India Payment Gateways Market Research Report: Forecast (2026-2032)

India Payment Gateways Market - By Payment Method (Credit / Debit Cards, UPI, Digital Wallets (eWallets), Bank Transfers, Cryptocurrencies, QR-Code Payments, Buy Now, Pay Later (BN ... PL)), By Transaction Mode (Online Payments (Web), In-App / Mobile Payments, Point of Sale (POS)), By Enterprise Size (Small & Medium Enterprise (SMEs), Large Enterprise), By End User (Retail & E-Commerce, Banking, Financial Services & Insurance (BFSI), Travel & Hospitality, Healthcare, Education, Government Services, Transportation & Logistics, Telecommunications, Others), and others Read more

- FinTech

- Mar 2026

- Pages 175

- Report Format: PDF, Excel, PPT

India Payment Gateways Market

Projected 9.69% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 2.25 Billion

Market Size (2032)

USD 3.92 Billion

Base Year

2025

Projected CAGR

9.69%

Leading Segments

By End User: Retail & E-Commerce

India Payment Gateways Market Report Key Takeaways:

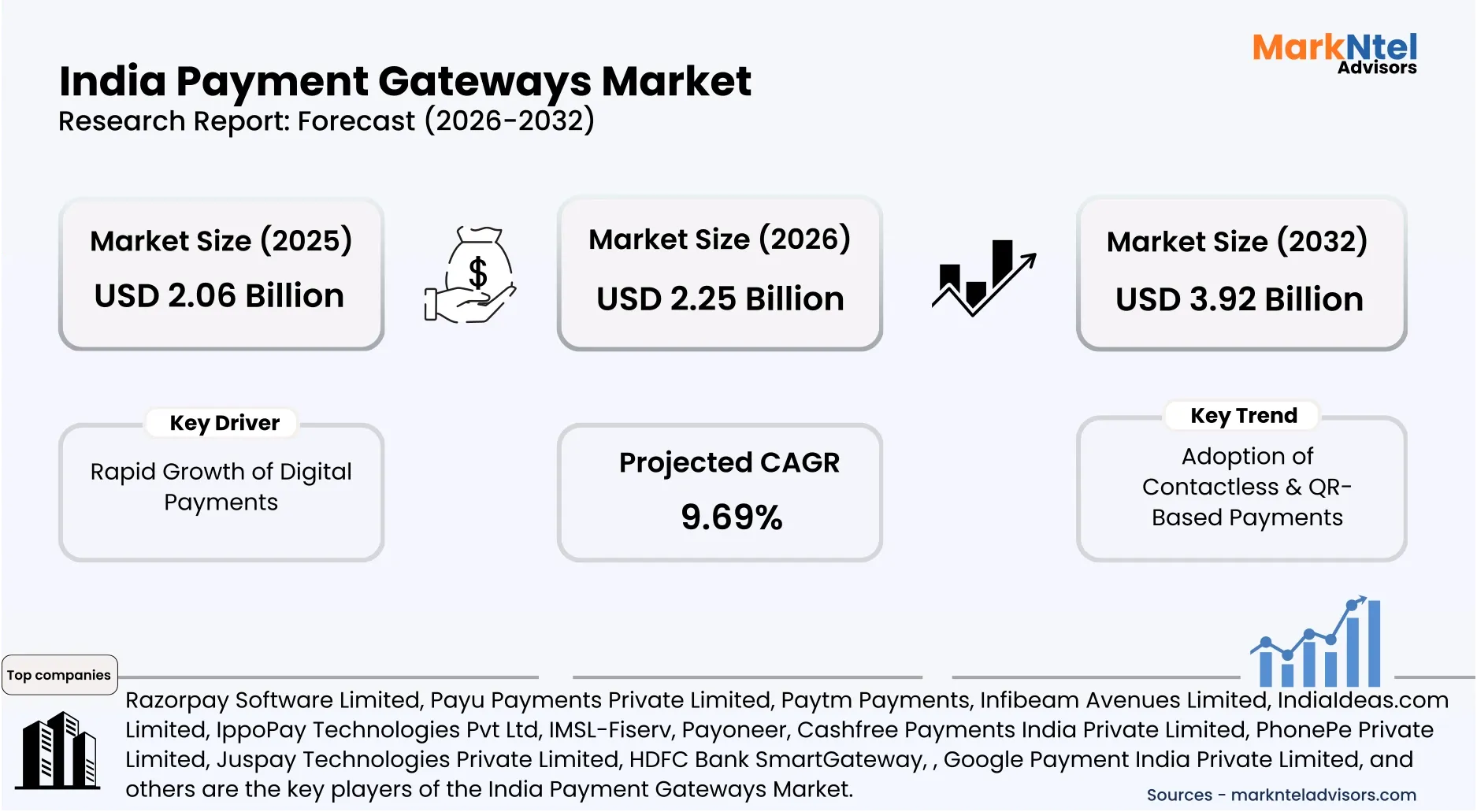

- The India Payment Gateways Market size was valued at around USD 2.06 billion in 2025 and is projected to grow from USD 2.25 billion in 2026 to USD 3.92 billion by 2032. The estimated CAGR from 2026 to 2032 is around 9.69%, indicating strong growth.

- By payment method, the UPI segment seized around 62% of the India Payment Gateways Market size in 2026.

- By end user, the retail & e-commerce represented 45% of the India Payment Gateways Market size in 2026, and Healthcare is growing with a CAGR of 12% during 2026-32.

- West region leads the India Payment Gateways Market with a substantial 35% share in 2026.

- The leading payment gateway companies in India are Razorpay Software Limited, Payu Payments Private Limited, Paytm Payments, Infibeam Avenues Limited, IndiaIdeas.com Limited, IppoPay Technologies Pvt Ltd, IMSL-Fiserv, Payoneer, Cashfree Payments India Private Limited, PhonePe Private Limited, Instamojo Technologies Private Limited, Juspay Technologies Private Limited, HDFC Bank SmartGateway, Airpay Payment Services Private Limited, Easebuzz Private Limited, NTT DATA Payment Services India Ltd, Stripe, Pine Labs, Amazon Pay (India) Private Limited, Google Payment India Private Limited, and others.

Market Insights & Analysis: India Payment Gateways Market (2026- 2032):

The India Payment Gateways Market size was valued at around USD 2.06 billion in 2025 and is projected to grow from USD 2.25 billion in 2026 to USD 3.92 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 9.69% during the forecast period, i.e., 2026-32.

The India Payment Gateways Market is experiencing rapid growth, driven by the accelerating penetration of digital payments and the increasing adoption of contactless and QR-based payment mechanisms.

India’s payment gateway ecosystem in 2025 is anchored in strong nationwide digital transaction momentum supported by institutional reforms and infrastructure expansion. For instance, the Reserve Bank of India recorded the Digital Payments Index (DPI) at 493.22 in March 2025, reflecting measurable progress in payment infrastructure robustness, transaction performance, and user adoption. This upward trajectory demonstrates how digital payment systems have become deeply embedded across commerce, public services, and institutional financial flows.

UPI transaction volumes grew 42% year-on-year in the second half of 2024, reaching over 93 billion transactions, while aggregate transaction value surpassed USD 2.5 trillion . This combination of high-frequency usage and rising ticket sizes is materially increasing transaction throughput, reinforcing merchant reliance on payment gateways for real-time processing, reconciliation, and settlement across digital channels.

India’s digital payments ecosystem gained global prominence in 2025 when the IMF recognized UPI as the world’s largest real-time retail payment system, processing nearly half of global instant transactions. With over 129.3 billion annual payments, India now anchors global real-time payment growth .

A critical catalyst supporting gateway market expansion is the rapid densification of acceptance infrastructure. QR code deployments expanded sharply, rising 126% year-on-year to over 633 million by late 2024 and exceeding 709 million active codes nationwide in 2025. This expansion has created one of the world’s most extensive digital acceptance networks. Importantly, adoption is no longer concentrated solely in major metropolitan areas; accelerated deployment across Tier-2 and Tier-3 cities such as Lucknow, Jaipur, Kochi, and Bhubaneswar indicates broad-based merchant onboarding.

India’s payment gateways market outlook remains strongly positive, underpinned by deepening adoption of contactless and QR-based payments across both urban and semi-urban ecosystems. Digital acceptance is no longer limited to large merchants or metros; its penetration into public infrastructure highlights structural maturity. For instance, the Nagpur division of Central Railway recorded a 22.10% share of QR-based transactions at ticket counters, demonstrating how everyday transit systems are integrating cashless payments to improve efficiency, reduce queues, and enhance passenger convenience. Such use cases expand transaction density and directly increase gateway processing volumes.

On the supply side, payment gateway providers are aligning their platforms with QR-first consumption patterns. IndiConnect, for example, offers integrated UPI gateway solutions that combine dynamic and static QR collection, UPI intents, and secure checkout flows across web and mobile channels. These capabilities enable merchants to unify online and offline acceptance, reinforcing gateways as critical orchestration layers in India’s contactless economy.

Similarly, BharatQR, a standardized QR framework developed by NPCI in collaboration with Mastercard and Visa, has emerged as a universal acceptance protocol embedded across gateways and PoS systems, reducing fragmentation and supporting interoperable, contactless payments nationwide.

Looking beyond 2025, policy-led expansion will further accelerate market growth. For example, the Reserve Bank of India and NPCI International Payments Ltd (NIPL) plan to extend UPI connectivity to around 20 countries by 2028–29, enabling cross-border real-time payments for tourism, remittances, and ecommerce. This internationalization will compel global merchants and platforms to integrate UPI-compatible gateways.

In parallel, national digital payment strategies target 1 billion unique UPI users by 2030 through district-level coverage expansion and welfare-linked payment integration, substantially enlarging the transaction base.

The convergence of widespread QR adoption, interoperable payment standards, and forward-looking global expansion plans positions India’s payment gateways market for sustained, multi-year growth. As acceptance deepens domestically and extends internationally, gateway platforms will become increasingly central to India’s digital commerce infrastructure.

India Payment Gateways Market Recent Developments:

- October 2025: BharatPe unveiled BharatPeX, an AI-powered digital payments stack designed to streamline enterprise payment integrations by combining in-app UPI, cards, and net-banking acceptance with implementation support and a virtual AI assistant. This aims to accelerate onboarding, enhance payment success rates, and offer enterprises greater control over user journeys and data.

- August 2025: Razorpay has collaborated with CRED and Visa to roll out CardSync, a one-tap card payment solution designed to simplify online checkouts across merchants using Razorpay. The solution leverages Visa’s tokenization framework to enable secure card portability, reduce payment friction, and improve transaction success rates by eliminating repeated card data entry during digital purchases.

India Payment Gateways Market Scope:

| Category | Segments |

|---|---|

| By Payment Method | Credit / Debit Cards, UPI, Digital Wallets (eWallets), Bank Transfers, Cryptocurrencies, QR-Code Payments, Buy Now, Pay Later (BNPL) |

| By Transaction Mode | Online Payments (Web), In-App / Mobile Payments, Point of Sale (POS) |

| By Enterprise Size | Small & Medium Enterprise (SMEs), Large Enterprise |

| By End User | Retail & E-Commerce, Banking, Financial Services & Insurance (BFSI), Travel & Hospitality, Healthcare, Education, Government Services, Transportation & Logistics, Telecommunications, Others |

India Payment Gateways Market Driver:

Rapid Growth of Digital Payments

The accelerated expansion of digital payments in India has emerged as a foundational driver of growth for the payment gateways market. In the first half of 2025, digital modes accounted for 99.8% of transaction volumes and 97.7% of value, highlighting a near-total shift from cash. This reflects the maturity of UPI-led real-time payments, increasing merchant reliance on scalable, reliable payment gateway infrastructure.

This growth is reinforced by rapid expansion in digital acceptance infrastructure. In 2024–25, PoS terminals increased 24.7% to about 11 million, while UPI QR codes rose to nearly 658 million . Low-cost QR adoption has brought small and informal merchants into digital commerce, expanding the addressable market and driving higher payment gateway usage across retail and services.

Underlying this growth is a measurable strengthening of payment system performance and usage. The Reserve Bank of India’s Digital Payments Index (DPI) increased to 465.33 by September 2024, rising 4.45% from March 2024, reflecting sustained improvements in infrastructure availability, transaction efficiency, and consumer adoption . The DPI’s upward trajectory indicates that digital payments growth is structural rather than cyclical, creating durable demand for scalable and secure gateway platforms.

The convergence of near-universal digital transaction usage, rapid acceptance infrastructure deployment, and sustained improvements in payment system performance is structurally expanding transaction volumes. This environment positions payment gateways as critical enablers of India’s digital economy, driving sustained market growth in the coming years.

India Payment Gateways Market Trend:

Adoption of Contactless & QR-Based Payments

Contactless and QR-based payments have transitioned from an emerging innovation to a core structural pillar of India’s digital payment ecosystem, fundamentally reshaping payment gateway demand. The scalability, low cost, and interoperability of QR-based acceptance, particularly through the Unified Payments Interface (UPI), have enabled rapid merchant onboarding across both organized and unorganized sectors.

In 2024–25, UPI QR codes recorded a sharp 91.5% year-on-year expansion, reaching approximately 657.9 million acceptance points. This surge reflects one of the fastest build-outs of digital payment infrastructure globally and underscores the growing reliance on real-time, contactless transaction modes in daily commerce.

This structural shift has materially strengthened the relevance of payment gateways that support multi-rail integrations, QR-first acceptance, and seamless checkout experiences. Platforms such as CCAvenue have aligned closely with this trend by enabling UPI QR, contactless payments, and card-based transactions through unified gateway solutions for online stores, mobile applications, and enterprise merchants.

Similarly, Pine Labs has emerged as a key enabler of QR-led and contactless acceptance through its integrated PoS systems and digital gateway offerings, which are widely deployed across retail, hospitality, and service sectors .

The rapid normalization of QR and contactless payments is not a cyclical shift but a structural transformation. As digital acceptance deepens nationwide, payment gateways with robust QR, UPI, and omni-channel capabilities are positioned to capture sustained transaction growth.

India Payment Gateways Market Challenge:

Security and Fraud Risks

Security vulnerabilities and rising digital fraud pose a material challenge to the growth of India’s payment gateways market, directly affecting consumer confidence and merchant adoption. Between April 2024 and January 2025, digital fraud losses reached about USD 515 million across 2.4 million cases, highlighting the rise of sophisticated cyber threats alongside expanding digital payment usage .

Regulatory data further highlight persistent exposure within formal banking and payment channels. In 2025, the Reserve Bank of India recorded 13,516 fraud incidents linked to digital payment modes, including cards and internet banking, with losses of around USD 63 million.

Longer-term data reinforce the structural nature of this risk as government disclosures show 63,315 digital payment fraud cases over the decade ending 2024, resulting in cumulative losses of USD 89 million. Moreover, RBI statistics indicate that total financial fraud values nearly tripled in 2024–25, rising to USD 4.4 billion as reporting coverage expanded .

Overall, persistently high fraud exposure increases compliance costs for gateway providers and may slow onboarding, thereby constraining market momentum unless security frameworks strengthen significantly.

India Payment Gateways Market (2026-32) Segmentation Analysis:

The India Payment Gateways Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Payment Method:

- Credit / Debit Cards

- UPI

- Digital Wallets (eWallets)

- Bank Transfers

- Cryptocurrencies

- QR-Code Payments

- Buy Now, Pay Later (BNPL)

- Others

The UPI segment holds the top spot in the India Payment Gateways Market, with a market share of around 62%. This segment is maintaining its leadership due to its highly scalable architecture, seamless interoperability across banks and platforms, and extensive adoption by both consumers and merchants.

As per the Reserve Bank of India’s 2024–25 data, UPI contributed 83.7% of total digital payment transaction volumes, increasing from 79.7% in the previous year, which highlights its expanding role as the primary channel for electronic transactions. During the same period, UPI facilitated 185.8 billion transactions, reflecting a 41% year-on-year growth, and demonstrating its ability to sustain high transaction intensity at a national scale.

Moreover, the aggregate value of UPI transactions increased from approximately USD 2.4 trillion to approximately USD 3.1 trillion, indicating growing acceptance for higher-value payments alongside routine retail use .

The combination of real-time settlement, low operational costs, and ease of integration with digital platforms has reinforced UPI’s centrality, enabling it to outperform alternative payment modes and maintain leadership within the evolving digital payments ecosystem.

Based on End User:

- Retail & E-Commerce

- Banking, Financial Services & Insurance (BFSI)

- Travel & Hospitality

- Healthcare

- Education

- Government Services

- Transportation & Logistics

- Telecommunications

- Others

The retail & e-commerce category leads the India Payment Gateways Industry, accounting for 45% of market share, primarily due to the structural shift toward digital purchasing channels. The sustained growth of online marketplaces, direct-to-consumer (D2C) brands, and omnichannel retail formats has significantly increased reliance on payment gateways to manage high-frequency, low-latency transactions. These platforms require seamless integration of multiple payment instruments, real-time settlement, automated reconciliation, and scalable checkout infrastructure, positioning payment gateways as a core operational layer.

Rising consumer preference for instant, frictionless digital payments across UPI, cards, wallets, and alternative payment methods has further strengthened gateway adoption within retail. High transaction volumes generated by flash sales, festival-driven demand, and subscription-based commerce continue to reinforce this segment’s revenue contribution.

Additionally, the expansion of small and medium online sellers, enabled by simplified onboarding and low-cost digital acceptance, has broadened the merchant base using gateway solutions.

While retail and e-commerce remain dominant, adjacent sectors are evolving rapidly. Healthcare is emerging as a high-growth end-user segment, expanding at a CAGR of 12%, supported by digital consultations, online pharmacies, and hospital payment platforms. Despite this momentum, the scale, transaction density, and continuous usage patterns of retail and e-commerce ensure their continued leadership in driving demand for payment gateway services.

India Payment Gateways Market (2026-32): Regional Projection

The India Payment Gateways Market is dominated by the West region, which holds a commanding 35% share, supported by its high concentration of commercial activity, advanced digital infrastructure, and early adoption of cashless transactions.

The region hosts major financial and business hubs such as Mumbai, Pune, Ahmedabad, and Surat, which collectively generate substantial transaction volumes across retail, e-commerce, financial services, and enterprise payments.

Mumbai’s position as India’s financial capital has been particularly influential, with intensive usage of online banking, fintech platforms, and corporate payment systems that depend heavily on reliable and scalable gateway solutions.

This dominance is reinforced by exceptionally high digital payment adoption levels. According to state-wise data released by the National Payments Corporation of India (NPCI) for the first quarter of 2025-26, Maharashtra alone recorded approximately 6.58 billion UPI transactions, significantly exceeding volumes in other major states and firmly anchoring the digital payments ecosystem in western India . Such a scale reflects both mature urban demand and strong penetration of contactless acceptance infrastructure across semi-urban markets.

Moreover, West India benefits from a dense and diversified merchant base, spanning organized retail, small traders, D2C brands, and service aggregators. Widespread adoption of UPI, cards, and QR-based payments has intensified gateway usage for high-frequency consumer transactions.

Complemented by proactive digital payment adoption by state and municipal authorities for public services, the region’s economic density and fintech readiness continue to position West India as the leading contributor to national payment gateway demand.

Gain a Competitive Edge with Our India Payment Gateways Market Report:

- India Payment Gateways Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- India Payment Gateways Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- India Payment Gateways Market Policies, Regulations, and Product Standards

- India Payment Gateways Market Trends & Developments

- India Payment Gateways Market Dynamics

- Growth Factors

- Challenges

- India Payment Gateways Market Hotspot & Opportunities

- India Payment Gateways Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Payment Method- Market Size & Forecast 2022-2032, USD Million

- Credit / Debit Cards

- UPI

- Digital Wallets (eWallets)

- Bank Transfers

- Cryptocurrencies

- QR-Code Payments

- Buy Now, Pay Later (BNPL)

- By Transaction Mode- Market Size & Forecast 2022-2032, USD Million

- Online Payments (Web)

- In-App / Mobile Payments

- Point of Sale (POS)

- By Enterprise Size- Market Size & Forecast 2022-2032, USD Million

- Small & Medium Enterprise (SMEs)

- Large Enterprise

- By End User- Market Size & Forecast 2022-2032, USD Million

- Retail & E-Commerce

- Banking, Financial Services & Insurance (BFSI)

- Travel & Hospitality

- Healthcare

- Education

- Government Services

- Transportation & Logistics

- Telecommunications

- Others

- By Region- Market Size & Forecast 2022-2032, USD Million

- North

- South

- East

- West

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Payment Method- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Credit / Debit Cards Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Transaction Mode- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India UPI Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Transaction Mode- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Digital Wallets (eWallets) Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Transaction Mode- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Bank Transfers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Transaction Mode- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Cryptocurrencies Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Transaction Mode- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India QR-Code Payments Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Transaction Mode- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Buy Now, Pay Later (BNPL) Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Transaction Mode- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Payment Gateways Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Razorpay Software Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Payu Payments Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Paytm Payments

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Infibeam Avenues Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IndiaIdeas.com Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IppoPay Technologies Pvt Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IMSL-Fiserv

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Payoneer

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cashfree Payments India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PhonePe Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Instamojo Technologies Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Juspay Technologies Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HDFC Bank SmartGateway

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Airpay Payment Services Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Easebuzz Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NTT DATA Payment Services India Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Stripe

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pine Labs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amazon Pay (India) Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Google Payment India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Razorpay Software Limited

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now