Egypt Logistics Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Service (Transportation Services, Warehousing & Distribution Services, Freight Forwarding Services, Inventory Management Services, Value-Added Logistics Services, Integration & ... Consulting Services), By Category (Conventional Logistics, E-Commerce Logistics), By Model Type (2PL (Second Party Logistics), 3PL (Third Party Logistics), 4PL (Fourth Party Logistics)), By Type (Forward Logistics, Reverse Logistics), By Operation (Domestic, International), By Mode of Transport (Roadways, Waterways, Airways, Railways), By End Use (Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others), and others Read more

- Automotive

- Mar 2026

- Pages 165

- Report Format: PDF, Excel, PPT

Egypt Logistics Market

Projected 3.73% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 19.37 Billion

Market Size (2032)

USD 24.13 Billion

Base Year

2025

Projected CAGR

3.73%

Leading Segments

By Mode of Transport: Roadways

Egypt Logistics Market Report Key Takeaways:

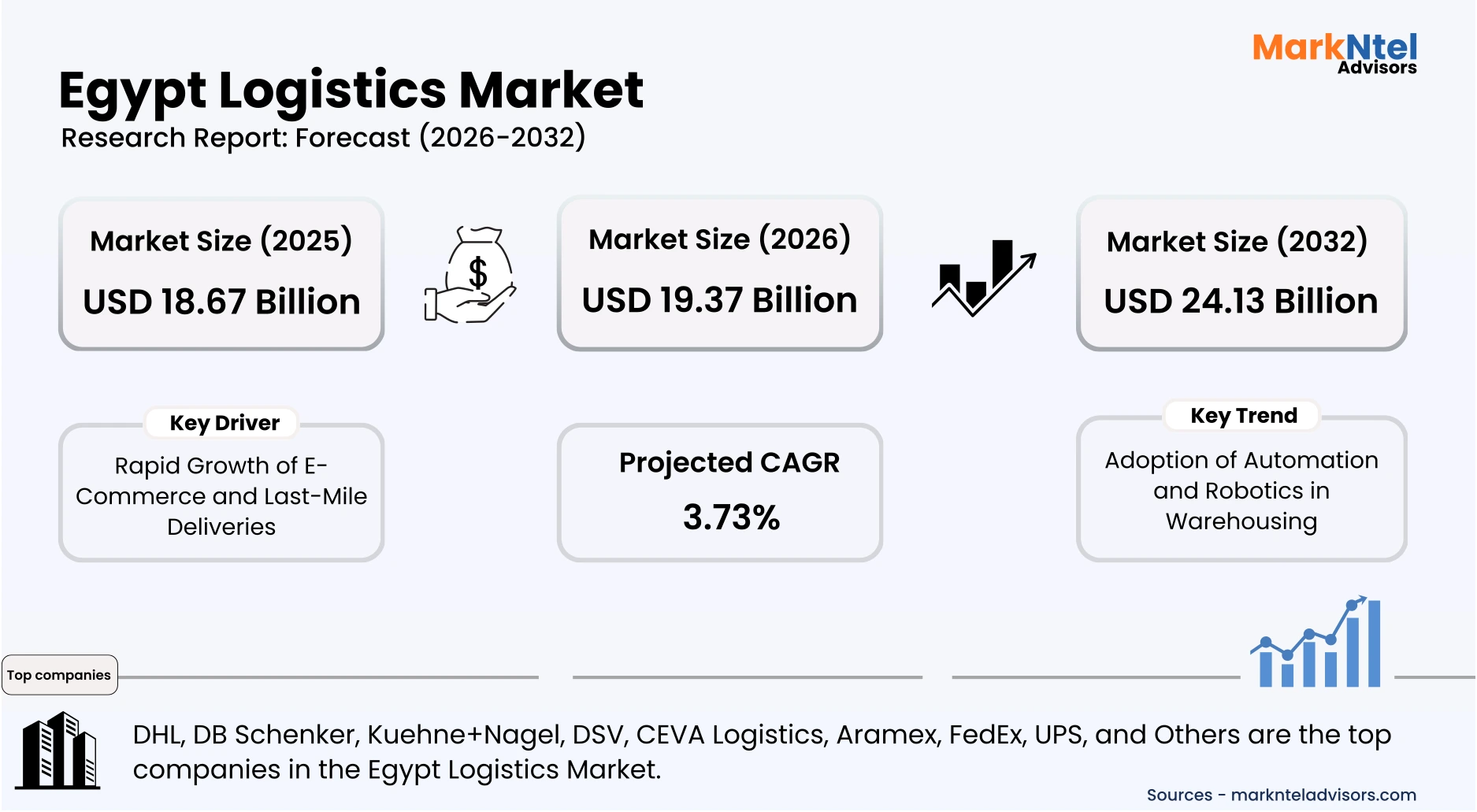

- The Egypt Logistics Market size was valued at around USD 18.67 billion in 2025 and is projected grow from USD 19.37 billion in 2026 to USD 24.13 billion by 2032, exhibiting a CAGR of 3.73% during the forecast period.

- The Greater Cairo region holds the largest market share of about 36% in the Egypt Logistics Market in 2026.

- By Model Type, the 3PL segment represented a significant share of about 45% in the Egypt Logistics Market in 2026.

- By Mode of Transport, the roadways segment presented a significant share of about 54% in the Egypt Logistics Market in 2026.

- Leading Logistics companies in the Egypt market are DHL, DB Schenker, Kuehne+Nagel, DSV, CEVA Logistics, Aramex, FedEx, UPS, and Others.

Market Insights & Analysis: Egypt Logistics Market (2026-32):

The Egypt Logistics Market size was valued at around USD 18.67 billion in 2025 and is projected grow from USD 19.37 billion in 2026 to USD 24.13 billion by 2032, exhibiting a CAGR of 3.73% during the forecast period, i.e., 2026-32.

Egypt’s logistics sector has expanded steadily over the past decade, supported by growing trade activity, infrastructure modernization, and a rapidly expanding consumer market. According to the Central Bank of Egypt (CBE), Egypt’s total foreign trade reached approximately USD 64.9 billion during the first half of fiscal year 2024/25, including USD 46.2 billion in imports and USD 18.7 billion in exports. This strong trade activity reflects substantial cargo flows requiring efficient transportation, warehousing, and freight forwarding services. As industrial production and consumer demand increase, logistics operators continue expanding distribution networks and service capacity.

Current market conditions remain favorable as Egypt advances large-scale infrastructure programs aimed at strengthening national transport connectivity. Government initiatives such as the National Roads Project and port modernization plans have expanded highway networks and improved access to key maritime gateways, including Alexandria, Damietta, and Ain Sokhna. These upgrades enhance cargo movement between ports, industrial zones, and inland distribution centers, reducing transit bottlenecks and improving supply-chain efficiency. Egypt’s National Narrative for Comprehensive Development also outlines plans to establish seven national logistics corridors and a network of 33 dry ports and logistics zones to connect production centers with maritime gateways and improve freight movement efficiency. At the same time, the Suez Canal Economic Zone (SCZone) continues to attract manufacturing and logistics investments that increase freight demand and distribution activity .

End-user industries play a central role in shaping logistics demand across the country. Egypt’s large consumer population, exceeding 110 million people according to national statistics, sustains strong retail and e-commerce distribution needs, particularly in densely populated regions such as Greater Cairo and the Nile Delta. Manufacturing sectors, including textiles, chemicals, food processing, and consumer goods, rely heavily on logistics providers for inbound raw materials and outbound finished products. Meanwhile, agricultural exports and pharmaceutical supply chains are increasing demand for specialized logistics services such as refrigerated transport and temperature-controlled storage.

Looking ahead, Egypt’s logistics market is expected to maintain positive momentum as infrastructure investment, digitalization, and industrial development continue to accelerate. Government programs supporting port expansion, railway upgrades, and logistics zones aim to strengthen the country’s role as a regional trade and distribution hub connecting Africa, Europe, and Asia. Private sector initiatives are also expanding fulfillment infrastructure, automated sorting facilities, and integrated supply-chain platforms to support growing e-commerce and manufacturing activity. Together, these economic, demographic, and policy-driven factors are expected to sustain logistics demand and reinforce Egypt’s long-term market growth trajectory.

Egypt Logistics Market Recent Developments:

- 2025 : The Suez Canal Automotive Terminal (SCAT), a JV between NYK, Africa Global Logistics, and Toyota Tsusho, began operations in East Port Said. The facility can initially handle 2,550 vehicles, with expansion capacity to 10,000, bolstering finished-vehicle import/export logistics.

- 2025 : Egypt entered cooperation pacts with Djibouti covering ports, logistics zones, and renewable energy to strengthen maritime transport and trade infrastructure links.

Egypt Logistics Market Scope:

| Category | Segments |

|---|---|

| By Service | (Transportation Services, Warehousing & Distribution Services, Freight Forwarding Services, Inventory Management Services, Value-Added Logistics Services, Integration & Consulting Services), |

| By Category | (Conventional Logistics, E-Commerce Logistics), |

| By Model Type | (2PL (Second Party Logistics), 3PL (Third Party Logistics), 4PL (Fourth Party Logistics)), |

| By Type | (Forward Logistics, Reverse Logistics), |

| By Operation | (Domestic, International), |

| By Mode of Transport | (Roadways, Waterways, Airways, Railways), |

| By End Use | (Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others), |

Egypt Logistics Market Driver:

Rapid Growth of E-Commerce and Last-Mile Deliveries

Egypt’s rapid expansion in e-commerce activity has emerged as a structural driver of logistics demand, supported by sustained digital connectivity growth. World Bank data indicate that internet usage in Egypt reached approximately 72.7% of the population in 2023, compared with nearly 54% in 2018, significantly enlarging the country’s digitally connected consumer base. As digital access expanded, online retail platforms and mobile commerce services gained wider adoption across urban populations. In 2025, Jumia inaugurated a 27,000-square-meter integrated warehouse in Cairo to strengthen storage and distribution capacity, particularly improving delivery reach to underserved regions such as Upper Egypt. This transformation has intensified demand for fulfillment centers, courier networks, and last-mile delivery infrastructure.

The demand impact is increasingly visible across Egypt’s largest consumer markets. Government digital transformation programs under the Digital Egypt initiative, expanded through 2025, have supported online payment systems and digital marketplace participation for small businesses. The Central Bank of Egypt has also promoted electronic payment adoption, increasing transaction frequency in online retail environments . As a result, logistics demand has grown particularly in Greater Cairo and Alexandria, where population density and retail activity generate high parcel volumes requiring rapid fulfillment and delivery.

Unlike cyclical retail expansion, e-commerce structurally increases logistics intensity because each online transaction generates multiple supply-chain movements. These include first-mile pickup from sellers, sorting and warehousing operations, and last-mile delivery to consumers, often followed by reverse logistics for returns. Egypt Post and courier operators have reported rising parcel handling volumes as online purchasing becomes more common. Consequently, the sustained rise of digital commerce is expanding shipment frequency and logistics throughput, directly increasing market size and operational demand across Egypt’s logistics sector.

Egypt Logistics Market Trend:

Adoption of Automation and Robotics in Warehousing

Automation and robotics are increasingly transforming warehousing operations as logistics providers respond to rising order volumes and efficiency pressures. The International Federation of Robotics reported continued global growth in industrial robot installations in logistics-related environments, particularly in automated storage, sorting, and packaging systems. In Egypt, expanding e-commerce fulfillment requirements and modern logistics parks have accelerated interest in technology-enabled warehouse operations. In 2026, Egyptian logistics company Bosta launched the Middle East’s largest automated parcel sorting machine capable of processing 11,000 parcels per hour and up to 250,000 parcels per day, supported by an investment of approximately USD 5 million. These developments reflect a structural shift toward a digitally integrated distribution infrastructure capable of managing high-order throughput.

The trend has emerged as logistics operators seek to reduce manual handling, improve inventory accuracy, and accelerate order processing cycles. Automated storage and retrieval systems, robotic picking technologies, and smart conveyor systems are being integrated into large fulfillment centers to optimize space utilization and operational productivity. Major logistics hubs and distribution facilities serving online retail platforms increasingly deploy digital warehouse management systems combined with automated equipment. This transformation is reshaping operational models by enabling faster order fulfillment and scalable logistics capacity.

Automation adoption is expected to persist as digital commerce and supply-chain complexity continue expanding across Egypt and the broader Middle East region. Automated warehouses enable higher throughput while reducing operational delays and labor-intensive processes, making them attractive for large distribution networks. As logistics infrastructure modernizes and companies invest in technology-driven supply-chain operations, robotics-based warehousing is becoming a core component of competitive logistics strategies. This structural transition will continue influencing long-term efficiency, service quality, and logistics network scalability.

Egypt Logistics Market Opportunity:

Expansion of Cold Chain and Pharma Logistics Services

Egypt’s healthcare expansion and pharmaceutical production growth are creating significant demand for temperature-controlled logistics infrastructure. According to the Egyptian Ministry of Health, the country has increased investments in vaccine storage, pharmaceutical distribution, and healthcare infrastructure to strengthen supply resilience following the COVID-19 pandemic. In 2025, DP World announced plans to build a USD 29 million cold storage facility in Egypt with capacity for around 25,000 pallets of refrigerated goods to strengthen temperature-controlled logistics infrastructure. Egypt also participates in regional vaccine manufacturing initiatives supported by international partners and public health agencies. These developments require reliable cold chain systems capable of maintaining strict temperature conditions during storage, transportation, and distribution.

Demand for pharmaceutical logistics services has intensified as Egypt strengthens its role as a regional healthcare and pharmaceutical hub. The government’s pharmaceutical sector development strategy, supported by regulatory authorities and international health organizations, aims to expand local drug production and improve medicine availability across domestic and regional markets. In 2025, Egypt began construction of a USD 220 million vaccine manufacturing complex in the Suez Canal Economic Zone to expand vaccine production and exports across Africa. As pharmaceutical exports and vaccine distribution networks expand, logistics providers must deploy refrigerated warehouses, specialized transport fleets, and real-time temperature monitoring systems. These requirements are generating substantial demand for advanced cold chain infrastructure.

The opportunity is particularly favorable for new entrants because temperature-controlled logistics remains relatively underdeveloped compared with conventional freight services. Establishing specialized cold storage facilities and compliant distribution networks allows smaller operators to differentiate through quality assurance, regulatory compliance, and service reliability. Emerging logistics firms can also integrate digital monitoring technologies and modular cold storage solutions more rapidly than legacy operators. As healthcare supply chains become more complex, specialized cold chain logistics providers are well-positioned to capture growing demand and scale operations across Egypt’s pharmaceutical distribution ecosystem.

Egypt Logistics Market Challenge:

Port Congestion and Urban Traffic Bottlenecks

Port congestion and urban traffic constraints remain a major operational challenge for Egypt’s logistics sector, driven by rising cargo volumes and infrastructure capacity limitations. Egypt’s strategic location along the Suez Canal has increased maritime traffic and container throughput across ports such as Alexandria, Damietta, and Sokhna. However, limited terminal capacity and aging transport connections between ports and inland distribution corridors often create operational delays. Operational shipping updates in 2026 reported that Egypt’s Port Said experienced an average vessel waiting time of approximately 3.63 days, highlighting ongoing congestion pressures on port handling capacity . It also reported that several LNG vessels were forced to wait outside Egypt’s import terminals, with one tanker remaining anchored for up to 11 days before docking due to scheduling and terminal congestion issues . According to reports from international shipping publications and port authorities, congestion during peak trade periods continues to slow container handling and cargo clearance.

The challenge is particularly visible in large urban logistics hubs such as Greater Cairo and Alexandria, where road congestion significantly affects freight mobility. Egypt’s expanding import, export, and e-commerce flows require efficient truck movement between ports, warehouses, and urban distribution centers. However, heavy traffic and limited dedicated freight corridors increase transportation time and operational costs for logistics companies. Delays in truck turnaround and container pickup can reduce supply-chain reliability and affect delivery schedules for manufacturers and retailers.

These infrastructure constraints materially limit logistics scalability and discourage rapid capacity expansion by market participants. When port operations or urban distribution networks experience congestion, shipment throughput declines and operational costs increase for freight operators and third-party logistics providers. As a result, companies must invest additional resources in scheduling, fleet management, and buffer inventory to maintain service reliability. Until freight infrastructure modernization and traffic management improvements accelerate, congestion will remain a structural barrier to logistics efficiency and market growth.

Egypt Logistics Market (2026-32) Segmentation Analysis:

The Egypt Logistics Market study of MarkNtel Advisors evaluates and highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Model Type:

- 2PL (Second Party Logistics)

- 3PL (Third Party Logistics)

- 4PL (Fourth Party Logistics)

The 3PL (Third-Party Logistics) segment dominates the Egypt Logistics Market, accounting for approximately 45% of total service demand, primarily because businesses increasingly outsource transportation, warehousing, and distribution operations to specialized logistics providers to improve efficiency and reduce capital expenditure. Egypt’s large consumer base and expanding trade activity generate significant freight volumes requiring coordinated supply-chain management. According to the World Bank, Egypt handled merchandise trade valued at over USD 200 billion in 2023, reflecting the scale of cargo flows that often require integrated logistics services rather than in-house transportation capabilities.

Industrial expansion and the growth of e-commerce have further strengthened demand for third-party logistics providers. Government-supported initiatives such as the Suez Canal Economic Zone (SCZone) continue to attract manufacturing and distribution investments, increasing demand for contract logistics, freight forwarding, and warehousing services. Companies operating in these industrial clusters frequently rely on 3PL providers to manage cross-border transportation, customs clearance, and distribution networks, enabling them to focus on core production activities while ensuring reliable logistics operations across domestic and international markets.

Operational flexibility also contributes to the segment’s dominance. Third-party providers offer scalable logistics networks that combine multimodal transport, modern warehousing facilities, and digital tracking systems. This allows manufacturers, retailers, and e-commerce companies to quickly adjust distribution capacity without investing heavily in fleets or storage infrastructure. As supply chains become more complex and time-sensitive, outsourcing logistics functions to specialized 3PL firms provides cost efficiency, operational expertise, and broader network coverage, reinforcing the segment’s leading share within Egypt’s logistics services market.

Based on Mode of Transport:

- Roadways

- Waterways

- Airways

- Railways

The roadways segment dominates the Egypt Logistics Market, accounting for approximately 54% of total transport demand, primarily because road transport remains the backbone of domestic freight movement and provides the most flexible distribution network across the country. Egypt’s economic activity is concentrated in major urban corridors such as Greater Cairo, Alexandria, and the Nile Delta, where trucking serves as the primary mode for moving consumer goods, agricultural products, and industrial materials. According to Egypt’s Ministry of Transport, nearly 94% of the country’s freight is transported by road , reflecting the heavy reliance on trucking networks for domestic cargo distribution.

Infrastructure expansion further reinforces the dominance of road transport. Egypt has significantly upgraded its highway system through national transport development programs designed to strengthen connectivity between ports, industrial zones, and inland consumption centers. Major maritime gateways such as Alexandria, Damietta, and Sokhna rely heavily on trucking networks to move containers and bulk cargo to warehouses, factories, and distribution hubs across the country. This extensive road connectivity ensures efficient first-mile and last-mile freight movement that other transport modes cannot easily replicate.

Operational flexibility also contributes to the segment’s leading share. Road freight enables direct door-to-door delivery, flexible routing, and faster response to changing shipment schedules compared with rail or maritime transport. Industries such as retail, manufacturing, agriculture, and e-commerce rely heavily on trucking networks to maintain continuous inventory flows and nationwide distribution coverage. The combination of extensive road infrastructure, high freight dependency on trucking, and strong demand for flexible distribution services continues to position roadways as the dominant mode of transport in Egypt’s logistics market.

Egypt Logistics Market (2026-32): Regional Projection

The Greater Cairo Region dominates the Egypt Logistics Market, accounting for approximately 36% of total regional demand, primarily because it represents the country’s largest economic and population center, generating substantial freight movement and distribution activity. According to Egypt’s Central Agency for Public Mobilization and Statistics (CAPMAS), the Greater Cairo metropolitan area hosts more than 20 million residents, making it one of the largest urban markets in the Middle East and North Africa . This high population concentration sustains strong demand for consumer goods distribution, e-commerce deliveries, and retail supply chains.

Industrial concentration and commercial infrastructure further reinforce the region’s logistics dominance. Greater Cairo hosts major industrial zones such as 6th of October City, 10th of Ramadan City, and New Cairo, which accommodate manufacturing facilities producing electronics, textiles, food products, chemicals, and consumer goods. These industrial clusters generate large volumes of inbound raw materials and outbound finished products requiring integrated logistics services. Additionally, Cairo functions as Egypt’s primary administrative and financial center, attracting multinational companies and large distribution hubs that rely on efficient freight transportation networks.

Strategic connectivity also strengthens Greater Cairo’s position as the country’s central logistics hub. The region is linked by extensive highway corridors connecting key maritime gateways such as Alexandria, Damietta, and Ain Sokhna ports, enabling efficient cargo movement between ports and inland markets. Cairo also hosts major logistics facilities, warehouses, and air cargo operations at Cairo International Airport. The combination of dense population demand, industrial production clusters, and multimodal transport connectivity positions the Greater Cairo Region as the leading logistics hub in Egypt’s national supply chain network.

Gain a Competitive Edge with Our Egypt Logistics Market Report:

- Egypt Logistics Market Report by MarkNtel Advisors provides a detailed and thorough analysis of market size and share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics and make informed decisions.

- This report also highlights current market trends and future projections, allowing businesses to identify emerging opportunities and potential challenges. By understanding market forecasts, companies can align their strategies and stay ahead of the competition.

- Egypt Logistics Market Report aids in assessing and mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks and optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Egypt Logistics Market Policies, Regulations, and Product Standards

- Egypt Logistics Market Trends & Developments

- Egypt Logistics Market Dynamics

- Growth Factors

- Challenges

- Egypt Logistics Market Hotspot & Opportunities

- Egypt Logistics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Service- Market Size & Forecast 2022-2032, USD Million

- Transportation Services

- Warehousing & Distribution Services

- Freight Forwarding Services

- Inventory Management Services

- Value-Added Logistics Services

- Integration & Consulting Services

- By Category- Market Size & Forecast 2022-2032, USD Million

- Conventional Logistics

- E-Commerce Logistics

- By Model Type- Market Size & Forecast 2022-2032, USD Million

- 2PL (Second Party Logistics)

- 3PL (Third Party Logistics)

- 4PL (Fourth Party Logistics)

- By Type- Market Size & Forecast 2022-2032, USD Million

- Forward Logistics

- Reverse Logistics

- By Operation- Market Size & Forecast 2022-2032, USD Million

- Domestic

- International

- By Mode of Transport- Market Size & Forecast 2022-2032, USD Million

- Roadways

- Waterways

- Airways

- Railways

- By End Use- Market Size & Forecast 2022-2032, USD Million

- Manufacturing

- Consumer Goods

- Retail

- Food and Beverages

- IT Hardware

- Healthcare

- Chemicals

- Construction

- Automotive

- Telecom

- Oil and Gas

- Others

- By Region - Market Size & Forecast 2022-2032, USD Million

- Greater Cairo Region

- Alexandria & Mediterranean Coast Region

- Suez Canal & Red Sea Corridor

- Nile Delta Region

- Upper Egypt Region

- Western Desert & Frontier Regions

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Service- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Egypt Forward Logistics Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Category- Market Size & Forecast 2022-2032, USD Million

- By Model Type- Market Size & Forecast 2022-2032, USD Million

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Operation- Market Size & Forecast 2022-2032, USD Million

- By Mode of Transport- Market Size & Forecast 2022-2032, USD Million

- By End Use- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Egypt Reverse Logistics Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Category- Market Size & Forecast 2022-2032, USD Million

- By Model Type- Market Size & Forecast 2022-2032, USD Million

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Operation- Market Size & Forecast 2022-2032, USD Million

- By Mode of Transport- Market Size & Forecast 2022-2032, USD Million

- By End Use- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Egypt Logistics Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- DHL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DB Schenker

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kuehne+Nagel

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DSV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CEVA Logistics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aramex

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FedEx

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- UPS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DHL

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now