of pet food demand due to their reliance on nutritionally balanced, commercially prepared diets and higher feeding frequency compared to other pet types. While other pets, such as small mammals, birds, fish, and reptiles collectively account for 17% of pets, their overall food consumption levels and spending contribution remain significantly lower, reinforcing the central role of cats and dogs in market expansion.

Additionally, Germany benefits from strong consumer spending capacity and a mature pet care ecosystem, which supports widespread adoption of packaged and premium pet food products. High pet ownership density, combined with a preference for commercial nutrition over home feeding, ensures sustained repeat purchases and higher per-household expenditure. This demand is further supported by well-developed retail and distribution networks, enabling extensive product availability across the country. As a result, the combination of large-scale pet ownership, dominance of high-consumption pet types, and consistent purchasing behavior firmly positions Germany as the leading country in the European pet food market.

Gain a Competitive Edge with Our Europe Pet Food Market Report:

- Europe Pet Food Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Europe Pet Food Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Pet Food Market Policies, Regulations, and Product Standards

- Europe Pet Food Market Trends & Developments

- Europe Pet Food Market Dynamics

- Growth Factors

- Challenges

- Europe Pet Food Market Hotspot & Opportunities

- Europe Pet Food Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Dry Pet Food

- Wet Pet Food

- Semi-moist Pet Food

- Snacks & Treats

- By Pet Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Dog

- Cat

- Bird

- Others (Fish, Small Mammals, Reptiles, etc.)

- By Form- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Pellets

- Crumbles

- Mesh

- Flakes

- By Specialty- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Prescription or Therapeutic Diets

- Weight Management Diets

- Hypoallergenic Diets

- By Ingredients- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Animal-based

- Plant-based

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Offline

- Hypermarkets/Supermarkets

- Retail Stores

- Specialty Pet Stores

- Online

- Offline

- By Country

- Germany

- The UK

- Italy

- France

- Spain

- Benelux

- Sweden

- Rest of Europe

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Germany Pet Food Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Pet Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Form- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Specialty- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Ingredients- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- The UK Pet Food Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Pet Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Form- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Specialty- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Ingredients- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Italy Pet Food Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Pet Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Form- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Specialty- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Ingredients- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- France Pet Food Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Pet Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Form- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Specialty- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Ingredients- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Spain Pet Food Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Pet Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Form- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Specialty- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Ingredients- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Benelux Pet Food Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Pet Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Form- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Specialty- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Ingredients- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Sweden Pet Food Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Million Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Pet Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Form- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Specialty- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Ingredients- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Europe Pet Food Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Mars Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nestlé SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vitakraft Pet Care GmbH & Co. KG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Heristo AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vet-Concept GmbH & Co KG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Spectrum Brands Holdings Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Agrolimen SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Natura Plus Ultra Pet Food SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hill’s Pet Nutrition

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- MPM Products Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Inspired Pet Nutrition Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Butcher's Pet Care Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dibaq-Diproteg SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Monge & C SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Agras Delic SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mars Inc

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now