Saudi Arabia Construction Glass Market Research Report: Forecast (2026-2032)

Saudi Arabia Construction Glass Market - By Product Type (Annealed Glass, Tempered Glass, Laminated Glass, Insulated Glass, Coated Control Glass, Smart Glass, Others), By Chemical ... Composition (Soda-Lime, Potash-Lime, Potash-Lead), By Manufacturing Process (Float Process, Rolled/Sheet Process), By Application (Commercial, Residential, Industrial, Infrastructure), and others Read more

- Buildings, Construction, Metals & Mining

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

Saudi Arabia Construction Glass Market

Projected 6.28% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 800 Million

Market Size (2032)

USD 1225 Million

Base Year

2025

Projected CAGR

6.28%

Leading Segments

By Product Type: Tempered Glass

Saudi Arabia Construction Glass Market Report Key Takeaways:

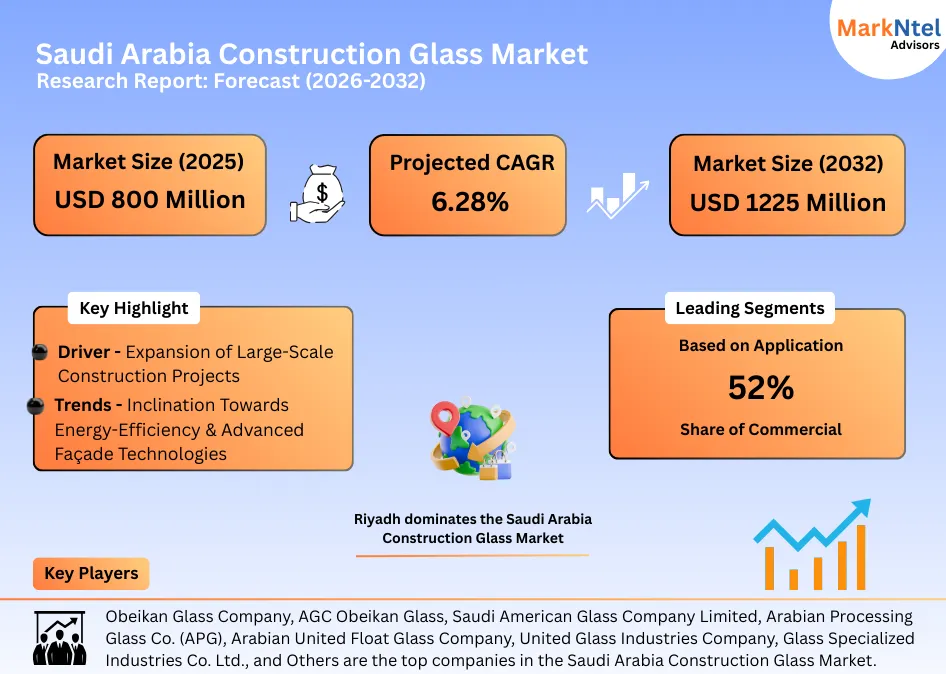

- Market size was valued at around USD 800 million in 2025 and is projected to reach USD 1,225 million by 2032. The estimated CAGR from 2026 to 2032 is around 6.28%, indicating strong growth.

- Riyadh holds the largest market share of about 35% in the Saudi Arabia Construction Glass Market in 2025.

- By product type, the tempered glass segment represented a significant share of about 45% in the Saudi Arabia Construction Glass Market in 2025.

- By application, the commercial sector presented a significant share of about 52% in the Saudi Arabia Construction Glass Market in 2025.

- Leading construction glass companies in the Saudi Arabia Market are Obeikan Glass Company, AGC Obeikan Glass, Saudi American Glass Company Limited, Arabian Processing Glass Co. (APG), Arabian United Float Glass Company, United Glass Industries Company, Glass Specialized Industries Co. Ltd., seele contracting, LLC, Saudi Guardian International Float Glass Co. Ltd, Zamil Industrial Investment Company (ZIIC), and Others.

Market Insights & Analysis: Saudi Arabia Construction Glass Market (2026-32):

The Saudi Arabia Construction Glass Market size was valued at approximately USD 800 million in 2025 and is projected to reach USD 1,225 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 6.28% during the forecast period, i.e., 2026-32.

The Saudi Arabia Construction Glass Market is projected to expand steadily, driven by rising large-scale construction activity and increasing adoption of energy-efficient, high-performance façade and glazing technologies.

Saudi Arabia’s built environment is undergoing an accelerated transformation in the mid-2020s, driven by large-scale urban redevelopment and high-density mixed-use construction . These developments are redefining architectural standards across the Kingdom, with increased emphasis on vertical construction, landmark structures, and visually distinctive façades. Such projects inherently increase demand for advanced construction materials, particularly architectural and façade glass, which plays a central role in modern urban design and in daylight-optimized buildings.

One of the most influential developments shaping long-term material demand is Jeddah Economic City, a master-planned urban redevelopment spanning approximately 56 million ft² (around 5.2 km²) with an estimated investment of USD 30 billion. The project is anchored by the Jeddah Tower, which is planned to exceed 1,000 meters in height, positioning it as the world’s tallest building upon completion . The tower is designed with a predominantly all-glass façade system, highlighting the critical role of high-performance glazing in super-tall construction.

Construction of the Jeddah Tower officially resumed in January 2025 after an extended pause, with updated timelines indicating targeted completion by 2028. The structural design combines reinforced concrete and steel, while the external envelope relies on advanced glass technologies engineered to withstand extreme wind loads, solar exposure, and height-related performance challenges. This restart has renewed market confidence and reinforces the importance of specialized façade glass solutions in next-generation megastructures.

Beyond super-tall developments, Jeddah Central represents another significant driver of architectural glass demand. Valued at approximately USD 20 billion, this Public Investment Fund–led mixed-use district will integrate residential buildings, hotels, museums, cultural venues, and retail zones. With phased construction extending through 2027, the project’s urban design prioritizes open façades, waterfront views, and transparent building envelopes, all of which intensify glazing requirements across multiple asset classes.

Saudi Arabia’s existing skyline further illustrates the established role of glass in landmark architecture. Structures such as the King Road Tower in Jeddah, featuring an all-glass façade integrated with a large-scale LED media screen, demonstrate how glass serves both functional and aesthetic purposes. These precedents reinforce continued preference for visually expressive and technologically advanced glazing systems in future developments.

Overall, Saudi Arabia’s construction glass outlook remains strongly positive, supported by megaproject restarts, large-scale urban districts, and an architectural shift toward high-rise, glass-intensive developments that prioritize performance, visibility, and iconic design.

Saudi Arabia Construction Glass Market Recent Developments:

- 2025: Saudi Arabia’s Gulf Guard (National Company for Glass Industries – ZOUJAJ) approved a USD 267 million investment to develop new float glass and glass coater production lines in Jubail Industrial City. The project aims to expand domestic capacity for architectural and energy-efficient glass, supporting large-scale construction demand and import substitution objectives.

- 2025: Big 5 Construct Saudi entered its second week in Riyadh, highlighting strong momentum in the Kingdom’s construction sector. The event featured innovations in façade systems, glazing, and sustainable building materials, reflecting rising demand from large-scale urban, commercial, and infrastructure projects across Saudi Arabia.

Saudi Arabia Construction Glass Market Scope

| Category | Segments |

|---|---|

| By Product Type | Annealed Glass, Tempered Glass, Laminated Glass, Insulated Glass, Coated Control Glass, Smart Glass, Others |

| By Chemical Composition | Soda-Lime, Potash-Lime, Potash-Lead |

| By Manufacturing Process | Float Process, Rolled/Sheet Process |

| By Application | Commercial, Residential, Industrial, Infrastructure |

Saudi Arabia Construction Glass Market Driver:

Expansion of Large-Scale Construction Projects

The primary driver of construction glass demand in Saudi Arabia is the acceleration of large-scale vertical and mixed-use developments, where advanced glazing systems are integral to façade performance, energy efficiency, wind resistance, and architectural identity rather than serving a purely decorative role.

Jeddah Tower exemplifies this demand, as its planned height exceeding 1,000 meters requires a fully engineered glass façade capable of withstanding extreme wind loads, structural stress, and solar exposure, driving the use of high-performance, specialized glazing systems .

The scale of façade demand is evidenced by the USD 280 million curtain wall contract awarded to Jangho Group, a global façade engineering firm. The contract scope extends beyond material supply to include façade design, fabrication, installation, performance testing, and maintenance, reflecting the technical depth and volume of construction glass required for such megastructures.

Project execution milestones further confirm sustained material uptake. In November 2025, Jangho Group completed the first curtain wall unit hoisting at Jeddah Tower, formally initiating large-scale façade installation and translating contractual commitments into physical glass deployment . Similar demand dynamics extend beyond super-tall buildings, as demonstrated by Jangho’s 36,000 m² curtain wall contract for King Fahd Sports City in Riyadh, indicating that stadiums and civic complexes are also driving substantial glass consumption .

The proliferation of façade-intensive megaprojects across Saudi Arabia is structurally expanding construction glass demand, anchoring market growth in long-term, capital-backed developments rather than short-cycle construction activity.

Saudi Arabia Construction Glass Market Trend:

Inclination Towards Energy-Efficiency & Advanced Façade Technologies

A key structural trend in Saudi Arabia’s construction glass market is the rapid adoption of energy-efficient glazing and advanced curtain wall systems, driven by extreme climatic conditions and strengthening regulations focused on building envelope performance and energy efficiency.

National energy policy has reinforced this transition through the Saudi Energy Efficiency Center (SEEC), which identifies buildings as a priority sector for electricity demand reduction and emphasizes envelope performance as a key intervention area . SEEC-backed technical frameworks influence façade material selection by promoting improved thermal resistance, reduced solar heat gain, and enhanced air tightness.

These objectives are formally embedded in the Saudi Building Code – Energy Conservation Code (SBC 601), which mandates minimum performance standards for insulation, air leakage, and fenestration in non-residential buildings, encouraging the adoption of insulated and high-performance glazing systems .

At the project execution level, megaprojects such as Jeddah Tower illustrate this trend in practice. Façade engineers are deploying unitized curtain wall systems integrating advanced glazing solutions engineered for superior thermal performance and water–air tightness. These systems are specifically designed to withstand coastal environmental conditions while meeting international façade performance standards.

The convergence of regulatory enforcement, climate-driven design requirements, and megaproject execution is institutionalizing energy-efficient glazing as a core specification in Saudi Arabia’s construction sector, positioning performance-oriented glass systems as a sustained market trend.

Saudi Arabia Construction Glass Market Opportunity:

World Cup 2034 Venue Infrastructure Expansion

A substantial opportunity for the Saudi Arabia construction glass market arises from the planned development of world-class stadium and event facilities tied to Saudi Arabia’s bid to host the FIFA World Cup 2034. These stadium projects are not only significant in scale but also require advanced façade and large-area glazing systems that meet performance, safety, and aesthetic specifications for modern sports venues, creating robust demand for construction glass solutions.

The Jeddah Central Development Stadium, currently under construction and expected to open in 2027, is planned with a seating capacity of 45,794 and will serve as a key venue for the World Cup’s group stage and round-of-32 matches, embedding structural material demand well ahead of tournament timelines.

Similarly, the King Abdullah Economic City Stadium is planned to begin construction in 2027 with a 45,700-seat capacity and scheduled completion by 2032, further expanding demand for performance glazing in large-format façade systems along the Red Sea coast.

The Aramco Stadium in Al Khobar, with a capacity of approximately 47,000 seats and expected completion by 2026, adds to the near-term material requirements, serving both the upcoming 2027 AFC Asian Cup and contributing to the World Cup infrastructure pipeline .

The integration of multiple stadium projects with staggered delivery timelines offers sustained, multi-year construction glass demand, positioning façade materials as fundamental components of Saudi Arabia’s sports and event infrastructure agenda.

Saudi Arabia Construction Glass Market Challenge:

Project Uncertainty and Execution Complexity

The project uncertainty and execution complexity remain a significant challenge for the Saudi Arabia Construction Glass market. A notable illustration is the temporary suspension of the Mukaab project in Riyadh, part of the New Murabba master development, as authorities reassessed project feasibility and funding alignment amid evolving fiscal priorities. Such interventions demonstrate that even landmark developments with global architectural ambition are not immune to strategic recalibration, introducing uncertainty into downstream material demand.

Project deferrals and suspensions disrupt the timing of façade system procurement and glass installations, directly affecting demand visibility for suppliers, fabricators, and façade contractors. These disruptions can weaken order backlogs and complicate capacity planning, particularly for manufacturers that align production schedules with multi-phase construction milestones.

In parallel, advanced façade projects, especially those involving large-scale or supertall structures, are characterized by prolonged design validation, engineering coordination, and regulatory approvals. The need for synchronization among international consultants, specialized manufacturers, and local authorities increases execution risk and extends project lead times.

Overall, project suspensions and complex execution frameworks reduce demand predictability, elevate operational risk, and constrain short-term growth visibility for construction glass suppliers across Saudi Arabia’s high-value development pipeline, limiting predictable growth prospects for the construction glass market.

Saudi Arabia Construction Glass Market (2026-32) Segmentation Analysis:

The Saudi Arabia Construction Glass Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Annealed Glass

- Tempered Glass

- Laminated Glass

- Insulated Glass

- Coated Control Glass

- Smart Glass

- Others

The tempered glass segment dominates the Saudi Arabia Construction Glass market, accounting for approximately 45% of market share, reflecting its critical role in meeting the Kingdom’s structural, safety, and environmental performance requirements.

Its high mechanical strength, approximately four to five times greater than conventional annealed glass, makes it particularly suitable for high-rise towers, large commercial developments, and expansive façade applications where resistance to wind loads and structural stress is essential. As Saudi Arabia continues to prioritize vertical urban development and architecturally complex projects, tempered glass has become a foundational material within modern building envelopes.

Regulatory and safety considerations further reinforce its market leadership. Tempered glass complies with stringent building safety standards due to its controlled breakage pattern, which minimizes injury risk in public and high-traffic environments. This characteristic supports its extensive adoption in façades, entrances, partitions, balustrades, and skylights across commercial, hospitality, and mixed-use assets.

Climatic suitability is another decisive factor underpinning dominance. Saudi Arabia’s extreme heat and high solar exposure demand glazing materials capable of withstanding thermal stress and temperature fluctuations.

Tempered glass offers superior thermal shock resistance and integrates efficiently with coatings, laminates, and insulated units, enabling its use in advanced façade systems and sustaining its leadership across performance-driven construction projects.

Based on Application:

- Commercial

- Residential

- Industrial

- Infrastructure

The commercial segment dominates the Saudi Arabia Construction Glass market, holding around 52% market share, primarily due to the scale, complexity, and performance requirements of non-residential developments.

Large commercial assets such as office towers, shopping malls, hotels, convention centers, and mixed-use complexes incorporate extensive glazed façades, atriums, and curtain wall systems, resulting in substantially higher glass consumption per project compared to residential structures.

Commercial buildings are also subject to more stringent regulatory and operational performance standards under the Saudi Building Code, particularly with respect to energy efficiency, safety, and durability. This drives widespread adoption of high-value glazing solutions, including insulated glass units, low-emissivity coatings, laminated safety glass, and engineered curtain wall assemblies designed to optimize thermal performance and solar control.

Furthermore, Vision 2030-driven investments are heavily concentrated in commercial and hospitality-led developments, where architectural identity and visual transparency are critical design objectives.

The combination of large project scale, advanced façade specifications, and sustained public and private investment positions the commercial segment as the primary driver of construction glass demand across the Kingdom.

Saudi Arabia Construction Glass Market (2026-32): Regional Projection

Riyadh dominates the Saudi Arabia Construction Glass Market with an estimated 35% share, reflecting its central role as the nation’s political, administrative, and economic hub. The region’s leadership in awarding major public works and urban development contracts directly supports demand for high-performance façade materials, including architectural glass.

In January 2025, Riyadh secured a substantial portion of the USD 1.7 billion of government construction contracts, with the capital’s share concentrated in large-scale housing, transport, and industrial sector projects .

Municipal initiatives further reinforce Riyadh’s construction leadership. In March 2025, the Riyadh Municipality announced 20 new investment opportunities spanning more than 175,000 m² of development land across mixed-use, residential, commercial, and industrial sites as part of Vision 2030’s urban expansion strategy . These structured city programs attract significant private capital and elevate the specification of façade systems in emerging developments.

Independent sector reporting confirms Riyadh as a concentrated holder of national construction value, accounting for a large portion of total project awards and ongoing pipelines across infrastructure, real estate, and civic assets.

This sustained intensity of construction activity, coupled with focused municipal facilitation and strategic public investment, underpins Riyadh’s dominant position within the construction glass market, as high-specification glass solutions are increasingly incorporated into the region’s urban transformation agenda.

Gain a Competitive Edge with Our Saudi Arabia Construction Glass Market Report:

- Saudi Arabia Construction Glass Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Saudi Arabia Construction Glass Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Saudi Arabia Construction Glass Market Policies, Regulations, and Product Standards

- Saudi Arabia Construction Glass Market Trends & Developments

- Saudi Arabia Construction Glass Market Dynamics

- Growth Factors

- Challenges

- Saudi Arabia Construction Glass Market Hotspot & Opportunities

- Saudi Arabia Construction Glass Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Annealed Glass

- Tempered Glass

- Laminated Glass

- Insulated Glass

- Coated Control Glass

- Smart Glass

- Others

- By Chemical Composition- Market Size & Forecast 2022-2032, USD Million

- Soda-Lime

- Potash-Lime

- Potash-Lead

- By Manufacturing Process- Market Size & Forecast 2022-2032, USD Million

- Float Process

- Rolled/Sheet Process

- By Application- Market Size & Forecast 2022-2032, USD Million

- Commercial

- Residential

- Industrial

- Infrastructure

- By Region- Market Size & Forecast 2022-2032, USD Million

- Riyadh

- Jeddah

- Damam

- Mecca & Madinah

- Others

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Annealed Glass Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Chemical Composition- Market Size & Forecast 2022-2032, USD Million

- By Manufacturing Process- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Tempered Glass Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Chemical Composition- Market Size & Forecast 2022-2032, USD Million

- By Manufacturing Process- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Laminated Glass Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Chemical Composition- Market Size & Forecast 2022-2032, USD Million

- By Manufacturing Process- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Insulated Glass Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Chemical Composition- Market Size & Forecast 2022-2032, USD Million

- By Manufacturing Process- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Coated Control Glass Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Chemical Composition- Market Size & Forecast 2022-2032, USD Million

- By Manufacturing Process- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Smart Glass Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Chemical Composition- Market Size & Forecast 2022-2032, USD Million

- By Manufacturing Process- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Construction Glass Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Obeikan Glass Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AGC Obeikan Glass

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saudi American Glass Company Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arabian Processing Glass Co. (APG)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arabian United Float Glass Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- United Glass Industries Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Glass Specialized Industries Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- seele contracting, LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saudi Guardian International Float Glass Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zamil Industrial Investment Company (ZIIC)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Obeikan Glass Company

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now