Saudi Arabia Diagnostic Labs Market Research Report: Forecast (2026-2032)

Saudi Arabia Diagnostic Labs Market - By Test Type (Pathology, Radiology & Imaging), By Pathology Test Type (Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Hi ... stopathology & Cytopathology, Molecular Diagnostics, Genetic Testing), By Radiology Type (X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others), By Service Delivery Mode (Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units), By Disease Type (Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others), By End-User (Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions), and others Read more

- Healthcare

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

Saudi Arabia Diagnostic Labs Market

Projected 5.97% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 1.58 Billion

Market Size (2032)

USD 2.37 Billion

Base Year

2025

Projected CAGR

5.97%

Leading Segments

By End-User: Hospitals

Saudi Arabia Diagnostic Labs Market Report Key Takeaways:

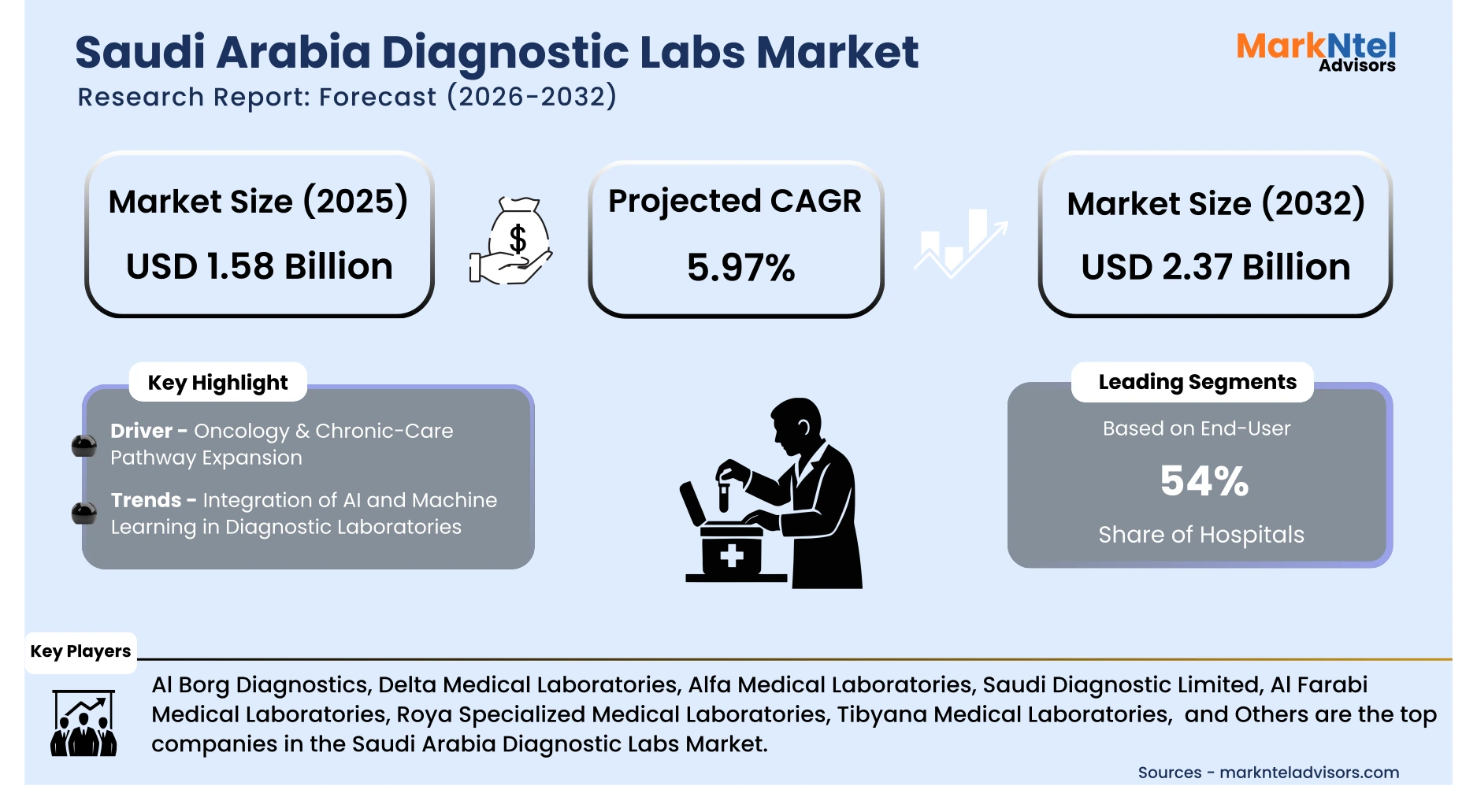

- Market size was valued at around USD1.58 billion in 2025 and is projected to reach USD2.37 billion by 2032. The estimated CAGR from 2026 to 2032 is around 5.97%, indicating strong growth.

- By Radiology Type, the X-Ray segment represented a significant share of about 32% in the Saudi Arabia Diagnostic Labs Market in 2025.

- By End-Use Industry, the hospitals presented a significant share of about 54% in the Saudi Arabia Diagnostic Labs Market in 2025.

- Leading Diagnostic Labs Companies in the Saudi Arabia Market are Al Borg Diagnostics, Delta Medical Laboratories, Alfa Medical Laboratories, Saudi Diagnostic Limited, Al Farabi Medical Laboratories, Roya Specialized Medical Laboratories, Tibyana Medical Laboratories, Al Hyatt Medical Laboratory Company, Al Arab Medical Laboratories, and Others.

Market Insights & Analysis: Saudi Arabia Diagnostic Labs Market (2026-32):

The Saudi Arabia Diagnostic Labs Market size was valued at around USD1.58 billion in 2025 and is projected to reach USD2.37 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 5.97% during the forecast period, i.e., 2026-32.

The Saudi Arabia diagnostic labs market is evolving from fragmented testing units toward integrated, capacity-driven service models, primarily influenced by disease burden and system-level healthcare reforms. For instance, non-communicable diseases account for approximately 73% of total deaths, which directly increases the frequency of diagnostic imaging, follow-up testing, and long-term disease monitoring . This epidemiological reality establishes a structurally high baseline demand for diagnostic services.

Building on this demand foundation, market dynamics are being reshaped by healthcare modernization under Vision 2030, which prioritizes hospital capacity expansion and private-sector participation. As hospitals are upgraded and new facilities commissioned, diagnostic services are increasingly embedded within hospital campuses rather than outsourced. Consequently, diagnostic labs benefit from captive volumes, shorter patient pathways, and higher test conversion rates. This integration strengthens demand predictability and supports long-term capacity planning for lab operators.

Additionally, healthcare infrastructure statistics reinforce this growth trajectory. The presence of 516 hospitals and expanding bed density across regions increases the number of diagnostic touchpoints nationwide. Similarly, rising physician density enhances test referral intensity, particularly for imaging and pathology services. Together, these supply-side expansions amplify diagnostic throughput beyond metropolitan centers, improving regional penetration for organized lab networks.

Moreover, insurance expansion acts as a demand multiplier. As private health-insurance beneficiaries exceeded 13 million, affordability barriers for diagnostics declined, shifting patient behavior toward insured testing and preventive screenings. This transition improves revenue visibility for labs and supports investments in high-CAPEx modalities such as CT and MRI. However, workforce concentration in urban centers introduces operational friction, particularly for advanced imaging utilization in peripheral regions, thereby influencing deployment strategies and reinforcing the relevance of centralized hub models.

Saudi Arabia Diagnostic Labs Market Recent Developments:

- 2024 : The Saudi Food and Drug Authority (SFDA) launched an initiative aimed at developing medical diagnostic laboratory devices and integrating three-dimensional (3D) printing technology within hospitals and medical laboratories.

- 2024 : Saudi Arabia’s SFDA issued MDS-G022 guidance on in-house in vitro diagnostic devices, clarifying requirements for laboratories developing or modifying diagnostic assays, strengthening regulatory compliance, quality standards, and oversight, while encouraging innovation within the Saudi diagnostic laboratories market.

Saudi Arabia Diagnostic Labs Market Scope:

| Category | Segments |

|---|---|

| By Test Type | Pathology, Radiology & Imaging |

| By Pathology Test Type | Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopathology & Cytopathology, Molecular Diagnostics, Genetic Testing |

| By Radiology Type | X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others |

| By Service Delivery Mode | Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units |

| By Disease Type | Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others |

| By End-User | Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions |

Saudi Arabia Diagnostic Labs Market Driver:

Oncology & Chronic-Care Pathway Expansion

The expansion of oncology and chronic-care pathways is a structurally reinforcing driver for diagnostic demand in Saudi Arabia, as these conditions inherently require continuous, multi-stage diagnostics rather than one-time testing. Cancer care, in particular, is diagnostics-intensive across screening, diagnosis, staging, treatment monitoring, and recurrence surveillance. According to the World Health Organization’s GLOBOCAN, Saudi Arabia records over 28,000 new cancer cases annually , a volume that directly translates into repeated imaging, histopathology, and biomarker testing throughout patient lifecycles.

This oncology-led demand is further amplified by the high burden of chronic diseases. As per the International Diabetes Federation, Saudi Arabia had approximately 5.34 million adults living with diabetes in 2024, a condition that requires routine laboratory monitoring and periodic imaging to track complications. Similarly, cardiovascular diseases necessitate recurring diagnostic assessments, reinforcing sustained utilization of laboratory and imaging services.

Moreover, rising caseloads and survivorship extend diagnostic requirements beyond initial treatment phases. As survival rates improve, patients remain within long-term monitoring pathways, increasing cumulative diagnostic volumes per patient. Collectively, the convergence of rising oncology incidence and expanding chronic-care management transforms diagnostics into an indispensable, recurring component of healthcare delivery, thereby driving sustained demand growth across imaging, pathology, and advanced laboratory testing in Saudi Arabia.

Saudi Arabia Diagnostic Labs Market Trend:

Integration of AI and Machine Learning in Diagnostic Laboratories

The integration of artificial intelligence (AI) and machine learning (ML) is emerging as a transformative trend in the Saudi Arabia diagnostic labs market, driven by national digital health priorities and adoption by leading tertiary institutions. Under the national data and AI agenda led by the Saudi Data & AI Authority, healthcare has been identified as a priority sector, enabling structured use of clinical and laboratory data for advanced analytics.

At the institutional level, King Faisal Specialist Hospital & Research Centre has operationalized AI through its Centre for Healthcare Intelligence, deploying machine-learning models across radiology and pathology workflows to improve diagnostic accuracy and reduce interpretation errors. Similarly, King Fahd Medical City has implemented AI-assisted imaging tools to accelerate scan interpretation and prioritize critical cases, directly reducing turnaround times.

Moreover, AI-enabled platforms from Siemens Healthineers and Philips Healthcare are being integrated into hospital PACS, LIS, and pathology systems, enabling automated image analysis, biomarker quantification, and decision support. In parallel, digital pathology solutions using whole-slide imaging and AI-based pattern recognition are enabling remote review and tele-pathology, addressing specialist shortages. These advancements are actively transforming the market.

Saudi Arabia Diagnostic Labs Market Opportunity:

Policy-Backed Expansion of Corporate & Occupational Screening

Saudi Arabia’s corporate-health and occupational diagnostic screening segment is being structurally expanded through coordinated government programs, labor regulations, and population-level health initiatives, creating a durable growth opportunity for diagnostic labs. Under Vision 2030, the Health Sector Transformation Program promotes preventive healthcare as a cost-containment strategy, explicitly integrating routine health assessments into workforce and population health management. This direction is reinforced by national productivity and safety objectives, which link employee health outcomes with economic efficiency and reduced workplace absenteeism.

Beyond policy intent, the government has launched mass diagnosis and early-detection programs that materially increase diagnostic volumes. The Saudi Ministry of Health leads nationwide screening initiatives under the National Transformation Program, including large-scale diabetes, hypertension, obesity, and cancer screening campaigns delivered through primary healthcare centers and employer-linked health drives. These programs rely on standardized laboratory tests, imaging diagnostics, and repeat monitoring, shifting diagnostics from optional testing to structured population coverage.

Operationally, labor regulations convert these programs into enforceable demand. The Ministry of Human Resources and Social Development mandates medical fitness certification for workers in high-risk sectors such as construction, industrial manufacturing, food handling, and healthcare services. These certifications require chest X-ray imaging, complete blood counts, and communicable-disease screening before job placement and during periodic renewals.

Saudi Arabia Diagnostic Labs Market Challenge:

High Initial Investments Impeding Market Growth

High capital intensity acts as a structural barrier to the expansion of diagnostic laboratories in Saudi Arabia, especially as testing shifts toward high-complexity modalities. The adoption of molecular diagnostics, automated clinical chemistry, and digital pathology requires simultaneous investment in analyzers, biosafety infrastructure, and laboratory IT systems, significantly raising entry and scaling costs.

For instance, equipment listings and manufacturer disclosures from suppliers such as Roche Diagnostics, Thermo Fisher Scientific, and Abbott indicate that real-time PCR systems typically range from USD 20,000 to over USD 150,000, while fully automated, high-throughput clinical chemistry analyzers frequently exceed USD 200,000, excluding installation and reagent agreements. Additionally, service, calibration, and preventive maintenance contracts, standard practice in regulated clinical environments, generally account for 8–12% of equipment value annually, increasing long-term ownership costs.

At the same time, capital allocation priorities within the Saudi Ministry of Health emphasize hospital capacity, workforce expansion, and national digital health platforms. Consequently, private diagnostic labs face longer payback periods, delayed technology upgrades, and limited expansion beyond Tier-1 cities, directly moderating nationwide diagnostic capacity growth despite rising demand.

Saudi Arabia Diagnostic Labs Market (2026-32) Segmentation Analysis:

The Saudi Arabia Diagnostic Labs Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Radiology Type:

- X-Ray

- Ultrasound

- CT Scan

- MRI

- Mammography

- PET-CT

- Nuclear Imaging

- Others

X-ray continues to dominate this market in Saudi Arabia with a market share of about 32% because it aligns directly with patient flow patterns, facility capabilities, and clinical decision pathways across the healthcare system. In emergency and outpatient settings, X-ray is the primary imaging modality for suspected fractures, chest infections, postoperative follow-up, and abdominal complaints, allowing clinicians to make rapid treatment decisions without referral delays.

For instance, national hospital service statistics published by the Saudi Ministry of Health show that injuries, respiratory diseases, and musculoskeletal disorders consistently rank among the top causes of hospital visits and admissions, all of which rely predominantly on radiographic evaluation. This demand profile structurally favors high-volume X-ray usage over advanced imaging.

Additionally, Saudi Arabia’s inpatient care model reinforces bedside imaging. Hospitals with large bed capacity routinely deploy mobile X-ray units for ICU patients, surgical wards, and immobile cases, where CT or MRI access is limited by patient condition and logistics. This significantly increases daily radiography volumes within hospitals.

Based on End-User:

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers (IDCs)

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

Hospitals dominate the market by accounting for about 54% because the entire healthcare ecosystem is engineered to originate, process, and retain diagnostic activity within hospital systems. Additionally, the Ministry of Health, which operates hundreds of hospitals, structures care delivery around integrated clinical pathways. As patients move from consultation to diagnosis to treatment within the same facility, laboratory testing remains embedded in hospital workflows to preserve speed, clinical accountability, and data continuity. This integration naturally minimizes diagnostic leakage to stand-alone labs.

Moreover, accreditation mandates from CBAHI require hospitals to maintain on-site laboratory capacity for emergency, ICU, surgical, and inpatient services. Compliance, therefore, compels continuous investment in hospital laboratories, regardless of external market alternatives.

Gain a Competitive Edge with Our Saudi Arabia Diagnostic Labs Market Report:

- Saudi Arabia Diagnostic Labs Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Saudi Arabia Diagnostic Labs Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Saudi Arabia Diagnostic Labs Market Policies, Regulations, and Product Standards

- Saudi Arabia Diagnostic Labs Market Trends & Developments

- Saudi Arabia Diagnostic Labs Market Dynamics

- Growth Factors

- Challenges

- Saudi Arabia Diagnostic Labs Market Hotspot & Opportunities

- Saudi Arabia Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Pathology

- Radiology & Imaging

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- Clinical Chemistry

- Hematology

- Immunology & Serology

- Microbiology

- Histopathology & Cytopathology

- Molecular Diagnostics

- Genetic Testing

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- X-Ray

- Ultrasound

- CT Scan

- MRI

- Mammography

- PET-CT

- Nuclear Imaging

- Others

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- Walk-in Testing

- Home Sample Collection

- Mobile Diagnostic Units

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- Infectious Diseases

- Oncology

- Diabetes & Endocrinology

- Cardiology

- Neurology

- Nephrology

- Gastroenterology

- Gynecology & Obstetrics

- Respiratory Disorders

- Orthopedics

- Others

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

- By Region- Market Size & Forecast 2022-2032, USD Million

- Riyadh

- Jeddah

- Dammam

- Makkah

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Pathology Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Radiology & Imaging Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Diagnostic Labs Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Al Borg Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Delta Medical Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alfa Medical Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saudi Diagnostic Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Farabi Medical Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Roya Specialized Medical Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tibyana Medical Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Hyatt Medical Laboratory Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Arab Medical Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Borg Diagnostics

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now