Global Sovereign Cloud Market Research Report: Forecast (2026-2032)

Sovereign Cloud Market - By Component (Solution, Services), By Deployment Type (Cloud-Based Sovereign Cloud, On-Premises Sovereign Cloud), By Cloud Type (Infrastructure-as-a-Servic ... e (IaaS), Platform-as-a-Service (PaaS), Software-as-a-Service (SaaS)), By Sovereignty Type (Data Sovereignty, Operational Sovereignty, Technical Sovereignty), By Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)), By End-Use Industry (Government & Defense, Banking, Financial Services & Insurance (BFSI), Healthcare & Life Sciences, Telecommunications, Energy & Utilities, Manufacturing, Others), and others Read more

- ICT & Electronics

- Feb 2026

- Pages 400

- Report Format: PDF, Excel, PPT

Global Sovereign Cloud Market

Projected 24.16% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 156.2 Billion

Market Size (2032)

USD 572.3 Billion

Largest Region

North America

Projected CAGR

24.16%

Leading Segments

By End-Use Industry: Government & Defense

Global Sovereign Cloud Market Report Key Takeaways:

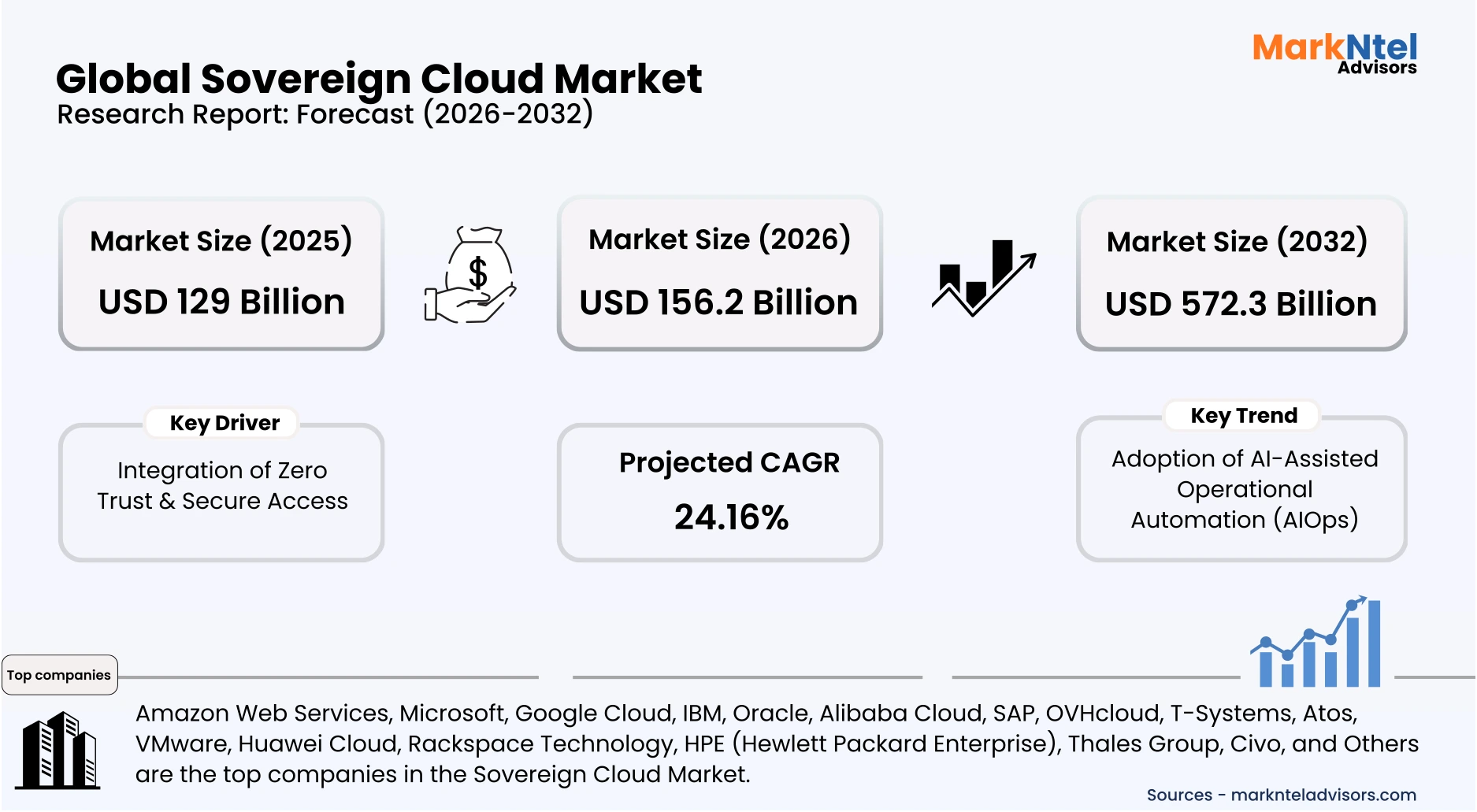

- Market size was valued at around USD 129 billion in 2025 and is projected to grow from USD 156.2 billion in 2026 to USD 572.3 billion by 2032. The estimated CAGR from 2026 to 2032 is around 24.16%, indicating strong growth.

- North America holds the largest market share of about 44% in the Global Sovereign Cloud Market in 2026.

- By Sovereignty Type, the Data Sovereignty segment represented a significant share of about 55% in the Global Sovereign Cloud Market in 2026.

- By End-User, the Government & Defense segment presented a significant share of about 32% in the Global Sovereign Cloud Market in 2026.

- Leading Sovereign Cloud Companies in the Global Market are Amazon Web Services, Microsoft, Google Cloud, IBM, Oracle, Alibaba Cloud, SAP, OVHcloud, T-Systems, Atos, VMware, Huawei Cloud, Rackspace Technology, HPE (Hewlett Packard Enterprise), Thales Group, Civo, and Others.

Market Insights & Analysis: Global Sovereign Cloud Market (2026-32):

The Sovereign Cloud Market size was valued at around USD 129 billion in 2025 and is projected to grow from USD 156.2 billion in 2026 to USD 572.3 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 24.16% during the forecast period, i.e., 2026-32.

The growth is fundamentally anchored in the shift from voluntary cloud adoption to regulation-led infrastructure mandates. Governments are no longer treating cloud as a technology choice but as a compliance-controlled asset, requiring that sensitive public data be hosted on platforms guaranteeing national legal jurisdiction, administrator residency, and domestic encryption-key ownership. These requirements are structurally favoring sovereign cloud deployments over conventional public cloud models.

As these mandates are codified into procurement rules, regulatory intent is translating directly into public-sector spending. The European Commission launched a USD209 million sovereign cloud services procurement tender in 2025 for EU institutions and agencies, indicating growing public-sector spending tied to sovereign cloud compliance and infrastructure requirements . Additionally, initiatives such as France’s Cloud de Confiance and Germany’s sovereign IT guidelines have reinforced this shift by systematically excluding non-sovereign cloud deployments from sensitive workloads, thereby locking sovereign compliance into long-term public IT modernization plans.

These procurement-driven requirements are, in turn, reshaping investment behavior across the cloud ecosystem. Sovereign cloud implementation necessitates country-specific data centers, locally incorporated operating entities, and restricted administrative access, materially increasing capital intensity compared to standardized hyperscaler regions. To meet these conditions, providers are accelerating localized infrastructure build-outs. For reference, OVHcloud expanded EU-based sovereign data-center capacity in 2025 , while T-Systems scaled sovereign environments powered by Google Cloud, integrating hyperscaler capabilities with locally governed operations to satisfy jurisdictional controls.

Crucially, the impact of these investments extends beyond government. As sovereign cloud platforms mature, compliance requirements are cascading into regulated private sectors. BFSI regulators now mandate domestic hosting of transaction and customer data, healthcare authorities require in-country processing of patient records, and telecom regulators enforce national-security oversight of metadata. This regulatory spillover is expanding sovereign cloud adoption across multiple end-use industries, sustaining market growth through 2032.

Global Sovereign Cloud Market Recent Developments:

- 2026: Rackspace Technology announced that its UK Sovereign Services achieved VMware Sovereign Cloud certification, enabling the company to deliver managed sovereign cloud infrastructure that ensures sensitive data remains securely stored, processed, and protected within UK jurisdiction while meeting strict compliance and data sovereignty requirements.

- 2025: Google Cloud continued expanding its sovereign cloud capabilities in partnership with T-Systems, strengthening the “T-Systems Sovereign Cloud powered by Google Cloud” portfolio. The offering enables enterprises and public sector organizations to maintain strict control over data residency, compliance, and operational sovereignty while leveraging Google Cloud infrastructure.

- 2025: Amazon Web Services (AWS) signed a cooperation agreement with Germany’s Federal Office for Information Security (BSI) to strengthen cybersecurity standards and support digital sovereignty initiatives across Germany and the European Union. The collaboration aims to enhance secure cloud infrastructure and ensure compliance with strict regional data protection and sovereignty requirements.

- 2025: Microsoft partnered with Yotta Data Services to integrate Azure AI services into Yotta’s Shakti Cloud, a sovereign AI cloud platform. The initiative is designed to accelerate AI innovation in India by enabling enterprises, startups, and public sector organizations to access advanced AI capabilities within a secure and locally governed cloud environment.

- 2024: SAP SE announced the general availability of its Sovereign Cloud capabilities in the United Kingdom, offering secure and localized cloud solutions designed to meet strict data sovereignty, compliance, and security requirements. The solution is tailored for public sector organizations, critical national infrastructure, and highly regulated industries, enabling them to store and process data within the UK while complying with national data protection regulations and cybersecurity standards.

Global Sovereign Cloud Market Scope:

| Category | Segments |

|---|---|

| By Component | Solution, Services |

| By Deployment Type | Cloud-Based Sovereign Cloud, On-Premises Sovereign Cloud |

| By Cloud Type | Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), Software-as-a-Service (SaaS) |

| By Sovereignty Type | Data Sovereignty, Operational Sovereignty, Technical Sovereignty |

| By Enterprise Size | Large Enterprises, Small & Medium Enterprises (SMEs) |

| By End-Use Industry | Government & Defense, Banking, Financial Services & Insurance (BFSI), Healthcare & Life Sciences, Telecommunications, Energy & Utilities, Manufacturing, Others |

Global Sovereign Cloud Market Driver:

Integration of Zero Trust & Secure Access

The integration of Zero Trust and secure access has emerged as a defining driver in the Global Sovereign Cloud market because governments increasingly demand cloud environments that combine data residency with continuous security enforcement. This shift began structurally when the National Institute of Standards and Technology (NIST) released SP 800-207 in 2020, formally establishing Zero Trust as a government-grade security model built on identity verification, device trust, and least-privilege access. As a result, sovereign cloud procurement frameworks started aligning cloud eligibility with Zero Trust compliance rather than perimeter security alone.

Similarly, the Cybersecurity and Infrastructure Security Agency reinforced this direction through its Zero Trust Maturity Model (2023), accelerating adoption across public-sector cloud workloads. In response, cloud providers began embedding Zero Trust controls directly into sovereign offerings. For instance, Microsoft launched Cloud for Sovereignty in 2022, integrating identity-centric access controls, restricted operator access, and national-partner governance to meet regulatory expectations . Likewise, Google Cloud, through its 2021 partnership with T-Systems, connected Zero Trust identity and access tooling with German jurisdiction cloud operations, directly linking security architecture to legal sovereignty.

More recently, Amazon Web Services announced the European Sovereign Cloud (2026), explicitly positioning Zero Trust, operational autonomy, and controlled access as baseline design principles. These integrations are contributing to the market growth.

Global Sovereign Cloud Market Trend:

Adoption of AI-Assisted Operational Automation (AIOps)

AIOps is emerging as a structural trend in the Global Sovereign Cloud Market as governments scale cloud infrastructure while facing shortages of cleared personnel, rising cyber risks, and strict audit obligations. The shift begins with policy acceptance. Governments now recognize AI not only as an application tool but as an operational enabler for managing sovereign infrastructure. For instance, the Cybersecurity and Infrastructure Security Agency released its AI Roadmap in 2023, explicitly encouraging responsible AI adoption across federal infrastructure to improve monitoring, incident response, and resilience, laying institutional groundwork for AIOps in government clouds.

Moreover, sovereign cloud operators began integrating AI into day-to-day cloud operations rather than user-facing services. Research programs from Microsoft Research (2023–2024) demonstrate tiered AIOps models that automate fault detection, root-cause analysis, and remediation while preserving human approval and audit logs, an approach aligned with sovereign governance requirements . As sovereign clouds expanded in scale, AI-driven automation became necessary to manage complexity without expanding privileged human access.

Global Sovereign Cloud Market Opportunity:

Rising Investments for Data-Center Expansion

Rising investments in nationally governed data-center infrastructure are creating a powerful opportunity for the Global Sovereign Cloud market by expanding jurisdiction-bound capacity required for sovereign hosting. This opportunity becomes most visible where governments align energy policy, infrastructure approvals, and digital-sovereignty objectives, ensuring sensitive data and cloud operations remain under domestic legal control.

This alignment is especially evident in the United States, where accelerating AI adoption has triggered a new wave of large-scale data-center construction. For instance, in 2024–2025, U.S. data-center construction reached record levels as utilities and states approved power-intensive facilities, with several multi-billion-dollar campuses announced across Virginia, Texas, and Arizona to support AI and government workloads under U.S. jurisdiction.

Similarly, India is converting data-localization policies into real infrastructure on the ground. For example, around USD60 billion invested between 2019 and 2024, several large data-center projects were announced or developed during 2024–2025 across key states. These include a USD11 billion, 2.5 GW data-center park in Maharashtra, a USD 6 billion data-center and power campus in Andhra Pradesh, a multi-billion-rupee hyperscale data-center hub in Tamil Nad u, and new AI-focused data-center campuses in Uttar Pradesh.

Together, these projects are rapidly expanding India’s domestic data-center capacity, creating a strong foundation for hosting government, regulated-sector, and AI workloads within national borders, supported by state incentives and power-tariff concessions, directly strengthening India’s ability to host government and regulated-sector cloud services domestically.

In China, investment remains state-directed and strategic. For instance, since 2021, China has poured tens of billions of dollars into new data centers and national computing hubs under government programs, with additional facilities commissioned in western provinces during 2024–2025 to keep cloud and AI workloads fully within Chinese jurisdiction.

Meanwhile, Thailand demonstrates how emerging markets are institutionalizing sovereign capacity. For reference, under the Eastern Economic Corridor, Thailand approved new data-center park projects in 2023–2024, attracting multi-billion-dollar commitments supported by Board of Investment incentives, dedicated power infrastructure, and subsea-cable access, directly enabling sovereign cloud and AI hosting for government and regulated users.

Across Europe, the European Commission continues to link cloud-sovereignty goals with regional infrastructure funding, encouraging member states to commission new locally governed data centers to meet compliant cloud-procurement requirements.

Global Sovereign Cloud Market Challenge:

High Deployment & Establishment Costs

High deployment and establishment costs remain a critical structural challenge constraining the global sovereign cloud market, directly affecting both scalability and geographic expansion. Unlike conventional public cloud models that benefit from centralized hyperscale efficiency, sovereign cloud architectures require country-specific data centers, legally independent operating entities, and segregated governance structures. These requirements significantly erode economies of scale and raise upfront capital commitments.

Large hyperscale data centers typically require capital investments running into several hundred million dollars and can exceed USD1 billion per facility, driven by the need for high-capacity power infrastructure, advanced cooling systems, land acquisition, and grid connectivity. Sovereign cloud models frequently necessitate multiple localized facilities across jurisdictions rather than centralized capacity, driving materially higher per-unit infrastructure costs and extending breakeven timelines.

Beyond capital expenditure, operational costs further intensify the challenge. The EU Agency for Cybersecurity (ENISA) estimates that continuous compliance audits, administrator access-logging, jurisdiction-bound encryption-key management, and sovereign incident-response readiness increase operating expenditure by 20–30% compared with standard cloud deployments. These recurring compliance costs persist throughout the asset lifecycle, not just during deployment.

Global Sovereign Cloud Market (2026-32) Segmentation Analysis:

The Global Sovereign Cloud Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the global level. Based on the analysis, the market has been further classified as;

Based on Sovereignty Type:

- Data Sovereignty

- Operational Sovereignty

- Technical Sovereignty

Data sovereignty dominates the Global Sovereign Cloud Market with a market share of about 55% because it represents the foundational legal requirement upon which operational and technical sovereignty are built. Governments prioritize data sovereignty as the location of data determines jurisdiction, legal authority, and exposure to extraterritorial laws. If public-sector or regulated data is stored outside national or regional boundaries, governments risk losing legal control regardless of the security, governance, or technology applied. For instance, policy frameworks driven by the European Commission require that sensitive public data remain under EU legal jurisdiction, immediately disqualifying cloud environments that do not meet residency requirements.

Once this legal boundary is established, governments extend requirements to operational sovereignty to ensure that cloud operations, such as system administration, access approvals, incident response, and audits, remain subject to domestic oversight. Operational sovereignty, however, is derivative rather than primary; its purpose is to safeguard data that has already been designated as sovereign.

To enforce both legal and operational mandates, governments then rely on technical sovereignty. Controls such as encryption-key ownership, isolated control planes, and restricted administrative access are implemented to technically ensure compliance with policy decisions. Guidance from the National Institute of Standards and Technology reinforces that technical controls are instruments for implementing governance requirements, not substitutes for legal authority.

Based on End-Use Industry:

- Government & Defense

- Banking, Financial Services & Insurance (BFSI)

- Healthcare & Life Sciences

- Telecommunications

- Energy & Utilities

- Manufacturing

- Others

The Government and Defense segment dominates the Global Sovereign Cloud Market by accounting for about 32% because it sits at the intersection of national security, legal authority, and large-scale public expenditure. Governments generate and control the largest volumes of sensitive and high-risk data, including defense intelligence, command-and-control systems, citizen registries, taxation platforms, and critical infrastructure databases. As a result, while public sectors increasingly depend on cloud computing, these workloads cannot operate under foreign jurisdiction, making sovereign cloud infrastructure a strategic requirement rather than a discretionary technology choice.

This dominance is clearly reflected in defense procurement. For instance, the U.S. Department of Defense awarded the Joint Warfighting Cloud Capability (JWCC) contract in 2022, with a ceiling value of USD9 billion, specifically to support classified and unclassified military workloads across multiple security domains . The contract explicitly mandates sovereign control, auditability, and restricted access, illustrating how defense needs directly translate into sovereign cloud demand.

Cybersecurity pressures further reinforce this trend. For reference, NATO reported a significant increase in cyber incidents targeting government and defense systems after 2022, accelerating migration toward cloud platforms with continuous monitoring and tightly controlled operations. This security imperative is backed by funding. For instance, India’s Union Government allocated over USD230 million in 2025 toward defense digitization, cybersecurity, and IT modernization , directly strengthening demand for domestically hosted sovereign cloud infrastructure.

Global Sovereign Cloud Market (2026-32): Regional Projection

North America leads the Global Sovereign Cloud Market with a market share of about 44% due to its unmatched combination of digital infrastructure depth, regulatory-driven demand, and concentration of hyperscale cloud providers. Structurally, the region hosts the world’s largest installed base of hyperscale data centers. For reference, the United States alone accounts for over 40% of global data-center capacity, supported by advanced power grids, high fiber density, and large-scale land availability, enabling faster sovereign cloud deployment than other regions.

Regulatory and policy frameworks strongly reinforce this dominance. In the United States, FedRAMP High, DoD Impact Level (IL) 4–6, and sector-specific mandates require government and defense workloads to be hosted on tightly controlled cloud environments with restricted access, auditability, and domestic jurisdiction. According to the U.S. Government Accountability Office, federal agencies spent over USD100 billion annually on IT, with cloud modernization and security compliance identified as priority areas during 2023–2026.

The region hosts the headquarters and primary operations of Amazon Web Services, Microsoft, Google Cloud, IBM, and Oracle, all of which expanded sovereign-aligned government cloud offerings between 2023 and 2025.

Together, superior infrastructure scale, enforceable compliance regimes, and concentrated high-value end-user demand explain why North America consistently outperforms other regions in sovereign cloud adoption intensity and market size.

Gain a Competitive Edge with Our Global Sovereign Cloud Market Report:

- Global Sovereign Cloud Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Global Sovereign Cloud Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Global Sovereign Cloud Market Policies, Regulations, and Product Standards

- Global Sovereign Cloud Market Trends & Developments

- Global Sovereign Cloud Market Dynamics

- Growth Factors

- Challenges

- Global Sovereign Cloud Market Hotspot & Opportunities

- Global Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- Solution

- Services

- By Deployment Type

- Cloud-Based Sovereign Cloud

- On-Premises Sovereign Cloud

- By Cloud Type

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- Software-as-a-Service (SaaS)

- By Sovereignty Type

- Data Sovereignty

- Operational Sovereignty

- Technical Sovereignty

- By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- By End-Use Industry

- Government & Defense

- Banking, Financial Services & Insurance (BFSI)

- Healthcare & Life Sciences

- Telecommunications

- Energy & Utilities

- Manufacturing

- Others

- By Region

- North America

- South America

- Europe

- The Middle East & Africa

- Asia-Pacific

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Outlook

- North America Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- By Country

- US

- Mexico

- Canada

- Rest of North America

- US Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Mexico Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Canada Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Market Size & Outlook

- South America Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- By Country

- Brazil

- Chile

- Rest of South America

- Brazil Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Chile Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Market Size & Outlook

- Europe Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- By Country

- Germany

- France

- UK

- Poland

- BENELUX

- Rest of Europe

- Germany Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- France Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- UK Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Poland Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- BENELUX Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Market Size & Outlook

- The Middle East & Africa Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- By Country

- UAE

- Saudi Arabia

- Qatar

- Israel

- South Africa

- Kenya

- Nigeria

- Egypt

- Rest of Middle East & Africa

- UAE Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Saudi Arabia Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Qatar Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Israel Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- South Africa Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Kenya Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Nigeria Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Egypt Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Market Size & Outlook

- Asia-Pacific Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- By Country

- China

- Japan

- India

- South Korea

- Indonesia

- Vietnam

- Malaysia

- Australia Rest of Asia-Pacific

- China Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Japan Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- India Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- South Korea Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Indonesia Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Vietnam Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Malaysia Sovereign Cloud Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component

- By Deployment Type

- By Cloud Type

- By Sovereignty Type

- By Enterprise Size

- By End-Use Industry

- Market Size & Outlook

- Market Size & Outlook

- Global Sovereign Cloud Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Amazon Web Services

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Microsoft

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Google Cloud

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IBM

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Oracle

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alibaba Cloud

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SAP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- OVHcloud

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- T-Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Atos

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VMware

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huawei Cloud

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rackspace Technology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HPE (Hewlett Packard Enterprise)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thales Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Civo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amazon Web Services

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now