Vietnam Healthcare Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Healthcare Expenditure Type (Public Healthcare Expenditure, Private Healthcare Expenditure, Out-of-Pocket Expenditure), By Pharmaceutical Segment (Prescription Drugs, Over-the-C ... ounter (OTC) Drugs, Generic Drugs, Branded Drugs, Biologics & Biosimilars), By Therapeutic Area (Cardiovascular Diseases, Oncology, Diabetes, Respiratory Diseases, Neurology, Infectious Diseases, Others), By Medical Device Type (Diagnostic Imaging Devices, Patient Monitoring Devices, Surgical Equipment, In-vitro Diagnostics, Orthopedic Devices, Cardiovascular Devices, Others), By Technology Type (Artificial Intelligence in Healthcare, Telemedicine & Remote Monitoring, Electronic Health Records (EHR), Healthcare Analytics, Robotic Surgery, Wearables & Health Apps), By Healthcare Workforce (Physicians, Nurses, Dentists, Allied Health Professionals), By Insurance Type (Public Health Insurance, Private Health Insurance), By Disease Category (Chronic Diseases, Infectious Diseases, Mental Health Disorders), By End User (Hospitals, Clinics, Diagnostic Centers / Laboratories, Ambulatory Surgical Centers, Home Healthcare, Research Institutes, Pharmacies, Others) Read more

- Healthcare

- Mar 2026

- Pages 160

- Report Format: PDF, Excel, PPT

Vietnam Healthcare Market

Projected 8.64% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 13.95 Million

Market Size (2032)

USD 22.93 Million

Base Year

2025

Projected CAGR

8.64%

Leading Segments

By Therapeutic Area: Cardiovascular Diseases

Vietnam Healthcare Market Report Key Takeaways:

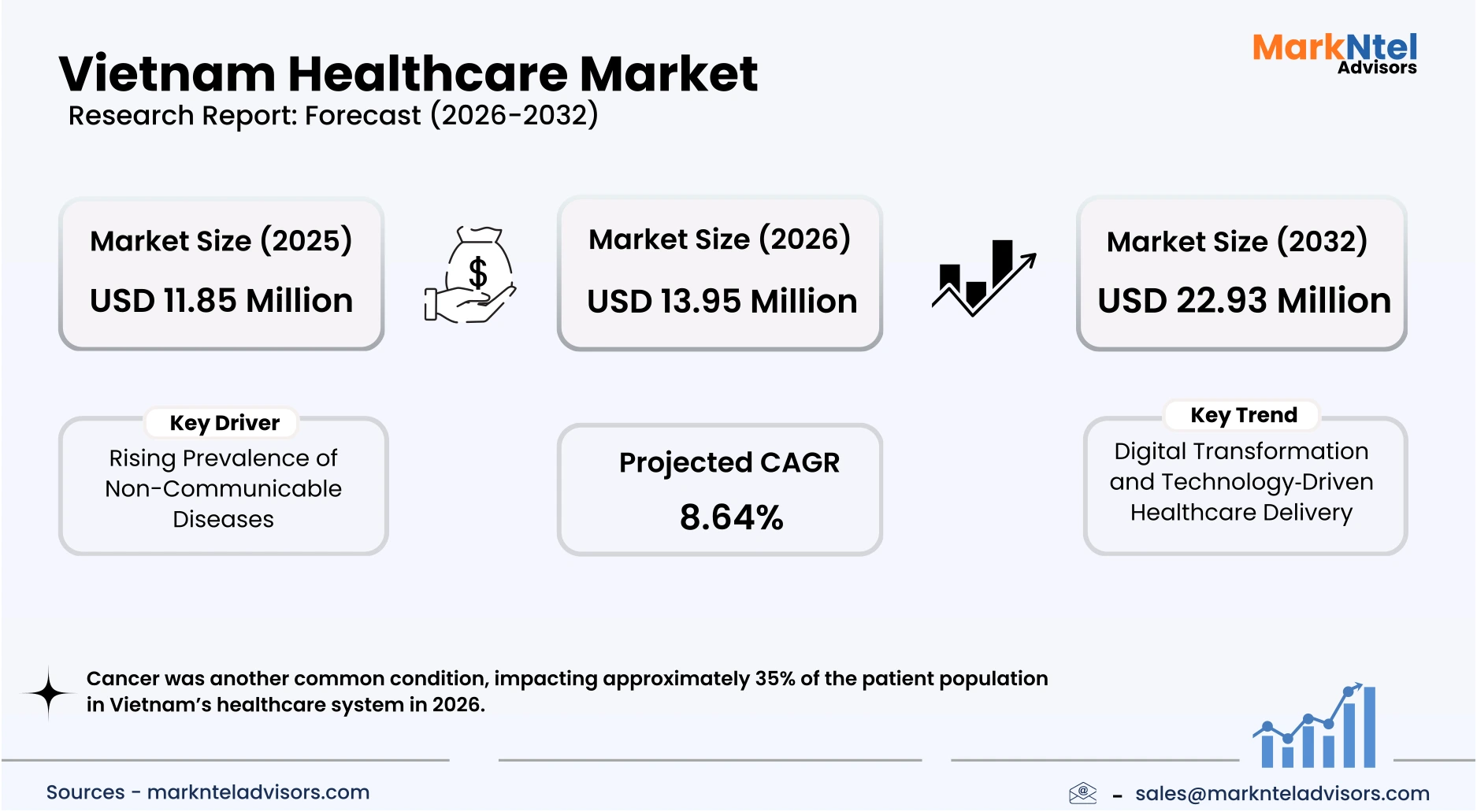

- The Vietnam Healthcare Market size was valued at USD 11.85 million in 2025 and is projected to grow from USD 13.95 million in 2026 to USD 22.93 million by 2032, exhibiting a CAGR of 8.64% during 2026-32.

- About 25% of patients in Vietnam’s healthcare system in 2026 were affected by cardiovascular diseases, highlighting a significant prevalence.

- Cancer was another common condition, impacting approximately 35% of the patient population in Vietnam’s healthcare system in 2026.

- Vietnam’s healthcare infrastructure includes 1,718 hospitals, over 350,000 beds, and numerous rehabilitation and residential care facilities.

Market Insights & Analysis: Vietnam Healthcare Market Landscape (2026-32):

The Vietnam Healthcare Market size was valued at USD 11.85 million in 2025 and is projected to grow from USD 13.95 million in 2026 to USD 22.93 million by 2032, exhibiting a CAGR of 8.64% during the forecast period, i.e., 2026-32.

Vietnam’s healthcare landscape is transitioning through structural reforms and investment in service quality, underpinned by ongoing national health agendas focused on disease prevention, primary care strengthening, and digital transformation. Politburo Resolution No. 72 (2025) and the recently adopted Law on Disease Prevention have reoriented the system toward proactive health promotion and expanded preventive services beyond traditional infectious disease control. According to 2025 data, non-communicable diseases (NCDs), including cardiovascular conditions, cancer, chronic respiratory disease, and diabetes, remain the leading cause of mortality, accounting for approximately 80% of all deaths, driving expanded demand for long‑term care and specialist services.

As of the end‑of 2024, Vietnam’s hospital network comprised over 1,700 facilities, with bed availability estimated at 34 beds per 10,000 people, meeting or exceeding national targets and reflecting decades of capacity growth. High demand is evidenced by widespread outpatient care, with millions of visits recorded annually, particularly in institutional settings such as district and central hospitals.

Disease trends show a rising clinical burden of metabolic dysfunction‑associated with fatty liver disease (MAFLD), affecting over 20% of adults in urban populations, closely tied with diabetes and obesity, and increasing utilization of tertiary care resources. Concurrently, dengue incidence in 2025 surged to over 181,000 reported cases with associated mortality, highlighting persistent infectious disease pressures alongside NCDs. These dual disease burdens are shaping patient demand patterns across institutional and community health services, influencing capacity planning and resource allocation across the sector.

The Vietnamese government has pursued expanded health insurance coverage through social health insurance reforms, achieving high coverage rates among citizens and facilitating increased utilization of health services. Strategic investments in digital health, electronic health records, and telemedicine aim to improve patient flow, reduce hospital overcrowding, and enhance access for rural and marginalized populations.

In summary, Vietnam’s healthcare market is expanding within a framework of regulatory reform, demographic change, and disease transition, supported by government policy, infrastructure enhancement, and technology adoption. These developments are expected to sustain healthcare demand growth through 2032 as capacity, digital integration, and preventive care frameworks continue to evolve.

Vietnam Healthcare Market Scope:

| Category | Segments |

|---|---|

| By Healthcare Expenditure Type | (Public Healthcare Expenditure, Private Healthcare Expenditure, Out-of-Pocket Expenditure), |

| By Pharmaceutical Segment | (Prescription Drugs, Over-the-Counter (OTC) Drugs, Generic Drugs, Branded Drugs, Biologics & Biosimilars), |

| By Therapeutic Area | (Cardiovascular Diseases, Oncology, Diabetes, Respiratory Diseases, Neurology, Infectious Diseases, Others), |

| By Medical Device Type | (Diagnostic Imaging Devices, Patient Monitoring Devices, Surgical Equipment, In-vitro Diagnostics, Orthopedic Devices, Cardiovascular Devices, Others), |

| By Technology Type | (Artificial Intelligence in Healthcare, Telemedicine & Remote Monitoring, Electronic Health Records (EHR), Healthcare Analytics, Robotic Surgery, Wearables & Health Apps), |

| By Healthcare Workforce | (Physicians, Nurses, Dentists, Allied Health Professionals), |

| By Insurance Type | (Public Health Insurance, Private Health Insurance), |

| By Disease Category | (Chronic Diseases, Infectious Diseases, Mental Health Disorders), |

| By End User | (Hospitals, Clinics, Diagnostic Centers / Laboratories, Ambulatory Surgical Centers, Home Healthcare, Research Institutes, Pharmacies, Others) |

Vietnam Healthcare Market Driver:

Rising Prevalence of Non-Communicable Diseases

The rising prevalence of noncommunicable diseases (NCDs) in Vietnam is the foremost structural driver expanding the healthcare market. Urbanization, dietary changes, and lifestyle-related risk factors have intensified incidence rates, stimulating consistent demand for diagnostics, hospital care, and specialized treatment services.

NCDs structurally increase healthcare utilization across institutional and community segments. Patients with chronic illnesses require frequent outpatient consultations, long-term medication, laboratory monitoring, and hospitalization for acute episodes, creating sustained service volumes. The Ministry of Health reports that earlier estimates indicated that approximately 15 million individuals in Vietnam were living with hypertension and diabetes ; however, it is important to note that this figure reflects the prevalence of these conditions rather than actual annual hospital visits or healthcare service utilization. This multi-level requirement ensures that NCD-driven demand affects nearly all segments of the healthcare system rather than a single service line.

Government initiatives amplify this driver by integrating NCD management into national policy frameworks. Vietnam’s newly adopted Law on Disease Prevention includes provisions that require organizing early detection, counseling, monitoring, and preventive treatment for persons at risk of noncommunicable diseases in the community, showing official emphasis on systematic prevention and early management. This demonstrates government policy directly targeting structural NCD control. Coverage ensures financial access to chronic care, enabling regular monitoring and adherence to long-term treatment plans. This structural alignment of disease prevalence, policy support, and financial coverage creates a durable expansion of healthcare service volume, reinforcing NCDs as a systemic and high-impact driver of Vietnam’s healthcare market growth.

Vietnam Healthcare Market Trend:

Digital Transformation and Technology‑Driven Healthcare Delivery

Vietnam’s healthcare market is undergoing a sustained structural shift toward digital transformation, driven by government policy, nationwide systems modernization, and systemic adoption of digital technologies. The Ministry of Health’s Decision No. 4048/QD‑BYT established shared platforms for electronic health records and remote medical consultation, resulting in over 34 million electronic health records created across the national VNeID platform and widespread hospital information system deployment. This shift reflects a broader policy focus on digital health as a core component of national health modernization.

This trend is reshaping industry practices and operating models across the healthcare value chain. Collaboration between the Ministry of Health, United Nations Development Programme (UNDP), and international partners has accelerated telehealth adoption, with remote consultation pilots expanding to commune health stations in multiple provinces, strengthening primary and community‑level care.

The digital transformation trend is persistent due to sustained government commitment, integration of national ID systems with healthcare data, and the scalability of digital platforms. Ongoing policy frameworks position digital health not as a temporary response to capacity challenges but as a systemic platform for long‑term health service delivery reform. Continued adoption of electronic records, telemedicine, and AI‑enabled tools is expected to underpin future improvements in quality, access, and operational efficiency, influencing how healthcare services are accessed and delivered throughout Vietnam’s healthcare system.

Vietnam Healthcare Market Opportunity:

Expansion of Tier‑2 and Rural Healthcare Infrastructure

Vietnam’s strategic healthcare network planning from 2025 to 2030 presents a compelling entry opportunity for new players to invest in tier‑2 (provincial and district) and rural healthcare infrastructure, driven by government priorities to expand equitable access and modernize capacity beyond major urban centers. Under Decision No. 201/QD‑TTg, the national healthcare facility network strategy mandates investments to standardize and strengthen infrastructure across regions, addressing service disparities and aligning facility development with demographic and care needs.

This opportunity translates into tangible demand because the Government has committed to prioritizing physical infrastructure, equipment, and human resources at the commune‑level and grassroots facilities to enhance service availability and reduce overconcentration in central hospitals.

For example, Ho Chi Minh City’s USD 2.5 billion healthcare investment program (2026‑2030) includes 100 new projects, featuring multiple major hospitals such as a tropical disease hospital and a hi‑tech screening center, reflecting large‑scale infrastructure expansion beyond traditional urban core facilities. Expansion of secondary facilities of major hospitals, e.g., Tu Du Hospital’s second facility in Can Gio and the second branch of Gia Dinh People’s Hospital, is being developed to deliver specialized and general healthcare closer to communities, reducing travel burdens for suburban and rural populations, illustrating how infrastructure investment is spatially diversifying service delivery. New and smaller entrants are uniquely positioned to capitalize because existing incumbent providers have historically focused on urban tertiary care, leaving smaller towns and rural districts underserved. Provincial initiatives like those in Thai Binh are investing heavily in regional infrastructure, including the enhancement of general hospitals, eye hospitals, and increased communal health stations, to raise service capacity and bed ratios in the region.

The structural policy mandate to mobilize diverse capital and encourage participation from non‑state economic sectors in facility construction and service provision lowers barriers for agile investors, construction partners, and healthcare service operators to differentiate through targeted infrastructure projects that deliver measurable improvements in care access and utilization across the country.

Vietnam Healthcare Market Challenge:

Shortage of Skilled Workforce

Vietnam’s healthcare system is constrained by a persistent shortage of highly qualified medical professionals, particularly nurses and specialized clinicians, which undermines service delivery and system efficiency. The Ministry of Health estimates that approximately 150,000 nurses are currently in practice, falling well short of the around 260,000 needed to meet p opulation needs, leaving significant gaps in frontline care capacity and workforce sustainability. This shortfall is compounded by regional imbalances and inadequate numbers of well‑trained staff to manage complex clinical services.

The workforce deficit measurably impacts operational performance and patient care quality across health facilities. Major urban hospitals experience difficulty recruiting nurses with advanced expertise, forcing facilities to operate below desired staffing levels despite rising patient volumes, while rural and district‑level facilities remain especially understaffed. Healthcare workers are also leaving public sector roles due to workload pressures and limited incentives, with thousands of resignations reported in recent policy discussions that underline retention challenges.

This structural constraint restricts market growth by limiting the sector’s ability to expand service capacity, adopt advanced clinical technologies, and deliver preventive and chronic care at scale. Without sufficiently skilled personnel, investments in new infrastructure or digital health platforms cannot be fully operationalized, slowing adoption rates and investment returns.

Strengthening education pathways, enhancing professional training standards, and introducing targeted retention incentives are essential to overcoming this fundamental bottleneck to long‑term healthcare market expansion.

Vietnam Healthcare Market Epidemiology Profile:

Cardiovascular Diseases:

Cardiovascular diseases (CVDs) remain the dominant health segment in Vietnam due to their high prevalence among the ageing population and the rising burden of lifestyle-related risk factors such as hypertension, smoking, high-fat diets, and sedentary behavior. According to Vietnam’s Ministry of Health reports, over 31% of deaths are due to some form of CVD, and cardiovascular conditions account for one of the largest shares of hospitalizations in tertiary care centers. The segment’s dominance is reinforced by government investment in specialized cardiology units and national prevention programs emphasizing early detection, awareness, and chronic disease management.

Hospitals and private healthcare providers have increasingly invested in AI-assisted cardiac imaging, catheterization labs, and robotic surgical systems, reflecting growing patient demand for high-quality care and structural support from both public and private financing. National initiatives targeting non-communicable diseases also foster community-based screening and management programs across provinces. For instance, Cho Ray Hospital invested USD 20 million to install a modern interventional cardiac catheterization system, including next‑generation digital subtraction angiography (DSA) suites and supportive hemodynamic devices demonstrating significant capital deployment into CVD infrastructure, International technology and training partnerships such as Medtronic Vietnam’s MoU with Hue Central Hospital help develop clinical skills and adopt advanced cardiovascular technologies (e.g., rhythm management and pacing techniques), reflecting investment flows through training and technology transfer.

The CVD treatment landscape in Vietnam is highly structured, combining hospital-based interventions, outpatient care, and preventive programs. Major hospitals in Hanoi and Ho Chi Minh City perform percutaneous coronary interventions (PCI), coronary artery bypass grafting (CABG), valve repair, heart failure management, and arrhythmia ablation, supported by advanced catheterization labs and imaging technologies. In 2024, Vietnam reported over 40,000 PCI procedures, illustrating procedural capacity expansion. Nationwide campaigns such as the “Healthy Heart Program” offer free blood pressure, glucose, and cholesterol screenings, along with specialist consultations, enhancing early detection and patient engagement .

Cancer:

Cancer is one of the leading health challenges in Vietnam, with liver, lung, and colorectal cancers being the most prevalent among adults. Vietnam records about 180,400 new cancer cases annually and over 120,000 cancer deaths each year, making cancer one of the leading causes of death in the country. Key risk factors include hepatitis infections, smoking, alcohol use, unhealthy diet, and environmental exposures, which together drive both incidence and demand for early diagnosis and specialized care. Population ageing and urbanization further amplify the cancer burden, highlighting the need for effective screening and treatment infrastructure.

Government policy and national health initiatives support cancer detection, treatment, and awareness. Public insurance schemes cover standard chemotherapy, radiotherapy, and surgical procedures, while national programs promote screening campaigns for breast, cervical, liver, and colorectal cancers. Public–private partnerships have facilitated the expansion of oncology centers, and international collaborations support technology transfer and clinical training. Hospitals in Hanoi and Ho Chi Minh City, including the National Cancer Hospital (K Hospital), lead in delivering comprehensive oncology care and integrating research-based treatment protocols.

The treatment landscape combines surgery, radiotherapy, chemotherapy, targeted therapy, and emerging immunotherapy. Major hospitals perform minimally invasive tumor resections, intensity-modulated radiotherapy (IMRT), and molecular-targeted therapies. Immunotherapies such as PD-1 inhibitors are increasingly available in select private and public centers. Community outreach programs provide early detection, awareness, and counseling services, ensuring patient engagement.

For example, Major hospitals such as Vinmec Oncology Center offer a wide range of advanced radiotherapy methods, including Intensity‑Modulated Radiation Therapy (IMRT ), supporting precise tumor targeting and reduced side effects. K Hospital (National Cancer Hospital) has invested in modern radiotherapy equipment (linear accelerators and 4D CT simulation systems) capable of delivering advanced techniques such as IMRT/VMAT , enhancing treatment quality for many cancer types. Oncology clinics in Vietnam provide targeted therapy, which uses drugs tailored to genetic/molecular cancer characteristics, as part of personalized cancer treatment plans.

Gain a Competitive Edge with Our Vietnam Healthcare Market Report:

- The Vietnam Healthcare Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competition, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Vietnam Healthcare Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Introduction

- Executive Summary

- Key Insights

- Key Findings (2020–2024)

- Market Outlook Snapshot (2025–2032F)

- Strategic Imperatives

- Macro Environment Analysis

- Vietnam at a Glance

- Geographic Overview

- Political Structure

- Trade & Regional Alliances

- Others

- Demographic Profile (2020–2032F)

- Population Trends

- Age Structure

- Urban vs Rural Distribution

- Fertility Rate Trends

- Migration Trends

- Ethnic Composition

- Economic Profile (2020–2032F)

- GDP (Current & Constant USD)

- GDP by Sector

- Working Population & Labor Participation

- Per Capita Income & Purchasing Power

- Unemployment & Underemployment

- Inflation Rate & Healthcare Cost Impact

- Foreign Direct Investment Trends

- Country PESTLE Analysis

- Vietnam at a Glance

- Vietnam Healthcare Market Analysis, 2026

- Healthcare System Overview

- Structure of Healthcare System

- Public vs Private Healthcare

- Governance & Regulatory Authorities

- Others

- Healthcare Ecosystem & Infrastructure (2020–2026)

- Healthcare Expenditure

- Healthcare Expenditure as % of GDP

- Per Capita Healthcare Expenditure

- Healthcare Facilities

- Number of Hospitals

- Number of Clinics

- Number of Pharmacies

- Number of Diagnostic Centres

- Public vs Private Distribution

- Bed Availability & Utilization

- Beds per 1,000 Population

- Beds Speciality

- Regional Disparities

- Healthcare Workforce

- Physicians per 1,000 Population

- Physicians by Speciality

- Nurses

- Dentists

- Allied Health Professionals

- Healthcare Expenditure

- Healthcare System Overview

- Health Outcomes & Public Health Indicators (2020–2026)

- Life Expectancy (Male vs Female)

- Infant Mortality Rate

- Maternal Mortality Ratio

- Immunisation Coverage Rates (Measles, DPT, HPV, COVID-19)

- Overall Disease Burden Trends

- Healthcare Reforms & Large-Scale Projects (2020-2026)

- Government Reforms

- Public-Private Partnerships

- Infrastructure Expansion Projects

- Private Sector Investments

- Others

- Insurance Framework

- Public Health Insurance Programs

- Private Health Insurance Market

- Insurance Penetration & Coverage Gaps

- Payer Landscape

- Reimbursement Models (FFS, Bundled, Value-Based Care)

- Claims Management & Transparency Issues

- Out-of-Pocket Expenditure Trends (2020-2026)

- Regulatory Environment (Healthcare Sector)

- Market Authorisation for Pharmaceuticals

- Market Authorisation for Medical Devices

- Licensing for Manufacturing, Import & Export

- Clinical Trial Regulations

- Intellectual Property & Patent Protection

- Advertising, Labeling & Packaging Regulations

- Pharmacy & Hospital Licensing Rules

- Others

- Market Dynamics & Technology

- Healthcare Market Dynamics

- Growth Drivers

- Challenges & Barriers

- Emerging Opportunities

- Value Chain Analysis

- Healthcare Technology Trends

- Digital Health Maturity

- Telemedicine & Remote Monitoring

- Artificial Intelligence & Machine Learning

- Health Apps & Wearables

- Robotic Surgery

- EHR, Data Interoperability & Cybersecurity

- Others

- Healthcare Market Dynamics

- Epidemiology Profile (By Age & By Gender) (2020–2032F)

- Chronic Diseases

- Cardiovascular Diseases

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Diabetes

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Cancer

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Chronic Respiratory Diseases

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Chronic Kidney Disease

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Cardiovascular Diseases

- Infectious Diseases

- Tuberculosis

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- HIV

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Hepatitis

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Others

- Tuberculosis

- Mental Health

- Prevalence of Mental Health Disorders

- Suicide Rates & Trends

- Urban-Rural & Gender Disparities

- Infrastructure Gaps

- Economic & Social Burden

- Chronic Diseases

- Vietnam Healthcare Market Stakeholders Analysis, 2026

- Vietnam Pharmaceutical Market Outlook (2020–2030F)

- Market Size & Growth

- Market Size (USD Million), 2020-2030F

- Market by Key Segments

- Prescription vs OTC

- Generics vs Branded

- Therapeutic Category Distribution

- Manufacturing Landscape

- Distribution & Supply Chain

- Major Distributors

- Major Suppliers

- Major Local and Multinational Players

- Pharmaceutical sector (Top 5–10 companies, % market share)

- Imports & Exports (Value in USD Million) (2020-2026)

- Key Pharmaceutical Clusters (if there)

- Investments and R&D (2020-2026)

- Others

- Market Size & Growth

- Vietnam Medical Devices Market Outlook (2020–2030F)

- Market Size & Growth

- Market Size (USD Million), 2020-2030F

- Market by Key Segments

- By Device Type

- By Risk Class

- By End-User

- Manufacturing Landscape

- Distribution & Supply Chain

- Distributors

- Supply Chain

- Major Local and Multinational Players

- Medical Devices Sector (Top 5–10 companies, % market share)

- Imports & Exports (Value in USD Million) (2020-2026)

- Key Medical Device Clusters (if there)

- Investments and R&D (2020-2026)

- Others

- Market Size & Growth

- Vietnam Pharmaceutical Market Outlook (2020–2030F)

- Vietnam Strategic & Investments in Healthcare Outlook (2025-2032F)

- High-Growth Segments

- Foreign Investment Opportunities

- Government Incentives & Ease of Doing Business

- Risk Assessment & Mitigation

- Trade Associations & Industry Bodies

- Pharmaceutical Associations

- Medical Device Associations

- Healthcare Provider Associations

- Regulatory & Standards Bodies

- Healthcare Trade Fairs & Conferences (2024–2026)

- National Healthcare Exhibitions

- Medical Technology Events

- Pharmaceutical Conferences

- Regional Latin America Events Relevant to Vietnam

- Impact of Global Health Events

- COVID-19 Impact (2020–2022)

- Post-Pandemic Recovery

- Emergency Preparedness Evolution

- Strategic Recommendations

- Market Entry Strategy

- Partnership Models

- Pricing Strategy

- Regulatory Navigation

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now