Japan Pacemakers Market Research Report: Forecast (2026-2032)

Japan Pacemakers Market - By Product Type (Implantable Pacemakers, External Pacemakers), By Technology (Single-Chamber Pacemakers, Dual-Chamber Pacemakers, Biventricular Pacemaker ... s), By Device Platform (Conventional Transvenous Pacemakers, MRI-Compatible Pacemakers, Leadless Pacemakers), By Component (Pulse Generator, Leads, Accessories & Programming Systems), By Clinical Indication Bradyarrhythmias, (Heart Block, Sick Sinus Syndrome), Atrial Fibrillation with Slow Ventricular Response, Heart Failure (CRT Indication), Post-Myocardial Infarction Temporary Pacing, Others), By End User (Hospitals & Cardiac Centers, Ambulatory Surgical Centers, Others), ans others Read more

- Healthcare

- Jan 2026

- Pages 135

- Report Format: PDF, Excel, PPT

Japan Pacemakers Market

Projected 3.78% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 118 Million

Market Size (2032)

USD 153 Million

Base Year

2025

Projected CAGR

3.78%

Leading Segments

By End User: Hospitals & Cardiac Centers

Japan Pacemakers Market Report Key Takeaways:

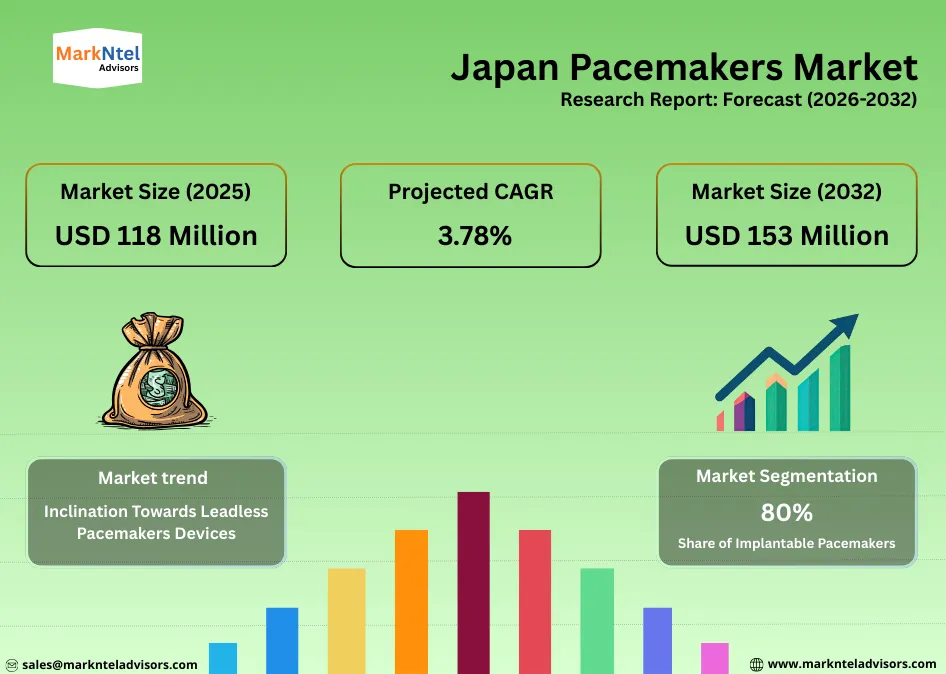

- The Japan Pacemakers Market size was valued at around USD 118 million in 2025 and is projected to reach USD 153 million by 2032. The estimated CAGR from 2026 to 2032 is around 3.78%, indicating strong growth.

- By product type, the implantable pacemakers seized around 80% of the Japan Pacemakers Market size in 2025.

- By end user, the hospitals & cardiac centers represented 75% of the Japan Pacemakers Market size in 2025.

- By technology, the dual-chamber pacemakers represented 45% of the Japan Pacemakers Market size in 2025.

- The leading pacemaker companies in Japan are Medtronic Plc, Abbott Laboratories, Boston Scientific Corporation, Osypka Medical GmbH, BIOTRONIK SE & Co. KG, MicroPort Scientific Corporation, Japan Lifeline Co., Ltd., ZOLL Medical Corporation, and others.

Market Insights & Analysis: Japan Pacemakers Market (2026- 2032):

The Japan Pacemakers Market size was valued at around USD 118 million in 2025 and is projected to reach USD 153 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 3.78% during the forecast period, i.e., 2026-32.

The Japan Pacemakers Market is experiencing rapid growth, driven by the rising burden of cardiovascular diseases and the growing clinical adoption of leadless pacemaker technologies that enhance patient safety, procedural efficiency, and long-term outcomes.

According to the Ministry of Health, Labour and Welfare (MHLW), heart disease (excluding hypertensive disorders) ranked as Japan’s second leading cause of death in 2024, accounting for 14.1% of total mortality .

Overall deaths rose to approximately 1.61 million in 2024 from 1.58 million in the prior year, underscoring the intensifying clinical exposure to serious cardiac conditions. This epidemiological backdrop directly strengthens demand for rhythm management therapies, including permanent pacemaker implantation.

Clinical registries further validate the depth and geographic spread of advanced cardiovascular disease. Japan’s nationwide JROADHF registry enrolled 4,329 hospitalized patients with heart failure with reduced ejection fraction (HFrEF), a population closely associated with bradyarrhythmias and conduction disorders .

Patients were distributed across all major regions, with Kanto (22.1%), Kinki (20.8%), and Chubu (18.0%) representing major concentrations. Ischemic heart disease accounted for 36.3% of cases nationwide, while arrhythmia-related etiologies formed a substantial share, reaching 16.9% in Kinki. These regionally differentiated patterns indicate persistent, localized demand for device-based rhythm management, reinforcing pacemakers as an essential component of Japan’s cardiac care infrastructure.

Technological transformation is amplifying this demand. The Pharmaceuticals and Medical Devices Agency (PMDA) confirmed in September 2024 that Abbott Medical Japan’s Aveir LP leadless pacemaker received expanded review for atrial pacing and AV synchrony, beyond ventricular-only use .

Clinical data demonstrated a 91% composite pacing success at three months and AV synchrony rates of approximately 95.7% among Japanese patients. By eliminating transvenous leads and subcutaneous generator pockets, leadless systems significantly reduce infection risk and procedural complexity, making them increasingly suitable for Japan’s aging and frail patient base.

Furthermore, this shift is reinforcing the dominance of advanced configurations, with dual-chamber pacemakers leading by technology at 45% share, reflecting rising clinical preference for physiologic pacing and AV coordination .

Japan’s cardiovascular disease burden is set to intensify well beyond 2025, underpinned by one of the world’s fastest-aging population profiles. Projections from the National Institute of Population and Social Security Research indicate that by 2070, nearly 40% of Japan’s population will be aged 65 and above, rising from about 29% in 2023, meaning roughly two in every five residents will be elderly. This demographic shift will substantially expand the pool of individuals vulnerable to age-related cardiac conditions, particularly heart failure and arrhythmias, which are primary indications for pacing therapy.

Moreover, the population aged 80 and above is expected to double to approximately 12 million by 2050. Advanced age is a dominant risk factor for atrial fibrillation, conduction disorders, and progressive heart failure, ensuring a structurally rising incidence of rhythm abnormalities.

The convergence of rising cardiovascular mortality, regionally entrenched heart failure prevalence, and rapid adoption of leadless and dual-chamber technologies establishes a durable growth trajectory for Japan’s pacemakers market. As demographic aging accelerates, pacemakers will become increasingly central to national cardiac care delivery, sustaining long-term market expansion.

Japan Pacemakers Market Scope:

| Category | Segments |

|---|---|

| By Product Type | Implantable Pacemakers, External Pacemakers |

| By Technology | Single-Chamber Pacemakers, Dual-Chamber Pacemakers, Biventricular Pacemakers |

| By Device Platform | Conventional Transvenous Pacemakers, MRI-Compatible Pacemakers, Leadless Pacemakers |

| By Component | Pulse Generator, Leads, Accessories & Programming Systems |

| By Clinical Indication | Bradyarrhythmias, (Heart Block, Sick Sinus Syndrome), Atrial Fibrillation with Slow Ventricular Response, Heart Failure (CRT Indication), Post-Myocardial Infarction Temporary Pacing, Others |

| By End User | Hospitals & Cardiac Centers, Ambulatory Surgical Centers, Others), ans others |

Japan Pacemakers Market Drivers:

Rising Incidence of Cardiovascular Diseases

Japan is witnessing a sustained rise in cardiovascular disease (CVD) burden, directly strengthening demand for pacemakers and rhythm-management solutions. The Ministry of Health, Labour and Welfare’s latest Patient Survey shows that 3.58 million people were receiving continuous treatment for heart diseases in 2023, excluding hypertensive heart disease .

This represents an increase of 530,000 patients, that are equivalent to nearly 17% growth in just three years. Within this population, arrhythmia and conduction disorders affected 1.09 million people, while heart failure impacted 722,000 patients and angina pectoris 978,000, highlighting a large and expanding pool of patients clinically aligned with pacemaker therapy .

The disease burden is further amplified by comorbid conditions. Epidemiological research indicates that 63.1% of adults with type-2 diabetes in Japan already have established cardiovascular disease, including coronary and cerebrovascular conditions. This intersection of metabolic and cardiac disorders accelerates progression toward rhythm abnormalities and structural heart disease, reinforcing long-term device demand.

Demographics compound this trend. Japan’s population is aging rapidly, with individuals aged over 75 expected to exceed 20% of the population by 2025 . Advanced age is a primary risk factor for bradyarrhythmias and heart failure, both of which frequently require pacing therapy.

The sharp rise in heart disease prevalence, the million-plus arrhythmia population, and Japan’s accelerating aging curve are structurally expanding the pacemaker candidate base. Together, these forces will continue to propel sustained market growth well beyond 2025.

Japan Pacemakers Market Trends:

Inclination Towards Leadless Pacemakers Devices

A defining trend in Japan’s pacemaker industry is the accelerating shift toward leadless pacemakers, driven by the need for safer, less invasive cardiac rhythm management. These systems are increasingly favored in older and frail patients, where minimizing surgical trauma and post-implant complications is critical.

At the same time, clinicians are beginning to reconsider leadless pacing for younger cohorts to reduce lifelong risks associated with transvenous leads, such as fracture, infection, and venous obstruction. Reflecting this evolution, Japan’s cardiac rhythm management guidelines now explicitly reference leadless pacing as an appropriate therapeutic option in selected patients.

As of 2024, Japan has two classes of approved leadless pacemakers in routine clinical use: single-chamber VVI systems such as Micra™ VR and Aveir™ VR, and the VDD-capable Micra™ AV, which enables atrioventricular synchrony without transvenous leads. Implanted directly into the right ventricle via catheter, these devices eliminate surgical pockets and lead systems, the primary sources of conventional pacemaker complications .

Clinical studies demonstrate procedural success rates of approximately 98–99% and consistently low complication profiles, validating their real-world safety and effectiveness. These advantages are reshaping physician preferences and institutional protocols, particularly in high-risk and elderly populations.

By offering safer implantation, fewer long-term complications, and expanding pacing capabilities, leadless pacemakers are redefining standard care in Japan. Their growing acceptance will structurally elevate device adoption and accelerate pacemaker market growth in the years ahead.

Japan Pacemakers Market Challenges:

High Costs and Reimbursement Constraints

Japan’s pacemakers market faces a persistent structural challenge from high device costs combined with rigid reimbursement policies under the National Health Insurance (NHI) system. The Ministry of Health, Labour and Welfare (MHLW) centrally controls implantable device pricing through fixed fee schedules, prioritizing cost containment over technology differentiation.

As a result, advanced systems such as leadless pacemakers and dual-chamber platforms often receive reimbursement comparable to conventional devices, despite higher acquisition costs and superior long-term clinical value. Hospitals are therefore compelled to limit their use or absorb part of the expense, restricting access even for eligible patients.

Policy-driven underutilization extends to other cardiac implantable therapies. Certain primary-prevention implantable cardioverter defibrillators (ICDs) remain unreimbursed for specific indications. A multicenter Japanese study reported that patients who were clinically eligible but untreated before cardiac arrest generated average medical costs of approximately USD 11,679, reflecting the economic burden created when preventive device therapy is delayed .

Overall, constrained reimbursement and high upfront costs suppress the adoption of advanced pacing technologies. Without structural reform, financial barriers will continue to slow innovation diffusion and moderate market expansion.

Japan Pacemakers Market (2026-32) Segmentation Analysis:

The Japan Pacemakers Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Product Type:

- Implantable Pacemakers

- External Pacemakers

The implantable pacemakers hold the top spot in the Japan Pacemakers Market, with a market share of around 80%. This segment is maintaining its leadership due to the underscoring of its status as the definitive solution for long-term cardiac rhythm management.

Their dominance reflects the clinical reality that most pacing indications in Japan, such as chronic bradycardia, advanced atrioventricular block, and conduction disturbances associated with heart failure, require permanent, continuous therapy rather than temporary intervention.

External pacemakers are largely confined to short-term use in acute care settings, including perioperative support and emergency stabilization, limiting their role in routine cardiology practice.

Japan’s demographic structure further reinforces this imbalance. The country’s rapidly ageing population exhibits a higher incidence of degenerative conduction disorders and recurrent arrhythmias, conditions that necessitate durable, lifelong pacing solutions. Implantable systems deliver multi-year functionality, stable rhythm correction, and sophisticated features such as rate modulation and atrioventricular synchrony, enabling superior clinical outcomes and reduced re-hospitalization risk.

Ongoing innovation, including leadless and minimally invasive implantable platforms, has enhanced procedural safety and patient acceptance, further entrenching implantable pacemakers as the standard of care. These structural and clinical advantages collectively sustain their overwhelming market leadership.

Based on End User:

- Hospitals & Cardiac Centers

- Ambulatory Surgical Centers

- Others

The hospitals & cardiac centers lead the Japan Pacemakers Industry, accounting for 75% of the market size, underscoring their structural dominance in the country’s cardiac care ecosystem.

Pacemaker implantation is a high-acuity procedure that requires advanced electrophysiology infrastructure, catheterization laboratories, perioperative imaging, and immediate access to critical care support. Such capabilities are concentrated almost exclusively within tertiary hospitals and government-designated cardiovascular institutes.

Japan’s referral-driven healthcare model further reinforces this dominance. Patients with suspected arrhythmias, conduction disorders, or advanced heart failure are systematically routed to hospital-based cardiology departments for definitive diagnosis and interventional management. These institutions perform comprehensive pre-procedural evaluations, including electrophysiological studies, continuous rhythm monitoring, and imaging-guided planning, followed by implantation and structured post-operative surveillance.

Hospitals also serve as the primary gateways for technological adoption. The deployment of advanced systems, such as leadless and dual-chamber pacemakers, requires specialized operator training, catheter-based delivery platforms, and emergency surgical backup, conditions rarely met in outpatient environments.

Additionally, reimbursement pathways and clinical governance frameworks are more efficiently aligned within hospital settings, enabling higher procedural volumes and standardized care pathways. Collectively, these structural, clinical, and regulatory advantages consolidate pacemaker demand within hospitals and cardiac centers across Japan.

Gain a Competitive Edge with Our Japan Pacemakers Market Report

- Japan Pacemakers Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Japan Pacemakers Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Japan Pacemakers Market Policies, Regulations, and Product Standards

- Japan Pacemakers Market Trends & Developments

- Japan Pacemakers Market Dynamics

- Growth Drivers

- Challenges

- Japan Pacemakers Market Hotspot & Opportunities

- Japan Pacemakers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Product Type – Market Size & Forecast 2022-2032, USD Million

- Implantable Pacemakers

- External Pacemakers

- By Technology – Market Size & Forecast 2022-2032, USD Million

- Single-Chamber Pacemakers

- Dual-Chamber Pacemakers

- Biventricular Pacemakers

- By Device Platform – Market Size & Forecast 2022-2032, USD Million

- Conventional Transvenous Pacemakers

- MRI-Compatible Pacemakers

- Leadless Pacemakers

- By Component– Market Size & Forecast 2022-2032, USD Million

- Pulse Generator

- Leads

- Accessories & Programming Systems

- By Clinical Indication – Market Size & Forecast 2022-2032, USD Million

- Bradyarrhythmias

- Heart Block

- Sick Sinus Syndrome

- Atrial Fibrillation with Slow Ventricular Response

- Heart Failure (CRT Indication)

- Post-Myocardial Infarction Temporary Pacing

- Others

- Bradyarrhythmias

- By End User – Market Size & Forecast 2022-2032, USD Million

- Hospitals & Cardiac Centers

- Ambulatory Surgical Centers

- Others

- By Region

- Hokkaido

- Tohoku

- Kanto

- Chubu

- Rest of Japan

- By Company

- Company Revenue Shares

- Competitor Characteristics

- By Product Type – Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Implantable Pacemakers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Technology – Market Size & Forecast 2022-2032, USD Million

- By Device Platform – Market Size & Forecast 2022-2032, USD Million

- By Component– Market Size & Forecast 2022-2032, USD Million

- By Clinical Indication – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- By Region

- Market Size & Outlook

- Japan External Pacemakers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Technology – Market Size & Forecast 2022-2032, USD Million

- By Device Platform – Market Size & Forecast 2022-2032, USD Million

- By Component– Market Size & Forecast 2022-2032, USD Million

- By Clinical Indication – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- By Region

- Market Size & Outlook

- Japan Pacemakers Market Key Strategic Imperatives for Success & Growth

- Competition Outlook

- Company Profiles

- Medtronic Plc

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Abbott Laboratories

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Boston Scientific Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Osypka Medical GmbH

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- BIOTRONIK SE & Co. KG

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- MicroPort Scientific Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Japan Lifeline Co., Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- ZOLL Medical Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Medtronic Plc

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now