Global Autonomous Driving Software Market Research Report: Growth Drivers & Forecast (2026-2032)

By Level of Autonomy (Level 1, Level 2, Level 3, Level 4, Level 5), By Vehicle Type (Passenger Vehicles, Commercial Vehicles), By Propulsion Type (Internal Combustion Engine (ICE), ... Electric Vehicles (EVs)), By Software Type (Perception and Planning Software, Chauffeur Software, Interior Sensing Software, Supervision & Monitoring Software), and others Read more

- ICT & Electronics

- Feb 2026

- Pages 195

- Report Format: PDF, Excel, PPT

Global Autonomous Driving Software Market

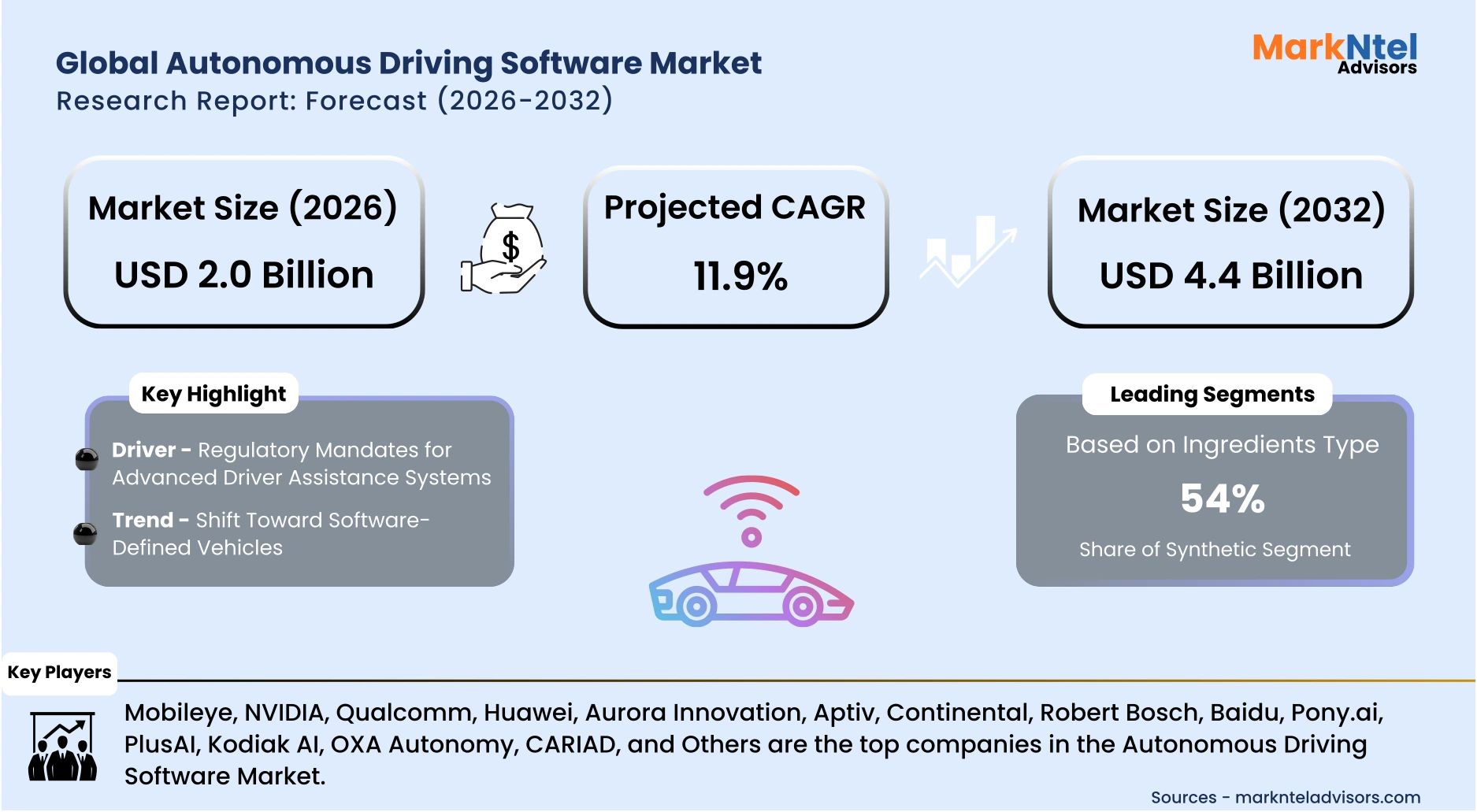

Projected 11.9% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 2.0 Billion

Market Size (2032)

USD 4.4 Billion

Largest Region

North America

Projected CAGR

11.9%

Leading Segments

By Propulsion Type: Internal Combustion Engine (ICE)

Global Autonomous Driving Software Market Report Key Takeaways:

- Market size is estimated at USD 2.0 billion in 2026 and is projected to reach USD 4.4 billion by 2032. The estimated CAGR from 2026 to 2032 is around 11.9%, indicating strong growth.

- North America holds the largest market share of about 48% in the Global Autonomous Driving Software Market in 2026.

- By Level of Autonomy, the Level 2 segment represented a significant share of about 55% in the Global Autonomous Driving Software Market in 2026.

- By Propulsion Type, the Internal Combustion Engine (ICE) segment seized a significant share of about 60% in the Global Autonomous Driving Software Market in 2026.

- Leading autonomous driving software Companies in the Global Market are Mobileye, NVIDIA, Qualcomm, Huawei, Aurora Innovation, Aptiv, Continental, Robert Bosch, Baidu, Pony.ai, PlusAI, Kodiak AI, OXA Autonomy, CARIAD, and Others.

Market Insights & Analysis: Global Autonomous Driving Software Market (2026-32):

The Global Autonomous Driving Software Market size is estimated at USD 2.0 billion in 2026 and is projected to reach USD 4.4 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 11.9% during the forecast period, i.e., 2026-32.

The global autonomous driving software market has progressed steadily due to regulatory acceptance and rising commercial validation of autonomous technologies. In 2025, NVIDIA released an open-source autonomous driving software platform aimed at accelerating development, simulation, and validation of self-driving systems, strengthening the software ecosystem supporting autonomy deployment .

Market conditions reflect a shift from experimental testing to structured commercial collaboration. In 2025, Stellantis entered a partnership with Pony.ai to jointly develop and deploy autonomous driving software across European markets, highlighting growing OEM reliance on specialized software providers to scale autonomous capabilities beyond pilot programs .

Industry-led initiatives have further supported market expansion by integrating autonomous software with mobility platforms. In 2025, Stellantis also announced a strategic collaboration with NVIDIA and Uber to advance robotaxi development, demonstrating how autonomous driving software is becoming central to commercial mobility services and fleet-based deployment models .

Overall, these developments indicate sustained market momentum driven by software modularization, OEM–technology partnerships, and commercial fleet adoption. The increasing availability of standardized and open autonomous driving software platforms in 2025 is expected to support broader adoption across passenger and commercial vehicles, reinforcing long-term demand growth for autonomous driving software solutions.

Global Autonomous Driving Software Market Recent Developments:

- 2025: Alphabet-backed Waymo raised a USD 16 billion funding round to accelerate robotaxi deployment into over 20 cities worldwide. The investment boosts autonomous driving software development and commercialization, underlining continued investor confidence in AV software platforms and services.

- 2026: Autonomous driving startup Waabi (AI-centric software) announced a major partnership with Uber to develop and support at least 25,000 robotaxis globally on Uber’s platform, injecting new competition and software innovation into the robotaxi segment .

Global Autonomous Driving Software Market Scope:

| Category | Segments |

|---|---|

| By Level of Autonomy | (Level 1, Level 2, Level 3, Level 4, Level 5), |

| By Vehicle Type | (Passenger Vehicles, Commercial Vehicles), |

| By Propulsion Type | (Internal Combustion Engine (ICE), Electric Vehicles (EVs)), |

| By Software Type | (Perception and Planning Software, Chauffeur Software, Interior Sensing Software, Supervision & Monitoring Software), |

Global Autonomous Driving Software Market Driver:

Regulatory Mandates for Advanced Driver Assistance Systems (ADAS)

One of the most decisive drivers accelerating the global autonomous driving software market is the expansion of government regulatory mandates requiring the integration and compliance of Advanced Driver Assistance Systems (ADAS) in new vehicles. These mandates are transforming ADAS from optional technology enhancements into legally required safety systems, compelling automakers to embed sophisticated software that governs functions such as adaptive braking, lane control, and driver monitoring. In several major markets, safety oversight bodies have introduced or tightened rules that directly impact autonomous driving software development.

In China, the Ministry of Industry and Information Technology implemented regulations in early 2025 requiring regulatory approval for over-the-air software upgrades related to autonomous driving systems to prevent hidden defects and enforce transparency in software changes, compelling automakers to secure licenses before deploying updates that alter key technical parameters . This effectively places autonomous and ADAS software under regulatory scrutiny previously reserved for hardware changes, broadening compliance requirements and software validation obligations.

The same regulatory tightening is reflected in actions taken to ban the use of terms like “smart driving” and “autonomous driving” in vehicle advertising, with authorities insisting that any upgrades or marketing claims be verified and approved to prevent misleading representations.

Furthermore, emerging regulations such as China’s draft safety rules for detecting driver disengagement in Level-2 systems, scheduled to take effect from 2027, will further raise compliance standards, ensuring that future ADAS software must incorporate sophisticated safety monitoring and risk mitigation capabilities .

Global Autonomous Driving Software Market Trend:

Shift Toward Software-Defined Vehicles (SDVs)

A defining trend in the global autonomous driving software market is the transition to software-defined vehicles (SDVs), where vehicle capabilities, performance, and user experience are increasingly governed by centralized software platforms rather than fixed hardware systems. SDVs enable over-the-air (OTA) updates, modular software services, and real-time system improvements, allowing vehicles to evolve continuously after sale. This shift aligns with global regulatory emphasis on software safety verification and cybersecurity, as seen in the European Union’s UNECE WP.29 regulations, which require functional safety and secure software management in all new vehicles from 2026 onwards.

In 2025, Toyota’s deployment of its Arene software development platform in the latest RAV4 model marked a concrete step toward SDV adoption by a major OEM, demonstrating how software platforms are being embedded deeply into vehicle electronics and user interfaces rather than remaining supplementary systems.

Government-driven safety and emissions regulations are further encouraging SDV adoption, as centralized software architectures allow real-time compliance monitoring, predictive maintenance, and adaptive driver assistance features. Countries such as Germany and Japan are providing incentives for connected and smart mobility systems, which further accelerates SDV integration.

Overall, by enabling continuous software updates, regulatory compliance, and scalable vehicle intelligence, the SDV trend is creating a structural shift in autonomous driving software demand, ensuring long-term market growth beyond 2025.

Global Autonomous Driving Software Market Opportunity:

Open‑Standard Autonomous Software Platforms for Mid‑Tier OEMs

A compelling market opportunity in the global autonomous driving software sector lies in the development and adoption of open‑standard software platforms that enable mid‑tier and regional original equipment manufacturers (OEMs) to access and integrate advanced autonomous driving functionalities without prohibitive costs. Such platforms promote interoperability, reduce duplicated engineering efforts, and establish common software foundations across multiple vehicle brands. In 2025, European automakers jointly launched a Memorandum of Understanding to develop a shared, open‑source automotive software ecosystem under the Eclipse Foundation’s S‑CORE project, aimed at producing core software components that can be standardized and certified for wide use by OEMs of all sizes .

These open standards are particularly valuable for mid‑tier OEMs that lack the financial scale of global incumbents yet face increasing regulatory and technical complexity in autonomous driving software. Using open, vendor‑neutral frameworks allows manufacturers to focus resources on differentiating features such as vehicle dynamics or user experience while relying on common, certifiable autonomy platforms.

Governments and regulatory bodies are increasingly supportive of such cooperative software frameworks, as they can enhance safety oversight and conformity with functional safety and cybersecurity standards without mandating proprietary solutions. These public endorsements reduce entry barriers for software deployment.

This opportunity is structurally significant because it lowers cost, speeds time‑to‑market, and fosters competition, enabling smaller OEMs to enter autonomous vehicle segments that were previously dominated by large manufacturers.

Global Autonomous Driving Software Market Challenge:

Regulatory Complexity and Compliance Burden on Autonomous Driving Software

A major challenge in the global autonomous driving software market is the growing regulatory complexity and compliance burden imposed by evolving international and national governance frameworks. Autonomous and connected vehicles increasingly fall under stringent type‑approval requirements for software update management systems (SUMS) and cybersecurity, as set forth by United Nations Economic Commission for Europe (UNECE) Regulations No. 155 and No. 156. These regulations require manufacturers to demonstrate secure software change procedures, establish organizational cybersecurity controls, and maintain traceable over‑the‑air update mechanisms before vehicles can be legally sold.

UNECE Regulation 155 mandates a formal Cyber Security Management System (CSMS) for all vehicles with automated and networked functions, requiring documentation and organizational governance to identify and mitigate cyber threats across the vehicle lifecycle. Regulation 156 requires secure and auditable processes for software updates, increasing development and certification workload for software suppliers and OEMs alike .

In the U.S., the National Highway Traffic Safety Administration (NHTSA) continues to exercise enforcement authority over automated driving systems through defect investigations and recall actions when software faults pose safety risks, such as improperly responding to traffic conditions . Prior recalls and probes, including cases where autonomous vehicle software updates were required to address unexpected behavior, highlight ongoing regulatory scrutiny and the associated compliance risk for developers.

These multi‑layered regulatory frameworks, spanning cybersecurity, update management, type approval, and defect reporting requirements, elevate development costs, extend certification timelines, and create barriers to entry for smaller software firms. Addressing this challenge will require harmonized regulatory approaches and clearer compliance pathways to reduce operational burden without compromising on safety.

Global Autonomous Driving Software Market (2026-32) Segmentation Analysis:

The Global Autonomous Driving Software Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the global level. Based on the analysis, the market has been further classified as;

Based on Level of Autonomy:

- Level 1

- Level 2

- Level 3

- Level 4

- Level 5

Level‑2 autonomous driving systems are the leading segment, accounting for 55% of market size, due to their widespread deployment across mid-range passenger vehicles. These systems offer combined adaptive cruise control and lane-keeping assistance while keeping the driver engaged, providing a practical balance between safety, affordability, and regulatory acceptance. OEMs favor Level‑2 solutions because they require less complex sensor fusion and software compared to Level‑3 or higher systems, reducing development costs and easing compliance with global safety standards such as UNECE WP.29. Governments in North America, Europe, and Asia are increasingly approving Level‑2 ADAS functionalities, promoting rapid adoption. Additionally, Level‑2 vehicles benefit from established infrastructure compatibility, making them accessible to mainstream consumers while allowing incremental software upgrades to improve performance over time.

Based on Propulsion Type:

- Internal Combustion Engine (ICE)

- Electric Vehicles (EVs)

Internal Combustion Engine (ICE) vehicles dominate the autonomous software market with 60% share, as they still constitute the largest portion of global vehicle fleets, particularly in Asia, Europe, and North America. ICE vehicles are often retrofitted or newly manufactured with Level‑2 autonomous capabilities, allowing software integration without the need for fully electric platforms. Many mid-tier OEMs continue to produce ICE vehicles for affordability and infrastructure readiness, especially in regions where EV charging networks are limited. The established supply chain and regulatory familiarity with ICE systems facilitate faster deployment of ADAS and autonomous software solutions, making ICE vehicles the primary platform for incremental automation adoption worldwide.

Global Autonomous Driving Software Market (2026-32): Regional Projection

The market for autonomous driving software is dominated by North America, accounting for 48% market share. This region leads due to its advanced automotive ecosystem, high adoption of connected and automated vehicle technologies, and supportive regulatory framework for ADAS and autonomous systems. The U.S. and Canada host numerous OEMs, Tier‑1 suppliers, and technology companies actively developing Level‑2 and Level‑3 autonomous platforms. States such as California, Michigan, and Texas serve as hubs for autonomous vehicle testing, offering regulatory sandboxes and safety guidelines that accelerate deployment. For example, companies like Waymo, Tesla, and General Motors conduct extensive on-road trials in these states under government-approved programs.

North America also benefits from high consumer acceptance of advanced driver assistance features, established insurance frameworks for autonomous operations, and extensive vehicle fleet data collection, all of which strengthen software performance and reliability. Consequently, these structural, regulatory, and technological factors collectively sustain North America’s market dominance in autonomous driving software.

Gain a Competitive Edge with Our Global Autonomous Driving Software Market Report:

- Global Autonomous Driving Software Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Global Autonomous Driving Software Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Global Autonomous Driving Software Market Policies, Regulations, and Product Standards

- Global Autonomous Driving Software Market Trends & Developments

- Global Autonomous Driving Software Market Dynamics

- Growth Factors

- Challenges

- Global Autonomous Driving Software Market Hotspot & Opportunities

- Global Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- Level 1

- Level 2

- Level 3

- Level 4

- Level 5

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- Passenger Vehicles

- Commercial Vehicles

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- Internal Combustion Engine (ICE)

- Electric Vehicles (EVs)

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Perception and Planning Software

- Chauffeur Software

- Interior Sensing Software

- Supervision & Monitoring Software

- By Region

- North America

- South America

- Europe

- The Middle East & Africa

- Asia-Pacific

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- North America Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- By Country

- The US

- Canada

- Mexico

- Rest of North America

- The US Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Canada Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Mexico Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- South America Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Argentina Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- Europe Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- By Country

- The UK

- Italy

- Germany

- France

- Spain

- Sweden

- BENELUX

- Rest of Europe

- The UK Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Italy Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Germany Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- France Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Sweden Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- BENELUX Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- The Middle East & Africa Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- By Country

- Saudi Arabia

- UAE

- South Africa

- Bahrain

- Rest of Middle East & Africa

- Saudi Arabia Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- South Africa Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Bahrain Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- Asia-Pacific Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Rest of Asia-Pacific

- China Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- South Korea Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Australia Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Indonesia Autonomous Driving Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Level of Autonomy- Market Size & Forecast 2022-2032, USD Million

- By Vehicle Type- Market Size & Forecast 2022-2032, USD Million

- By Propulsion Type- Market Size & Forecast 2022-2032, USD Million

- By Software Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- Global Autonomous Driving Software Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Mobileye

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NVIDIA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Qualcomm

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huawei

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aurora Innovation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aptiv plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Continental AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Robert Bosch GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Baidu, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- OXA Autonomy Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CARIAD

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pony.ai

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PlusAI Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kodiak AI, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mobileye

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now