Asia Air Purifier Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Product Type (Room Air Purifier, Central/Whole-Home Air Purifier, Portable Air Purifier, Smart Air Purifier, Industrial/Commercial Purifier), By Filter Type (High-Frequency Part ... iculate Air (HEPA) filters, HEPA+ Activated Carbon, HEPA+ Activated Carbon + Ion, HEPA+ Electrostatic Precipitators, HEPA+ Ion & Ozone, Others), By Sales Channel (Online Sales, Offline Sales), By End User (Residential, Commercial, Industrial, Institutional), and others Read more

- Environment

- Feb 2026

- Pages 260

- Report Format: PDF, Excel, PPT

Asia Air Purifier Market

Projected 9.83% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 3.92 Billion

Market Size (2032)

USD 6.88 Billion

Base Year

2025

Projected CAGR

9.83%

Leading Segments

By Product Type: Room Air Purifier

Asia Air Purifier Market Report Key Takeaways:

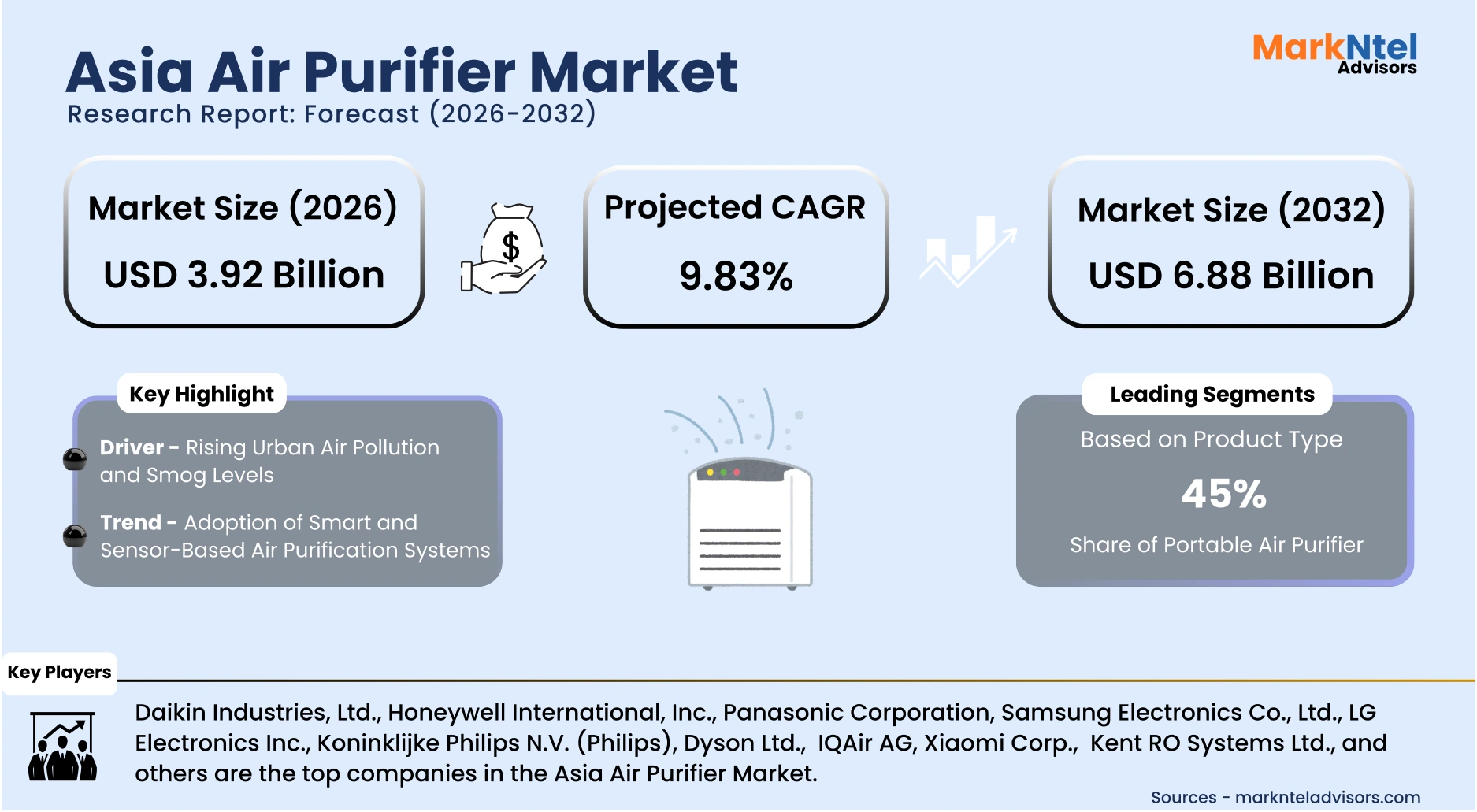

- The Asia Air Purifier Market size was valued at around USD 3.13 billion in 2025 and is projected grow from USD 3.92 billion in 2026 to USD 6.88 billion by 2032, exhibiting a CAGR of 9.83% during the forecast period.

- China holds the largest market share of about 41% in the Asia Air Purifier Market in 2026.

- By Product Type, the Portable Air Purifier segment represented a significant share of about 45% in the Asia Air Purifier Market in 2026.

- By Filter Type, the HEPA + Activated Carbon segment presented a significant share of about 43% in the Asia Air Purifier Market in 2026.

- Leading Air Purifier companies in the Asia Market are Daikin Industries, Ltd., Honeywell International, Inc., Panasonic Corporation, Samsung Electronics Co., Ltd., LG Electronics Inc., Koninklijke Philips N.V. (Philips), Dyson Ltd., Blueair (Blueair AB), IQAir AG, Xiaomi Corp., Coway Co., Ltd., Sharp Corporation, Whirlpool Corporation, Midea Group Co., Ltd., Nirvana Being, Hokocare, MayAir, Levoit (Vesync Co., Ltd.), Kent RO Systems Ltd., and Others.

Market Insights & Analysis: Asia Air Purifier Market (2026-32):

The Asia Air Purifier Market size was valued at around USD 3.13 billion in 2025 and is projected grow from USD 3.92 billion in 2026 to USD 6.88 billion by 2032, exhibiting a CAGR of 9.83% during the forecast period, i.e., 2026-32.

Air pollution in Asia remains a significant public health issue and has historically driven demand for air filtration technologies such as air purifiers. Average annual PM2.5 concentrations in many Asian urban areas continue to exceed recommended safety thresholds, with only a limited share of cities meeting clean air targets, underscoring sustained public concern about indoor and outdoor air quality. The World Health Organization reports that environmental risks account for nearly 24% of the global disease burden, with air pollution alone responsible for almost 7 million premature deaths annually, highlighting the scale of exposure across densely populated regions. In 2025, updated global air quality standards and national pollutant benchmark databases further reflected institutional recognition of pollution as a systemic health risk, while continued urban exposure to PM2.5 remains a leading indicator of environmental burden. These developments have historically contributed to rising residential adoption of air purifiers as households seek effective indoor filtration amid persistently elevated pollution levels .

Current environmental conditions and national policy responses continue to influence market dynamics across Asia. For example, India’s capital region has implemented the highest level of pollution curbs in response to winter smog episodes, including vehicle restrictions and construction halts to protect public health, reflecting recognition of air quality risks by government authorities . In parallel, national ambient air quality indicators have shown gradual improvements in some Indian metropolitan regions, with average AQI (air quality index) improvements reported from 2018 to 2025 . In China, ambitious targets to eliminate severe air pollution by the end of 2025 have included strengthened forecasting, emissions management, and transportation planning measures, demonstrating how regulatory action continues to shape environmental governance and end-user demand for mitigation technologies .

Regulatory frameworks across Asian economies have underscored indoor air quality as part of broader public health strategies, reinforcing consumer and institutional interest in air purifiers. WHO’s updated air quality standards provide comparative insights into national pollutant limits, highlighting efforts by multiple countries to align with evidence-based air quality benchmarks . National initiatives like India’s National Clean Air Programme (NCAP) and regional collaborative frameworks have expanded monitoring and enforcement infrastructure, motivating both residential and commercial sectors to adopt air filtration solutions. These policy and monitoring developments create an environment where air purifiers are increasingly considered essential for health protection in indoor environments.

Industry responses to these environmental and regulatory drivers include expanded product portfolios and region-specific strategies. Manufacturers have introduced energy-efficient and smart air purifiers tailored to local standards and consumer preferences, aligning with government programs to electrify households and improve urban living standards. Continued urbanization, demographic growth in at-risk populations, and enforcement of air quality guidelines suggest that demand for effective indoor air purification solutions will remain robust through the latter half of the decade, supporting sustained market growth in Asia.

Asia Air Purifier Market Recent Developments:

- 2025 : LG Electronics introduced the LG PuriCare AeroBooster air care solution across several Asian markets in January 2025, featuring advanced Aero Series V filters, Dual Airflow circulation, UVnano™ hygiene technology, and AI+ mode for energy savings. The premium design and smart features target improved indoor air quality in homes across Vietnam, Thailand, Japan, Malaysia, and Singapore.

- 2024 : Philips, under Versuni India, launched new air purifiers in India, including the 3200, 4200 Pro, and 900 Mini models, priced from approximately USD 120. The models are designed to deliver quiet and efficient air purification with advanced filtration features, including Wi-Fi-enabled options to enhance indoor air quality in residential spaces.

Asia Air Purifier Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Room Air Purifier, Central/Whole-Home Air Purifier, Portable Air Purifier, Smart Air Purifier, Industrial/Commercial Purifier), |

| By Filter Type | (High-Frequency Particulate Air (HEPA) filters, HEPA+ Activated Carbon, HEPA+ Activated Carbon + Ion, HEPA+ Electrostatic Precipitators, HEPA+ Ion & Ozone, Others), |

| By Sales Channel | (Online Sales, Offline Sales), |

| By End User | (Residential, Commercial, Industrial, Institutional), |

Asia Air Purifier Market Driver:

Rising Urban Air Pollution and Smog Levels

Rapid industrial expansion, coal-dependent power generation, vehicle density growth, construction activity, and seasonal biomass burning have structurally intensified air pollution across major Asian economies. Indonesia, where coal accounts for roughly two-thirds of electricity generation and coal capacity expanded by about 15% through mid-2024, illustrates how energy structure contributes to sustained particulate emissions. In South Asia, high urban population density combined with transport congestion and industrial clustering further compounds localized PM2.5 accumulation. These systemic emission sources explain why pollution remains persistent rather than temporary.

The 2024 World Air Quality Report shows that 74 of the world’s 100 most polluted cities were in India, while Bangladesh ranked among the most polluted countries globally, highlighting concentrated exposure across the region. India’s national average PM2.5 level reached 50.6 µg/m³ in 2024, nearly ten times the recommended safety thresholds, reflecting structural emission pressures. Indonesia remained the most polluted country in Southeast Asia despite a 4% annual improvement, demonstrating that incremental reductions have not yet resolved baseline pollution levels. Such conditions reinforce continuous exposure in high-density urban centers .

This structural pollution environment materially expands the air purifier market volume rather than merely influencing pricing. Only 17% of nearly 9,000 surveyed cities globally met recommended PM2.5 standards, indicating that unsafe exposure remains widespread and recurring. Vietnam’s air pollution has been estimated to reduce national GDP by approximately 4%, underscoring its macroeconomic impact . As emission-intensive growth models persist alongside expanding urban populations, sustained environmental exposure continues to generate durable, first-time adoption and multi-year penetration growth across Asia’s air purifier market.

Asia Air Purifier Market Trend:

Adoption of Smart and Sensor-Based Air Purification Systems

The integration of sensors, connectivity modules, and artificial intelligence into air purifiers represents a structural shift in product architecture and user engagement across Asia. Rising smartphone penetration and expanding broadband access, as reported by the International Telecommunication Union, have enabled widespread adoption of app-connected household devices. Governments across Asia continue to promote digital infrastructure expansion under national digital economy strategies, accelerating Internet of Things integration in residential appliances. This ecosystem has facilitated real-time air quality monitoring, automated purification modes, and remote management features as standard consumer expectations rather than premium add-ons.

The trend is reshaping industry dynamics by transforming air purifiers from standalone hardware into data-enabled indoor air management systems. Manufacturers are increasingly embedding PM2.5 sensors, cloud-based analytics, and voice-assistant compatibility to align with smart home platforms. During the 2024 festive season, Dyson introduced the Purifier Cool TP11 in India with real-time AQI responsiveness , while Xiaomi launched the Mijia Smart Air Purifier 6 in China, featuring formaldehyde removal, multi-pollutant sensors, and smart home integration, reinforcing the move toward intelligent air purification solutions. Retail channels have shifted toward online-first sales models, where consumers compare live air quality metrics and performance specifications digitally.

This transition is expected to persist because it aligns with long-term digitalization, energy efficiency, and public health transparency objectives. Governments continue to invest in smart city programs that integrate connected infrastructure and environmental monitoring frameworks. As consumers demand measurable proof of air quality improvement rather than passive filtration, sensor-based verification becomes essential. Consequently, smart purification systems are redefining value propositions and structurally influencing long-term market evolution across Asia.

Asia Air Purifier Market Opportunity:

Expansion into Institutional and Healthcare Infrastructure

The expansion of healthcare and institutional infrastructure across Asia presents a structural entry opportunity for emerging air purifier manufacturers. According to the World Bank, health expenditure across South and East Asia has continued to rise in recent years, reflecting sustained public and private investment in hospitals and medical facilities. Governments, including India and Indonesia, are increasing budget allocations for healthcare capacity expansion and primary care infrastructure through national health missions and public facility upgrades, with Indonesia allocating approximately USD 15 billion to its national health budget in 2025 . Additionally, India’s Union Budget 2026 increased health sector allocation by nearly 10% to approximately USD 12.8 billion, directing additional funding toward hospitals, medical education, and emergency care infrastructure . The post-pandemic emphasis on infection prevention and indoor air quality standards has further strengthened institutional awareness of controlled indoor environments.

This opportunity translates into tangible demand because hospitals, clinics, laboratories, and educational institutions require high-efficiency filtration systems to manage airborne pathogens and maintain compliant indoor conditions. Peer-reviewed research published in medical journals has reinforced the role of HEPA-based filtration in reducing airborne particulate and microbial load in enclosed clinical spaces. Notably, in 2024, Smart Air reported supplying more than 1,000 HEPA-based air purification units across over 130 hospitals in the Philippines, indicating expanding institutional-scale adoption in healthcare settings . As new healthcare facilities are constructed or retrofitted, procurement specifications increasingly include mechanical ventilation upgrades and standalone purification units.

The segment is particularly attractive for new and smaller players because institutional procurement often prioritizes performance, compliance, and cost efficiency over brand legacy. Local manufacturers can compete by offering application-specific systems, maintenance contracts, and localized servicing networks. Public tenders and decentralized procurement models in emerging economies lower barriers to entry compared to premium consumer retail channels. As healthcare infrastructure continues expanding under national development programs, scalable institutional demand provides a stable growth pathway for emerging market participants.

Asia Air Purifier Market Challenge:

High Replacement and Maintenance Costs of Advanced Filtration Systems

The high replacement and maintenance costs associated with advanced HEPA and multi-stage filtration systems represent a structural barrier to wider air purifier adoption across Asia. High-efficiency particulate air (HEPA) filters require periodic replacement to maintain certified performance standards, particularly in environments with elevated particulate concentrations. In many Asian cities where PM2.5 levels frequently exceed recommended limits, filter clogging accelerates, shortening replacement cycles. This raises recurring ownership costs beyond the initial device purchase, particularly in price-sensitive emerging economies.

The financial burden is measurable at both household and institutional levels. Public hospitals operating under fixed annual budgets must allocate recurring expenditure for filter procurement and system servicing, which can constrain procurement decisions despite rising infrastructure allocations. In highly polluted cities such as Delhi, where AQI levels can exceed 300 during winter, purifier filters reportedly clog within 15 days in 2024, leading to seasonal replacement costs of approximately USD 240–360 per household . For residential consumers, replacement filters for branded systems often represent a significant proportion of the original unit cost over a multi-year period. In countries with higher import dependence for specialized filtration media, currency fluctuations and logistics costs further increase end-user expenditure, affecting long-term affordability.

This structural cost burden materially restricts market expansion by limiting sustained usage and repeat purchases. Price-sensitive consumers may delay filter replacement, reducing system efficiency and undermining perceived value, which can slow penetration rates. Smaller market entrants also face inventory and supply chain pressures in maintaining consistent filter availability. As advanced filtration technologies remain essential for performance compliance, ongoing maintenance expenditure continues to act as a scalability constraint across the Asia air purifier market.

Asia Air Purifier Market (2026-32) Segmentation Analysis:

The Asia Air Purifier market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Room Air Purifier

- Central/Whole-Home Air Purifier

- Portable Air Purifier

- Smart Air Purifier

- Industrial/Commercial Purifier

The portable air purifier segment dominates the Asia Air Purifier Market, accounting for approximately 45% of total demand, primarily because urban households require flexible, room-specific filtration solutions rather than centralized systems. Asia’s rapid urbanization has intensified apartment living; according to the United Nations, over half of Asia’s population now resides in urban areas, with megacities continuing to expand. High-rise residential structures and rental accommodations often lack integrated HVAC systems capable of supporting whole-home purification. Portable units, therefore, provide an accessible and installation-free solution suited to dense metropolitan environments.

Affordability and ease of deployment further reinforce segment dominance. Portable air purifiers eliminate the need for structural retrofitting, making them suitable for rented homes, small offices, and dormitories where infrastructure modifications are restricted. In highly polluted cities such as Delhi and Jakarta, seasonal AQI spikes drive immediate retail demand for plug-and-play devices that can be relocated between bedrooms and living areas. E-commerce expansion across Asia has also facilitated direct-to-consumer sales of compact purifier models, accelerating volume penetration across middle-income households.

Industrial structure supports this leadership position. Major manufacturers, including Xiaomi, Philips, and Dyson, prioritize portable models within their Asia product portfolios, emphasizing smart connectivity and energy efficiency; for instance, Xiaomi has expanded its portfolio with plans to introduce new portable air purifiers, including compact variants potentially designed for automotive use at accessible price points . Portable units also align with rising consumer preference for lower upfront capital expenditure compared to centralized systems. The combination of urban density, infrastructure constraints, price sensitivity, and rapid deployment capability continues to position portable air purifiers as the dominant product category across Asia’s evolving indoor air quality market.

Based on Filter Type:

- High-Frequency Particulate Air (HEPA) filters

- HEPA+ Activated Carbon

- HEPA+ Activated Carbon + Ion

- HEPA+ Electrostatic Precipitators

- HEPA+ Ion & Ozone

- Others

The HEPA + Activated Carbon segment dominates the Asia Air Purifier Market, accounting for approximately 43% of total demand, primarily because urban pollution across the region comprises both particulate matter and gaseous contaminants. According to global air quality assessments, many Asian cities continue to record elevated PM2.5 concentrations alongside high levels of volatile organic compounds (VOCs) and nitrogen oxides from transport, industry, and household emissions. HEPA filtration is certified to remove at least 99.97% of particles as small as 0.3 microns, making it effective against fine particulate pollution. However, HEPA alone cannot neutralize odors or chemical gases, necessitating the integration of activated carbon layers for comprehensive indoor protection.

Industrial and institutional procurement patterns further reinforce this dominance. Hospitals and commercial facilities increasingly require multi-stage filtration capable of managing both airborne pathogens and chemical pollutants in enclosed environments. Activated carbon is widely recognized for its adsorption capacity against formaldehyde, smoke, and household VOCs, which are common in dense residential settings with limited ventilation. As Asian households experience seasonal smog events and indoor pollution from cooking and furnishings, dual-stage systems offer broader protection without the safety concerns associated with ozone-generating technologies.

Manufacturing standardization also supports segment leadership. Major brands across China, Japan, South Korea, and India predominantly configure mid-range and premium models with combined HEPA and carbon filters; for instance, Sharp Business Systems India recently launched its PureFit series featuring electrostatic HEPA and activated carbon triple filtration systems with smart connectivity options. This balanced combination of particulate efficiency, gaseous adsorption capability, regulatory acceptability, and scalable production continues to position HEPA + Activated Carbon systems as the leading filtration category across Asia’s air purifier market.

Asia Air Purifier Market (2026-32): Regional Projection

China dominates the Asia Air Purifier Market, accounting for approximately 41% of total regional demand, primarily because it combines the region’s largest urban consumer base with the most extensive domestic manufacturing ecosystem. According to the National Bureau of Statistics of China, the country’s urbanization rate exceeded 66% in recent years, translating into hundreds of millions of urban households exposed to dense metropolitan air conditions. Large population centers such as Beijing, Shanghai, and Guangzhou sustain high residential appliance consumption volumes. This scale effect structurally elevates baseline demand relative to other Asian economies.

Industrial capacity further reinforces China’s leadership. China remains the world’s largest manufacturing economy, with the World Bank reporting that it contributes over a quarter of global manufacturing value added. The country hosts a concentrated network of appliance manufacturers, component suppliers, and filter media producers, enabling cost-efficient mass production of air purifiers across entry-level and premium segments. Domestic brands such as Xiaomi, Midea, and Haier benefit from integrated supply chains and strong e-commerce penetration, which reduces distribution costs and accelerates product turnover. This vertically integrated ecosystem supports both domestic consumption and regional exports.

Policy and regulatory emphasis on air quality management also sustains long-term market volume. China has implemented multi-year clean air action plans targeting particulate reduction and industrial emission control, increasing public awareness of indoor air protection. Despite improvements in certain regions, seasonal pollution events continue to reinforce precautionary household adoption. The combination of large-scale urban demand, manufacturing dominance, digital retail infrastructure, and sustained environmental policy focus structurally positions China ahead of other Asian markets in overall air purifier consumption and market share.

Gain a Competitive Edge with Our Asia Air Purifier Market Report:

- Asia Air Purifier Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Asia Air Purifier Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Asia Air Purifier Market Policies, Regulations, and Product Standards

- Asia Air Purifier Market Trends & Developments

- Asia Air Purifier Market Country & Company Wise Pricing Analysis, 2026

- Historical Price Trend- By Companies’ SKUs

- Cost Fluctuation in Raw Materials

- Others

- Asia Air Purifier Market Import & Export Tariffs, By Country

- China

- India

- Japan

- South Korea

- Southeast Asia

- Asia Air Purifier Market Gap Analysis, 2026

- Asia Air Purifier Market Dynamics

- Growth Factors

- Challenges

- Asia Air Purifier Market Hotspot & Opportunities

- Asia Air Purifier Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Room Air Purifier

- Central/Whole-Home Air Purifier

- Portable Air Purifier

- Smart Air Purifier

- Industrial/Commercial Purifier

- By Filter Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- High-Frequency Particulate Air (HEPA) filters

- HEPA+ Activated Carbon

- HEPA+ Activated Carbon + Ion

- HEPA+ Electrostatic Precipitators

- HEPA+ Ion & Ozone

- Others

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Online Sales

- Offline Sales

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Residential

- Commercial

- Industrial

- Institutional

- By Country

- China

- India

- Japan

- South Korea

- Southeast Asia

- Rest of Asia

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- China Air Purifier Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Filter Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- India Air Purifier Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Filter Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- Japan Air Purifier Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Filter Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- South Korea Air Purifier Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Filter Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- Southeast Asia Air Purifier Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Filter Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By End User- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- Asia Air Purifier Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Daikin Industries, Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honeywell International, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panasonic Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samsung Electronics Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Electronics Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Koninklijke Philips N.V. (Philips)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dyson Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Blueair (Blueair AB)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IQAir AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Xiaomi Corp.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coway Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sharp Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Whirlpool Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Midea Group Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nirvana Being

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hokocare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- MayAir

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Levoit (Vesync Co., Ltd.)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kent RO Systems Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daikin Industries, Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now