Middle East Military Aircraft Modernization Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Type (Fighter Aircraft, Transport Aircraft, Helicopters, Trainer Aircraft, Unmanned Aerial Vehicles (UAVs), Special Mission Aircraft), By Modernization (Avionics, Engine Upgrade ... s, Structural Modifications / Life Extension Programs, Weapon System Upgrades, Radar & Sensor Upgrades, Communication & Networking Solutions), By Component (Software, Hardware), By End User (Air Forces, Army Aviation Units / Defense Forces, Ministries of Defense, Defense Integrators / Contractors), and others Read more

- Aerospace & Defense

- Mar 2026

- Pages 150

- Report Format: PDF, Excel, PPT

Middle East Military Aircraft Modernization Market

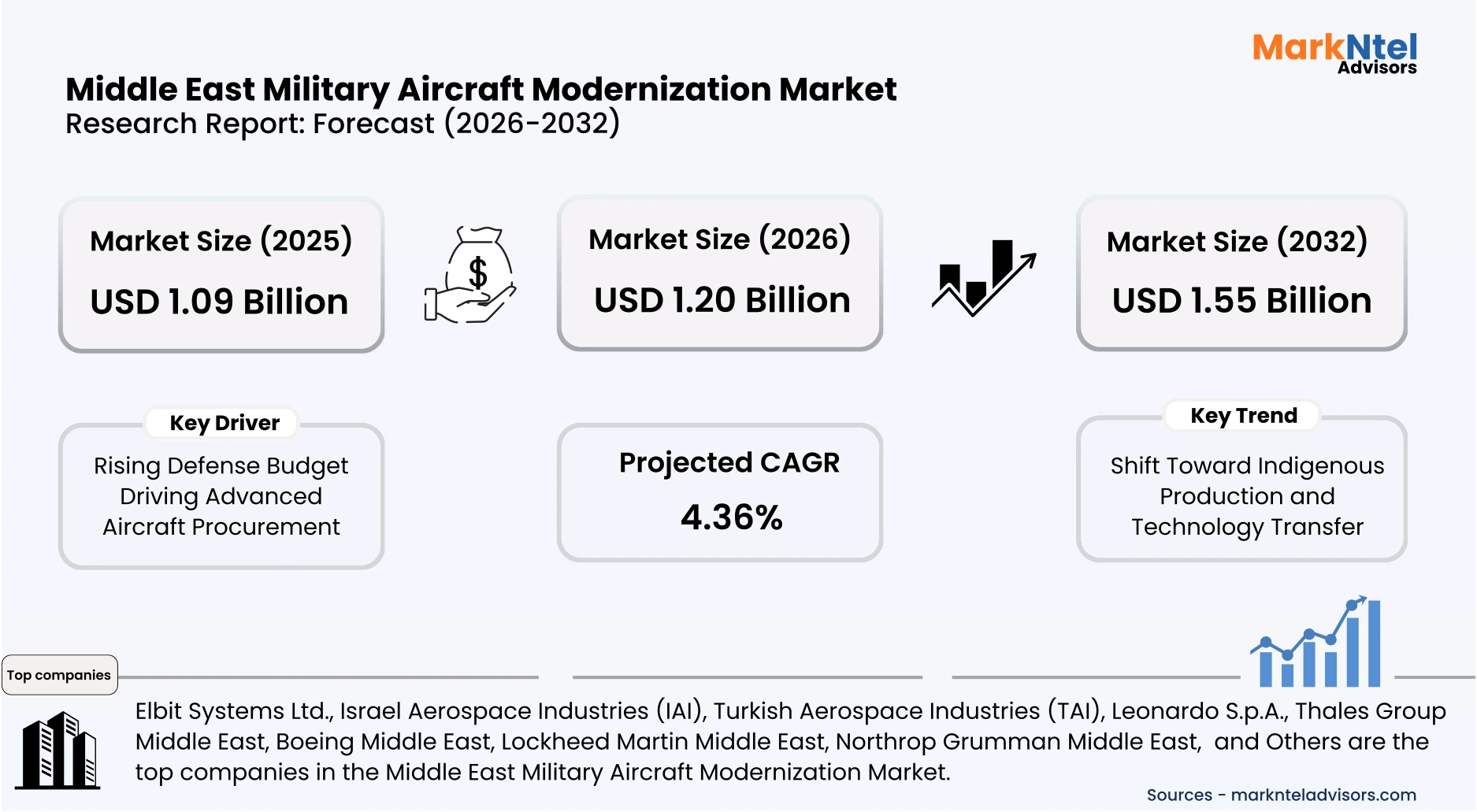

Projected 4.36% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 1.20 billion

Market Size (2032)

USD 1.55 billion

Base Year

2025

Projected CAGR

4.36%

Leading Segments

By Component: Hardware

Middle East Military Aircraft Modernization Market Report Key Takeaways:

- Market size was valued at around USD 1.09 billion in 2025 and is projected grow from USD 1.20 billion in 2026 to USD 1.55 billion by 2032. The estimated CAGR by revenue from 2026 to 2032 is around 4.36%, indicating strong growth.

- Saudi Arabia holds the largest market share of about 38% in the Middle East Military Aircraft Modernization Market in 2026.

- By Type, the Fighter Aircraft seized a significant share of about 72% in the Middle East Military Aircraft Modernization Market in 2026.

- By component, the hardware captured a significant share of about 63% in the Middle East Military Aircraft Modernization Market in 2026.

- Leading Military Aircraft Modernization Companies in the Middle East Market are Elbit Systems Ltd., Israel Aerospace Industries (IAI), Turkish Aerospace Industries (TAI), Leonardo S.p.A., Thales Group Middle East, Boeing Middle East, Lockheed Martin Middle East, Northrop Grumman Middle East, Raytheon Technologies Middle East, and Others.

Market Insights & Analysis: Middle East Military Aircraft Modernization Market (2026-32):

The Military Aircraft Modernization Market size was valued at around USD 1.09 billion in 2025 and is projected grow from USD 1.20 billion in 2026 to USD 1.55 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 4.36% during the forecast period, i.e., 2026-32.

The Middle East military aircraft modernization market has advanced significantly due to sustained government investment linked to broader strategic agendas and defense-driven economic policies. Countries across the Gulf Cooperation Council and neighboring states have continually expanded defense budgets to modernize air fleets, with Saudi Arabia significantly raising military expenditures in 2025 to approximately USD78 billion, accounting for over 7% of GDP, reinforcing long-term modernization planning under Vision 2030. Policy frameworks like Saudi Vision 2030 explicitly aim to diversify defense spending and localize production, promoting industrial participation in advanced aircraft maintenance, repair, and overhaul (MRO) and supporting national airpower capabilities.

Current conditions reflect robust procurement activity and expanding defense industrial ecosystems that reinforce end-user demand from air forces and national security agencies. At the Dubai Airshow 2025, the UAE’s Tawazun Council signed multiple defense contracts worth upwards of approximately USD4.9 billion involving aircraft maintenance, technical support, and procurement agreements, demonstrating both operational sustainment and capability enhancement across fixed-wing and rotary platforms. These deals illustrate a strong government commitment to aircraft modernization, integrating both international collaboration and domestic industrial growth, which directly influences institutional end-user segments like air force units and police aviation services.

Industry responses and strategic partnerships are forming a backbone for long-term modernization and technological integration. Saudi interest in procuring advanced platforms such as F-15EX Eagle II and potentially up to 48 F-35 stealth fighters reflects a policy-driven push to transition to next-generation systems and enhance deterrence against evolving threats. The integration of international OEMs into domestic supply chains under Vision 2030 and similar UAE initiatives creates knowledge transfer pathways, fosters local skill development, and augments maintenance and sustainment infrastructure, further sustaining demand from institutional military end-users.

Prospects remain strong, anchored in economic capacity, strategic policy alignment, and end-user operational priorities. Continued Gulf state defense allocations, diversification of supplier sources, and structured technology partnerships are expected to sustain modernization efforts well into the next decade, ensuring air forces maintain operational superiority in residential, commercial, and industrial threat environments. Moreover, formalization of deals at exhibitions like UMEX & SimTEX 2026 underscores a commitment to unmanned and advanced aircraft systems, indicating long-term demand trajectories shaped by both policy incentives and evolving end-user requirements.

Middle East Military Aircraft Modernization Market Recent Developments:

- 2026: Thales is supplying the Qatar Emiri Air Force with GM200MM/A and GM400α radars, along with a national maintenance system and operator training. The radars will enhance airspace protection and integrate with existing networks, supporting long-term operational readiness while strengthening Qatar’s sovereignty in line with the National Vision 2030.

- 2026: Leonardo DRS has partnered with SAMI and Advanced Electronic Company to locally produce advanced combat computing systems and thermal vision technologies, enhancing Saudi Arabia’s Land C2 and vehicle capabilities. The collaboration supports defense modernization, Vision 2030 goals, and the development of sustainable national defense capabilities.

Middle East Military Aircraft Modernization Market Scope:

| Category | Segments |

|---|---|

| By Type | (Fighter Aircraft, Transport Aircraft, Helicopters, Trainer Aircraft, Unmanned Aerial Vehicles (UAVs), Special Mission Aircraft), |

| By Modernization | (Avionics, Engine Upgrades, Structural Modifications / Life Extension Programs, Weapon System Upgrades, Radar & Sensor Upgrades, Communication & Networking Solutions), |

| By Component | (Software, Hardware), |

| By End User | (Air Forces, Army Aviation Units / Defense Forces, Ministries of Defense, Defense Integrators / Contractors), |

Middle East Military Aircraft Modernization Market Driver:

Rising Defense Budget Driving Advanced Aircraft Procurement

Middle Eastern nations, particularly Saudi Arabia, the UAE, and Qatar, have consistently increased defense spending over the past decade to strengthen their military capabilities. According to GlobalFirepower, the UAE allocates USD23.48 billion annually to defense, while Qatar spends USD11.95 billion, demonstrating a sustained commitment to modernizing air forces and acquiring advanced fighter jets, helicopters, and rotary-wing platforms . This financial dedication ensures that modernization programs are well-funded and aligned with national security priorities.

Government initiatives such as Saudi Vision 2030 and the UAE defense localization strategies emphasize upgrading operational readiness and fleet capabilities. Rising budgets enable acquisition of cutting-edge avionics, next-generation radar systems, and unmanned aerial platforms. Qatar, for instance, continues to invest in MALE-class drones worth USD1.96 billion for surveillance and precision strikes, while retaining options for additional Typhoon fighter jets, ensuring air forces maintain technological parity with global standards .

The impact of increased defense budgets extends beyond procurement to infrastructure, training, and maintenance of advanced aircraft. Enhanced funding allows investment in airbases, simulator programs, and pilot training, improving operational efficiency and combat readiness. Evidence from Qatar, the UAE, and neighboring states shows that rising defense expenditures directly drive demand for advanced aircraft and accelerate modernization initiatives across the region.

Middle East Military Aircraft Modernization Market Trend:

Shift Toward Indigenous Production and Technology Transfer

The Middle Eastern defense industry is increasingly moving beyond simple procurement toward indigenous production and structured technology transfer agreements to build internal industrial capability. Saudi Arabia has signed multiple aerospace manufacturing MoUs, including with Airbus to localize helicopter development and aircraft component production, aligning with Vision 2030 goals to manufacture more systems domestically .

This trend is visible beyond the Gulf, with Egypt’s Arab Organization for Industrialization entering partnerships with foreign firms at EDEX 2025 to localize UAV production, engine overhaul work, and aircraft components, while the UAE’s AMMROC signed industrial cooperation MoUs to develop aircraft structural and maintenance capabilities with Egypt’s AO I. These initiatives demonstrate active technology absorption and joint production frameworks that extend indigenous capability across fixed‑wing, rotary, and unmanned platforms.

By fostering joint ventures, MoUs, and co‑development agreements, countries in the region are strengthening workforce skills, building integrated MRO ecosystems, and enabling in‑country production lines that support long‑term aircraft modernization. This shift toward local industrialization and technology transfer enhances sovereign capabilities, reduces dependency on external suppliers for critical systems, and lays the foundation for sustainable aircraft modernization over the coming decade.

Middle East Military Aircraft Modernization Market Opportunity:

Growing Adoption of Next-Generation Combat and Surveillance Technologies

Middle Eastern air forces are increasingly acquiring next‑generation combat aircraft and surveillance platforms to enhance deterrence and operational capability amid evolving threat environments. Saudi Arabia is advancing negotiations to acquire JF‑17 Block III fighter jets valued at around USD2 billion, reflecting a pivot toward diversified and modernized combat fleets.

The race for cutting‑edge airborne surveillance is also accelerating, with SAAB formally offering its advanced GlobalEye AEW&C aircraft to Saudi Arabia to provide long‑range intelligence, surveillance, and reconnaissance (ISR) capability against drone and missile threats . The UAE already operates a growing fleet of GlobalEye AEW&C platforms, significantly enhancing regional situational awareness and early warning capacity .

Unmanned aerial systems represent another high‑growth segment, with the UAE signing approximately USD403 million in local UAV contracts at UMEX 2026, including heavy‑lift drones and R&D for advanced UAV platforms . These developments demonstrate robust adoption of autonomous surveillance and combat systems alongside traditional fighter jets.

The convergence of advanced manned and unmanned technologies positions the Middle East as a key growth hub for combat and ISR innovation. This creates significant opportunities for defense manufacturers and system integrators that can deliver high‑end aircraft, AEW&C platforms, and sensor‑rich UAVs, aligning with national modernization visions and enhancing air force interoperability across the region.

Middle East Military Aircraft Modernization Market Challenge:

Dependence on Foreign Suppliers for Critical Systems

Despite significant modernization efforts, Middle Eastern nations remain heavily reliant on foreign suppliers for critical aircraft, avionics, engines, and weapon systems. Countries such as Qatar and Saudi Arabia source advanced fighter jets, drones, and air-defense systems from the U.S., France, and the U.K., which exposes procurement programs to delays, export restrictions, and geopolitical uncertainties.

This dependence limits flexibility in upgrades, fleet expansion, and timely integration of emerging technologies. Maintenance, repair, and overhaul (MRO) activities often require specialized foreign expertise, while licensing restrictions can slow the adoption of cutting-edge systems. Even localized production initiatives cannot fully replace imported components, creating structural vulnerability in long-term modernization plans.

Geopolitical tensions and conflict periods further exacerbate the risk. High-value U.S. arms sales totaling nearly USD 16 billion to Israel and Saudi Arabia amid regional tensions in early 2026 highlight how Middle Eastern militaries continue to rely on foreign suppliers to maintain operational readiness during crise s. According to SIPRI data, 66% of Israel’s major arms imports in 2020–24 were supplied by the U.S., including aircraft, missiles, armored vehicles, and air-defense systems, while Germany and Italy supplied naval platforms and F‑35 components. These transfers, funded through both direct purchases and long-term U.S. military assistance, emphasize the structural dependence on external suppliers for operational capability .

Such reliance underscores the ongoing challenge for Middle Eastern air forces to achieve self-sufficiency and resilient defense capabilities. Even with regional modernization programs and localization efforts, countries remain vulnerable to supply chain disruptions, export restrictions, and geopolitical fluctuations that could delay critical deliveries of aircraft, munitions, and advanced systems during periods of heightened tension or conflict.

Middle East Military Aircraft Modernization Market (2026-32) Segmentation Analysis:

The Middle East Military Aircraft Modernization Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Type:

- Fighter Aircraft

- Transport Aircraft

- Helicopters

- Trainer Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Special Mission Aircraft

The fighter aircraft dominates the Middle East Military Aircraft Modernization Market, holding around 72% market share, as advanced combat jets constitute the cornerstone of regional air power and strategic deterrence. Fighter aircraft provide critical capabilities, including air superiority, precision strike, and multi-role operations, which are unmatched by other platform types. Recent deliveries of French Rafale fighters to the UAE in early 2025 highlight sustained investments in modern combat fleets to maintain operational readiness and technological parity .

Regional defense strategies further reinforce the prioritization of fighter aircraft. Saudi Arabia is evaluating major procurements of F‑15EX Eagle II jets and potentially up to 48 F‑35 stealth fighters, demonstrating a strategic focus on modernizing frontline combat capabilities and enhancing force projection . These acquisitions drive long-term demand for upgrades, integrated avionics, weapons systems, and pilot training, ensuring the fighter aircraft segment maintains a dominant position in modernization spending.

Operational deployment and multinational exercises further underscore the centrality of fighters in regional air operations. Exercises such as Saudi Arabia’s Spears of Victory‑2026, involving F‑16 Block‑52 jets from Pakistan and Gulf partners, illustrate the strategic and interoperability significance of combat aircraft . Collectively, sustained procurement, active utilization, and multinational collaboration reinforce the fighter aircraft segment as the primary driver of the Middle East Military Aircraft Modernization Market.

Based on Component:

- Software

- Hardware

The hardware segment dominates the Middle East Military Aircraft Modernization Market, with 63% market share, because core physical systems such as avionics suites, radar arrays, electro‑optical sensors, and integrated mission computers are fundamental to the performance and modernization of military aircraft. These tangible hardware components enable critical operational functions, including surveillance, navigation, targeting, communication, and electronic warfare, that are essential for both legacy upgrades and next‑generation platforms. As regional militaries expand and modernize their fleets, priority is given to procuring robust hardware solutions that enhance survivability and situational awareness.

In defense exhibition highlights this underlying demand, with major hardware technologies taking center stage at events like Dubai Airshow 2025. At the show, defense electronics firm ASELSAN signed key contracts and memoranda of understanding with Emirati partners for advanced avionics, situational awareness systems, and airborne payload integrations , reflecting strong interest in mission‑critical hardware components across manned and unmanned platforms. These agreements underscore the priority placed on procuring avionics and radar systems that directly impact operational readiness and interoperability.

Furthermore, the persistence of airborne surveillance requirements reinforces the hardware segment’s leading role. Swedish manufacturer Saab actively pitched its GlobalEye surveillance aircraft to Qatar and Saudi Arabia, demonstrating strong regional interest in airborne early warning and control capabilities that rely on sophisticated radar and sensor hardware . Such platforms not only enhance airspace monitoring but also integrate complex hardware suites that drive procurement volumes.

The dominance of hardware is also reinforced by its cross‑platform applicability and lifecycle demands: radar systems, avionics, and mission computers are compatible across fighter jets, ISR aircraft, and unmanned systems, generating sustained demand for upgrades, spares, and integration services. Combined with ongoing regional modernization roadmaps and expanding defense budgets, the operational necessity and repeat acquisition cycles of hardware components solidify this segment as the leading contributor within the Middle East Military Aircraft Modernization Market.

Middle East Military Aircraft Modernization Market (2026-32): Regional Projection

Saudi Arabia dominates the Middle East Military Aircraft Modernization Market with an estimated 38% share because it represents the region’s largest and most sustained investment base in aerial combat capability expansion. The Kingdom has prioritized large‑scale aircraft modernization and sustainment within its defense strategy, reinforcing airpower as a central pillar of national security. This commitment is reflected in ongoing contracts such as a USD49.7 million Boeing sustainment agreement for its existing F‑15 fighter fleet, ensuring high availability and extended operational life for one of the region’s most numerous combat platforms.

This procurement drive is complemented by the continuous modernization of existing platforms and robust multinational cooperation. The Royal Saudi Air Force operates a large and diversified combat fleet that includes upgraded F‑15SA/SR variants, Eurofighter Typhoons, and potentially next‑generation fighters, positioning it ahead of most regional peers in terms of capability and scale. Participation in major exercises such as Spears of Victory‑2026 alongside allied air forces further underscores Riyadh’s operational emphasis on fighter readiness and interoperability .

Saudi Arabia’s dominant share also reflects its broader strategic defense posture, which prioritizes airpower as a deterrent against regional threats and as a tool for power projection. By investing heavily in advanced aircraft procurement, infrastructure, and potential future procurements, including stealth and next‑generation platforms, Riyadh reinforces its role as the primary driver of military aviation modernization across the Middle East, sustaining long‑term demand and securing its leadership position in the market.

Gain a Competitive Edge with Our Middle East Military Aircraft Modernization Market Report:

- Middle East Military Aircraft Modernization Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Middle East Military Aircraft Modernization Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Middle East Military Aircraft Modernization Market Policies, Regulations, and Product Standards

- Middle East Military Aircraft Modernization Market Trends & Developments

- Middle East Military Aircraft Modernization Market Dynamics

- Growth Factors

- Challenges

- Middle East Military Aircraft Modernization Market Hotspot & Opportunities

- Middle East Military Aircraft Modernization Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Fighter Aircraft

- Transport Aircraft

- Helicopters

- Trainer Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Special Mission Aircraft

- By Modernization- Market Size & Forecast 2022-2032, USD Million

- Avionics

- Engine Upgrades

- Structural Modifications / Life Extension Programs

- Weapon System Upgrades

- Radar & Sensor Upgrades

- Communication & Networking Solutions

- By Component- Market Size & Forecast 2022-2032, USD Million

- Software

- Hardware

- By End User- Market Size & Forecast 2022-2032, USD Million

- Air Forces

- Army Aviation Units / Defense Forces

- Ministries of Defense

- Defense Integrators / Contractors

- By Country

- Saudi Arabia

- UAE

- Qatar

- Kuwait

- Oman

- Israel

- South Africa

- Egypt

- Rest of the Middle East

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Military Aircraft Modernization Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Modernization- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Military Aircraft Modernization Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Modernization- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Qatar Military Aircraft Modernization Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Modernization- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kuwait Military Aircraft Modernization Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Modernization- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Oman Military Aircraft Modernization Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Modernization- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Israel Military Aircraft Modernization Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Modernization- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- South Africa Military Aircraft Modernization Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Modernization- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Egypt Military Aircraft Modernization Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Modernization- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Middle East Military Aircraft Modernization Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Elbit Systems Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Israel Aerospace Industries (IAI)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Turkish Aerospace Industries (TAI)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Leonardo S.p.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thales Group Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Boeing Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lockheed Martin Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Northrop Grumman Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Raytheon Technologies Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elbit Systems Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now