UAE Healthcare Market Research Report: Growth Drivers & Forecast (2026-2032)

By Healthcare Expenditure Type (Public Healthcare Expenditure, Private Healthcare Expenditure, Out-of-Pocket Expenditure), By Pharmaceutical Segment (Prescription Drugs, Over-the-C ... ounter (OTC) Drugs, Generic Drugs, Branded Drugs, Biologics & Biosimilars), By Therapeutic Area (Cardiovascular Diseases, Oncology, Diabetes, Respiratory Diseases, Neurology, Infectious Diseases, Others), By Medical Device Type (Diagnostic Imaging Devices, Patient Monitoring Devices, Surgical Equipment, In-vitro Diagnostics, Orthopedic Devices, Cardiovascular Devices, Others), By Technology Type (Artificial Intelligence in Healthcare, Telemedicine & Remote Monitoring, Electronic Health Records (EHR), Healthcare Analytics, Robotic Surgery, Wearables & Health Apps), By Healthcare Workforce (Physicians, Nurses, Dentists, Allied Health Professionals), By Insurance Type (Public Health Insurance, Private Health Insurance), By Disease Category (Chronic Diseases, Infectious Diseases, Mental Health Disorders), By End User (Hospitals, Clinics, Diagnostic Centers / Laboratories, Ambulatory Surgical Centers, Home Healthcare, Research Institutes, Pharmacies, Others) Read more

- Healthcare

- Mar 2026

- Pages 150

- Report Format: PDF, Excel, PPT

UAE Healthcare Market

Projected 10% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 3.74 Billion

Market Size (2032)

USD 6.63 Billion

Base Year

2025

Projected CAGR

10%

Leading Segments

By Therapeutic Area: Cardiovascular Diseases

UAE Healthcare Market Report Key Takeaways:

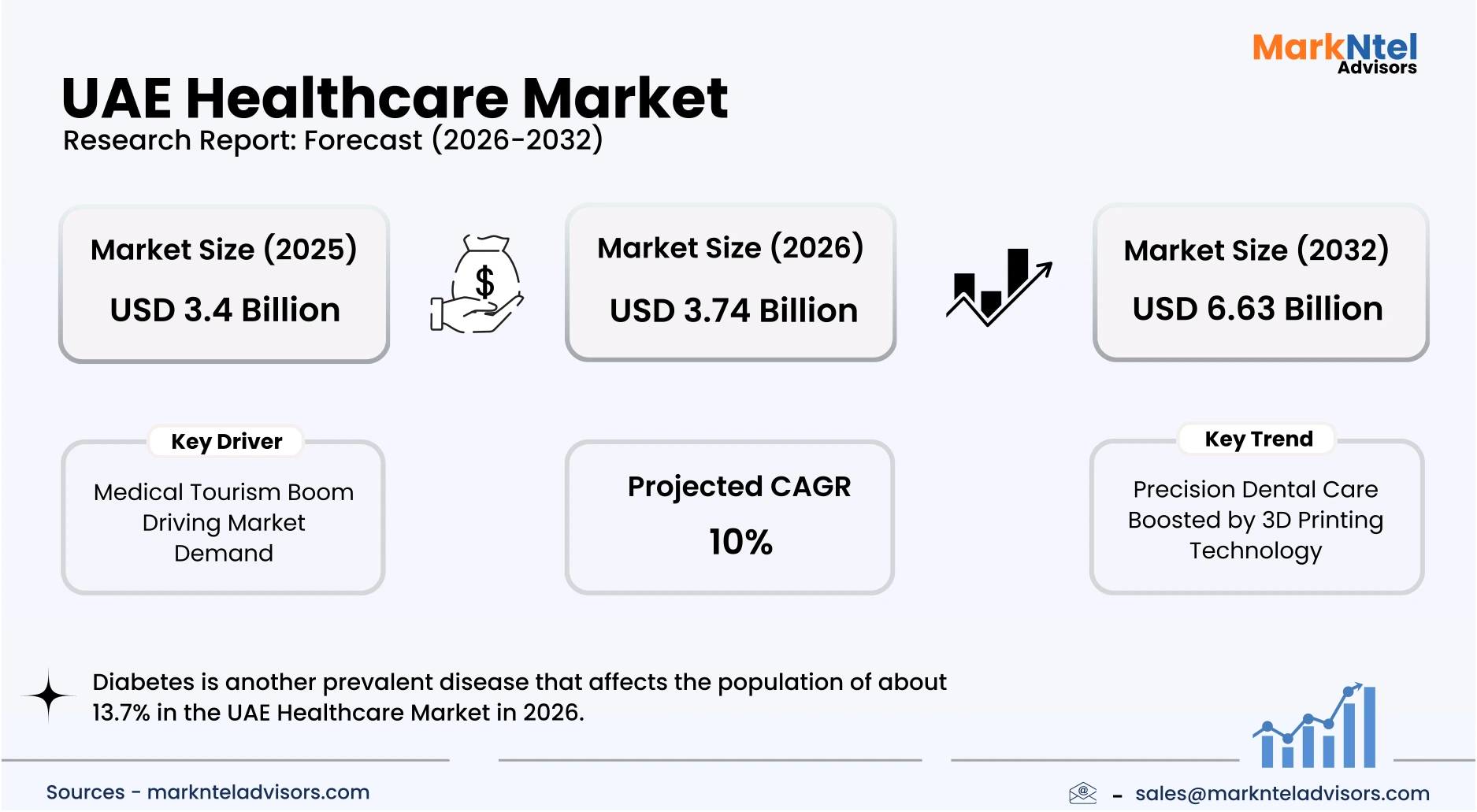

- The UAE Healthcare Market size was valued at USD 3.4 billion in 2025 and is projected to grow from USD 3.74 billion in 2026 to USD 6.63 billion by 2032, exhibiting a CAGR of 10% during the forecast period.

- About 11.5% patients in the UAE healthcare market are affected by cardiovascular diseases in 2026.

- Diabetes is another prevalent disease that affects the population of about 13.7% in the UAE Healthcare Market in 2026.

- The UAE healthcare system comprises over 170 hospitals and approximately 18,500 hospital beds nationwide, supported by more than 34,000 physicians and nearly 68,000 nurses, reflecting a well-developed healthcare infrastructure.

Market Insights & Analysis: UAE Healthcare Market (2026-32):

The UAE Healthcare Market size was valued at USD 3.4 billion in 2025 and is projected to grow from USD 3.74 billion in 2026 to USD 6.63 billion by 2032, exhibiting a CAGR of 10% during the forecast period, i.e., 2026-32.

The UAE Healthcare Market has demonstrated measurable expansion in infrastructure and service capacity, supported by government strategic planning and demographic demand. According to the latest official health statistics, the country operated 173 hospitals and 6,854 health centers across public and private providers, r eflecting extensive facility coverage in relation to population growth. An official report noted that the number of hospitals in Dubai doubled over the past seven years, reaching approximately 55 hospitals in the city by late 2025, reflecting ongoing expansion in response to rising demand from residents and visitors.

Chronic and genetically‑linked diseases are shaping care demand, with non-communicable conditions such as cardiovascular disorders, diabetes, and cancer accounting for significant disease burdens and influencing service planning. The Department of Health Abu Dhabi announced that the Emirati Genome Programme has collected over 800,000 genetic samples from citizens as of late 2025, reinforcing the UAE’s focus on precision and preventive healthcare. This initiative is described as one of the largest population-wide genomic projects in the region and is positioning the UAE as a leader in personalized medicine and longevity research. Government newborn screening guidelines also aim to detect rare hereditary conditions soon after birth, further expanding diagnostic reach. Department of Health Abu Dhabi launched one of the world’s most comprehensive newborn genetic screening programmes in 2025, offering whole‑genome sequencing to screen for over 815 treatable childhood genetic conditions at key hospitals in the emirate. This initiative integrates genomic and AI tools to enhance early diagnosis and improve long-term health outcomes for newborns in the UAE.

Healthcare policy and regulatory frameworks enacted in 2025–2026 have directly influenced market expansion by reducing operational barriers and enhancing digital interoperability. A nationwide unified digital licensing platform is being implemented to streamline credentialing for more than 200,000 healthcare professionals, improving workforce distribution across the emirates. AI governance and health information exchange mandates also require facilities to meet cybersecurity and data quality standards before deploying new technologies, fostering a secure and regulated growth environment. Expanded mandatory insurance coverage across northern emirates has widened access to services, increasing utilization of both primary and specialized care.

Industry participation and technology investment by both public and private stakeholders are accelerating innovation adoption and service modernization. Strategic partnerships between health authorities and technology firms have supported AI-enabled early detection tools for chronic conditions such as diabetes and cancer, while large-scale genomic initiatives are positioning the UAE as a life sciences hub for future therapeutics. End‑user segments, including institutional clients (hospitals and clinics), commercial insurers, and residential populations, are collectively driving demand for advanced digital health platforms, telemedicine services, and precision diagnostics. These integrated efforts are laying the foundation for sustained growth through 2032, with emphasis on quality, accessibility, and outcomes-oriented care delivery.

UAE Healthcare Market Scope:

| Category | Segments |

|---|---|

| By Healthcare Expenditure Type | (Public Healthcare Expenditure, Private Healthcare Expenditure, Out-of-Pocket Expenditure), |

| By Pharmaceutical Segment | (Prescription Drugs, Over-the-Counter (OTC) Drugs, Generic Drugs, Branded Drugs, Biologics & Biosimilars), |

| By Therapeutic Area | (Cardiovascular Diseases, Oncology, Diabetes, Respiratory Diseases, Neurology, Infectious Diseases, Others), |

| By Medical Device Type | (Diagnostic Imaging Devices, Patient Monitoring Devices, Surgical Equipment, In-vitro Diagnostics, Orthopedic Devices, Cardiovascular Devices, Others), |

| By Technology Type | (Artificial Intelligence in Healthcare, Telemedicine & Remote Monitoring, Electronic Health Records (EHR), Healthcare Analytics, Robotic Surgery, Wearables & Health Apps), |

| By Healthcare Workforce | (Physicians, Nurses, Dentists, Allied Health Professionals), |

| By Insurance Type | (Public Health Insurance, Private Health Insurance), |

| By Disease Category | (Chronic Diseases, Infectious Diseases, Mental Health Disorders), |

| By End User | (Hospitals, Clinics, Diagnostic Centers / Laboratories, Ambulatory Surgical Centers, Home Healthcare, Research Institutes, Pharmacies, Others) |

UAE Healthcare Market Driver:

Medical Tourism Boom Driving Market Demand

The rapid expansion of medical tourism has emerged as a primary structural driver significantly augmenting demand in the UAE Healthcare Market. Over 691,000 international patients visited Dubai in recent years, generating healthcare spending exceeding USD 280 million, alongside indirect revenues of approximately USD 627 million. These figures reflect sustained cross-border demand, driven by the UAE’s high-quality clinical services, state-of-the-art infrastructure, and internationally accredited hospitals that attract patients from the Gulf, Europe, and Asia.

This surge in medical tourism is measurably impacting hospital utilization and service uptake across end-user segments, including elective surgeries, specialized diagnostics, and wellness programs. Government initiatives such as DHA’s Health Tourism Strategy 2025 and visa facilitation programs for patients have streamlined access, expanded market reach, and increased occupancy rates in both public and private hospitals. The driver’s effect is geographically broad, benefiting major hubs like Dubai and Abu Dhabi while incentivizing peripheral emirates to enhance specialty services and hospitality-linked healthcare offerings.

Crucially, medical tourism expands market volume rather than merely affecting pricing, as new patient inflows lead to increased service consumption, prolonged hospital stays, and repeated care cycles for chronic and elective conditions. High-income international patients often utilize bundled packages including diagnostics, surgery, and rehabilitation, creating systemic growth in procedural volumes and ancillary services. The structural nature of this driver ensures long-term market expansion, influencing healthcare infrastructure investments, talent recruitment, and specialized service development, thereby establishing a durable foundation for the UAE Healthcare Market growth through 2032.

UAE Healthcare Market Trend:

Precision Dental Care Boosted by 3D Printing Technology

The UAE’s dental sector is increasingly adopting 3D printing technologies to enhance precision in prosthodontics, orthodontics, and implantology. By leveraging 3D‑printed dental models, crowns, and aligners, clinics are able to reduce procedure times, improve fit accuracy, and minimize patient discomfort, creating measurable improvements in care quality. Facilities such as Dubai Dental Clinic and American Dental Clinic Abu Dhabi have integrated in-house 3D printing labs to accelerate treatment planning and delivery.

This technological adoption addresses rising patient demand for customized, efficient, and high-quality dental solutions, particularly among the expatriate population seeking advanced aesthetic and corrective procedures. Regulatory alignment with MOHAP standards ensures that 3D‑printed devices meet strict quality and safety protocols, encouraging wider acceptance among private and public dental providers. For example, Smile Design Dental Laboratory in Dubai describes the use of advanced CAD/CAM systems and 3D printers to deliver precision dental restorations and efficient digital workflows for implant restorations, crowns, and orthodontic appliances.

Smaller dental practices and emerging startups benefit from lower entry costs for 3D printing equipment and access to cloud-based CAD/CAM platforms, enabling them to compete with established clinics on service quality and speed. For instance, Digital Dental Lab in the UAE accepts digital impressions and uses CAD/CAM plus 3D printing workflows to produce crowns, bridges, veneers, implants, and surgical guides with high precision for clinics. This s hows real adoption of digital workflows and additive manufacturing in dental restorations. The combination of precision, regulatory support, and scalable deployment positions 3D printing as a structural opportunity in the UAE dental care market, promoting long-term growth and technological differentiation.

UAE Healthcare Market Opportunity:

Rising Pharmaceutical and Biotech Production Hub

The UAE presents a compelling opportunity for new entrants in pharmaceuticals and biotech, driven by government initiatives supporting local manufacturing, research, and distribution. Incentives such as the Dubai Science Park licensing benefits, Abu Dhabi’s healthcare manufacturing zones, and reduced import tariffs for active pharmaceutical ingredients (APIs) create a favorable environment for startups and SMEs to establish production facilities. These policies align with national strategies to enhance self-sufficiency and regional export capacity.

Tangible market demand is supported by the UAE acting as a regional distribution hub for the Gulf Cooperation Council (GCC), importing and exporting essential medicines while serving hospitals, clinics, and pharmacies nationwide. Partnerships and strategic MoUs, e.g., Globalpharma signed four agreements in 2025, aim to bolster local manufacturing, technology transfer, and access to biosimilars and OTC products, reinforcing the UAE’s role as a regional pharmaceutical hub. The government’s push for biosimilars, vaccines, and specialty drugs creates room for niche players to innovate with localised production or contract manufacturing, particularly in oncology, cardiology, and chronic disease treatment. The UAE’s pharmaceutical sector is described as poised to become a global hub with domestic value exceeding USD 4 billion and projected to rise further, driven by investments in manufacturing, innovation, and quality controls.

The UAE’s biotech sector is emerging as a strategic frontier for innovation, driven by government-backed research initiatives, specialized life sciences ecosystems, and growing demand for advanced therapies and precision medicine. For example, Health X accelerator, launched by start AD and the Department of Health – Abu Dhabi, this Programme is designed to bring 30 global life sciences startups into Abu Dhabi’s biotech ecosystem over two years , advancing cutting-edge research and commercialization. Supportive regulatory pathways, public-private collaborations, and investment in biotech research centers provide a structurally favorable environment for scaling operations and gaining a competitive edge in the GCC region.

UAE Healthcare Market Challenge:

Skilled Workforce Shortage Impeding Market Growth

A critical challenge in the UAE Healthcare Market is the uneven distribution of facilities and services, heavily concentrated in Dubai and Abu Dhabi, while the Northern Emirates have fewer hospitals, specialized clinics, and diagnostic centers. This geographic imbalance restricts patient access to high-quality care and limits the reach of advanced medical interventions.

Compounding this issue is the shortage of skilled healthcare professionals, including physicians, nurses, and technicians, particularly in northern regions. Smaller hospitals and clinics struggle to recruit and retain talent, affecting service delivery, adoption of advanced diagnostics, and implementation of innovative treatments. Operational inefficiencies arise from high reliance on travel for specialized staff and uneven coverage. The UAE’s physician and nurse density is about 2.9 and 6.4 per 1,000 people, respectively, which is below many developed systems and reflects ongoing workforce limitations that affect service delivery capacity. Forecasts show a projected shortfall of approximately 15,000 nurses and allied health professionals in Abu Dhabi alone by 2030, and 6,000 physicians plus 11,000 nurses are needed in Dubai due to growing demand, underscoring the scale of staffing gaps.

Workforce limitations restrict nationwide market expansion, slowing technology adoption and increasing operational costs for providers. Government initiatives, including regional hospital expansions, telemedicine programs, and professional training incentives, are underway, but structural gaps persist, continuing to pose significant barriers for both established players and new entrants.

UAE Healthcare Market Epidemiology Profile:

Cardiovascular Diseases:

Cardiovascular diseases (CVD) maintain dominance in the UAE due to the country’s high prevalence of metabolic risk factors, including obesity and hypertension among adults. A health screening analysis found 11.5% of participants had a high cardiovascular risk , and modifiable risk factors like obesity and inactivity were common. Rapid urbanization, sedentary lifestyles, and dietary shifts have materially elevated incidence rates over the past decade. Government health surveillance and national screening programs have improved detection, revealing that a substantial share of the adult population is at elevated cardiovascular risk. Cardiovascular diseases account for about 34% of all deaths in the UAE , making them a major mortality driver among non-communicable diseases.

Policy prioritization through national non-communicable disease strategies has driven targeted funding for prevention and early intervention, attracting significant investment from both public and private healthcare sectors. These include cardiovascular clinics, advanced diagnostic infrastructure, and chronic care pathways, reinforcing economic flows into CVD management. End-user demand for specialized cardiac care and lifestyle medicine has grown, prompted by rising health awareness and insurance coverage expansion.

Hospitals across the UAE are investing in advanced cardiac care facilities with cutting-edge technology, including comprehensive cardiac programmes that span prevention, early detection, intervention, and rehabilitation, demonst rating infrastructure commitment to cardiovascular health. Policy incentives, such as screening subsidies and employer wellness programs, underpin long-term management and treatment adherence. Together, these factors converge to solidify CVD as the leading chronic condition with robust structural, financial, and demand-driven support across the UAE healthcare landscape.

Diabetes:

Diabetes remains one of the most pervasive chronic health conditions in the UAE. National survey data show 13.7% of UAE adults reported diabetes , and a notable share also had hypertension. Incidence rates continue to rise among younger age groups due to shifts in diet and physical activity, making diabetes a sustained public health priority. Mortality associated with diabetes‑related complications reinforces its epidemiological significance.

Government frameworks, such as strategic non-communicable disease plans, mandate national screening, early diagnosis, and integrated care models, channeling policy momentum toward diabetes management. These policies have catalyzed substantial investment flows into specialized diabetes clinics, patient education programs, and digital self-management tools, supporting clinical outcomes and reducing long-term burden. Private sector engagement is high, driven by rising demand for continuous glucose monitoring and insulin therapy solutions.

End‑user demand characteristics include preference for preventive care, chronic disease management, and personalized treatment plans, shaping market expansion and product availability. Health insurance reforms that improve the affordability of diabetes care further amplify sustained dominance by enhancing access to medications and allied health services. In the UAE, diabetes care goes beyond basic treatment to include structured national screening and follow-up programs. For example, the Ministry of Health and Prevention (MoHAP) has launched a nationwide diabetes and pre‑diabetes screening campaign that links detection with immediate access to consultations, lifestyle coaching, and treatment referrals.

Gain a Competitive Edge with Our UAE Healthcare Market Report:

- The UAE Healthcare Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competition, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The UAE Healthcare Market Landscape Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Introduction

- Executive Summary

- Key Insights

- Key Findings (2020–2024)

- Market Outlook Snapshot (2025–2032F)

- Strategic Imperatives

- Macro Environment Analysis

- UAE at a Glance

- Geographic Overview

- Political Structure

- Trade & Regional Alliances

- Others

- Demographic Profile (2020–2032F)

- Population Trends

- Age Structure

- Urban vs Rural Distribution

- Fertility Rate Trends

- Migration Trends

- Ethnic Composition

- Economic Profile (2020–2032F)

- GDP (Current & Constant USD)

- GDP by Sector

- Working Population & Labor Participation

- Per Capita Income & Purchasing Power

- Unemployment & Underemployment

- Inflation Rate & Healthcare Cost Impact

- Foreign Direct Investment Trends

- Country PESTLE Analysis

- UAE at a Glance

- UAE Healthcare Market Analysis, 2026

- Healthcare System Overview

- Structure of Healthcare System

- Public vs Private Healthcare

- Governance & Regulatory Authorities

- Others

- Healthcare Ecosystem & Infrastructure (2020–2026)

- Healthcare Expenditure

- Healthcare Expenditure as % of GDP

- Per Capita Healthcare Expenditure

- Healthcare Facilities

- Number of Hospitals

- Number of Clinics

- Number of Pharmacies

- Number of Diagnostic Centres

- Public vs Private Distribution

- Bed Availability & Utilization

- Beds per 1,000 Population

- Beds Specialty

- Regional Disparities

- Healthcare Workforce

- Physicians per 1,000 Population

- Physicians by Specialty

- Nurses

- Dentists

- Allied Health Professionals

- Healthcare Expenditure

- Healthcare System Overview

- Health Outcomes & Public Health Indicators (2020–2026)

- Life Expectancy (Male vs Female)

- Infant Mortality Rate

- Maternal Mortality Ratio

- Immunization Coverage Rates (Measles, DPT, HPV, COVID-19)

- Overall Disease Burden Trends

- Healthcare Reforms & Large-Scale Projects (2020-2026)

- Government Reforms

- Public-Private Partnerships

- Infrastructure Expansion Projects

- Private Sector Investments

- Others

- Insurance Framework

- Public Health Insurance Programs

- Private Health Insurance Market

- Insurance Penetration & Coverage Gaps

- Payer Landscape

- Reimbursement Models (FFS, Bundled, Value-Based Care)

- Claims Management & Transparency Issues

- Out-of-Pocket Expenditure Trends (2020-2026)

- Regulatory Environment (Healthcare Sector)

- Market Authorisation for Pharmaceuticals

- Market Authorisation for Medical Devices

- Licensing for Manufacturing, Import & Export

- Clinical Trial Regulations

- Intellectual Property & Patent Protection

- Advertising, Labeling & Packaging Regulations

- Pharmacy & Hospital Licensing Rules

- Others

- Market Dynamics & Technology

- Healthcare Market Dynamics

- Growth Drivers

- Challenges & Barriers

- Emerging Opportunities

- Value Chain Analysis

- Healthcare Technology Trends

- Digital Health Maturity

- Telemedicine & Remote Monitoring

- Artificial Intelligence & Machine Learning

- Health Apps & Wearables

- Robotic Surgery

- EHR, Data Interoperability & Cybersecurity

- Others

- Healthcare Market Dynamics

- Epidemiology Profile (By Age & By Gender) (2020–2032F)

- Chronic Diseases

- Cardiovascular Diseases

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Diabetes

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Cancer

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Chronic Respiratory Diseases

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Chronic Kidney Disease

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Cardiovascular Diseases

- Infectious Diseases

- Tuberculosis

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- HIV

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Hepatitis

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Others

- Tuberculosis

- Mental Health

- Prevalence of Mental Health Disorders

- Suicide Rates & Trends

- Urban-Rural & Gender Disparities

- Infrastructure Gaps

- Economic & Social Burden

- Chronic Diseases

- UAE Healthcare Market Stakeholders Analysis, 2026

- UAE Pharmaceutical Market Outlook (2020–2030F)

- Market Size & Growth

- Market Size (USD Million), 2020-2030F

- Market by Key Segments

- Prescription vs OTC

- Generics vs Branded

- Therapeutic Category Distribution

- Manufacturing Landscape

- Distribution & Supply Chain

- Major Distributors

- Major Suppliers

- Major Local and Multinational Players

- Pharmaceutical sector (Top 5–10 companies, % market share)

- Imports & Exports (Value in USD Million) (2020-2026)

- Key Pharmaceutical Clusters (if there)

- Investments and R&D (2020-2026)

- Others

- Market Size & Growth

- UAE Medical Devices Market Outlook (2020–2030F)

- Market Size & Growth

- Market Size (USD Million), 2020-2030F

- Market by Key Segments

- By Device Type

- By Risk Class

- By End-User

- Manufacturing Landscape

- Distribution & Supply Chain

- Distributors

- Supply Chain

- Major Local and Multinational Players

- Medical Devices Sector (Top 5–10 companies, % market share)

- Imports & Exports (Value in USD Million) (2020-2026)

- Key Medical Device Clusters (if there)

- Investments and R&D (2020-2026)

- Others

- Market Size & Growth

- UAE Pharmaceutical Market Outlook (2020–2030F)

- UAE Strategic & Investments in Healthcare Outlook (2025-2032F)

- High-Growth Segments

- Foreign Investment Opportunities

- Government Incentives & Ease of Doing Business

- Risk Assessment & Mitigation

- Trade Associations & Industry Bodies

- Pharmaceutical Associations

- Medical Device Associations

- Healthcare Provider Associations

- Regulatory & Standards Bodies

- Healthcare Trade Fairs & Conferences (2024–2026)

- National Healthcare Exhibitions

- Medical Technology Events

- Pharmaceutical Conferences

- Regional Latin America Events Relevant to the UAE

- Impact of Global Health Events

- COVID-19 Impact (2020–2022)

- Post-Pandemic Recovery

- Emergency Preparedness Evolution

- Strategic Recommendations

- Market Entry Strategy

- Partnership Models

- Pricing Strategy

- Regulatory Navigation

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now