Europe Mental Health Apps Market Research Report: Forecast (2026-2032)

Europe Mental Health Apps Market - By Type / Functionality (Cognitive Behavioral Therapy (CBT) Apps, Mood Tracking & Self-Assessment Apps, Meditation & Mindfulness Apps, AI / Chatb ... ot-Based Mental Health Apps, Gamified Mental Health Apps, Community & Peer Support Apps), By Platform (iOS, Android, Others), By Revenue Model (Subscription-Based, Freemium, One-Time Purchase, In-App Purchases, B2B / Enterprise Licensing, Reimbursement-Based (Public or Insurance), Others) By Age Group (Children & Adolescents, Adults, Geriatric Population), By Application (Depression & Anxiety Management, Stress Management, Meditation & Mindfulness, Wellness & General Mental Well-Being, Sleep Disorder Management, PTSD & Trauma Management, Addiction & Substance Abuse Support, Other Mental Health Conditions), By End User (Individuals / Consumers, Healthcare Providers, Employers / Corporates, Public Health Systems, Insurers & Payers), and others Read more

- Healthcare

- Dec 2025

- Pages 165

- Report Format: PDF, Excel, PPT

Europe Mental Health Apps Market

Projected 9.83 % CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 1.52 Billion

Market Size (2032)

USD 2.93 Billion

Base Year

2025

Projected CAGR

9.83 %

Leading Segments

By Platform: iOS

Europe Mental Health Apps Market Report Key Takeaways:

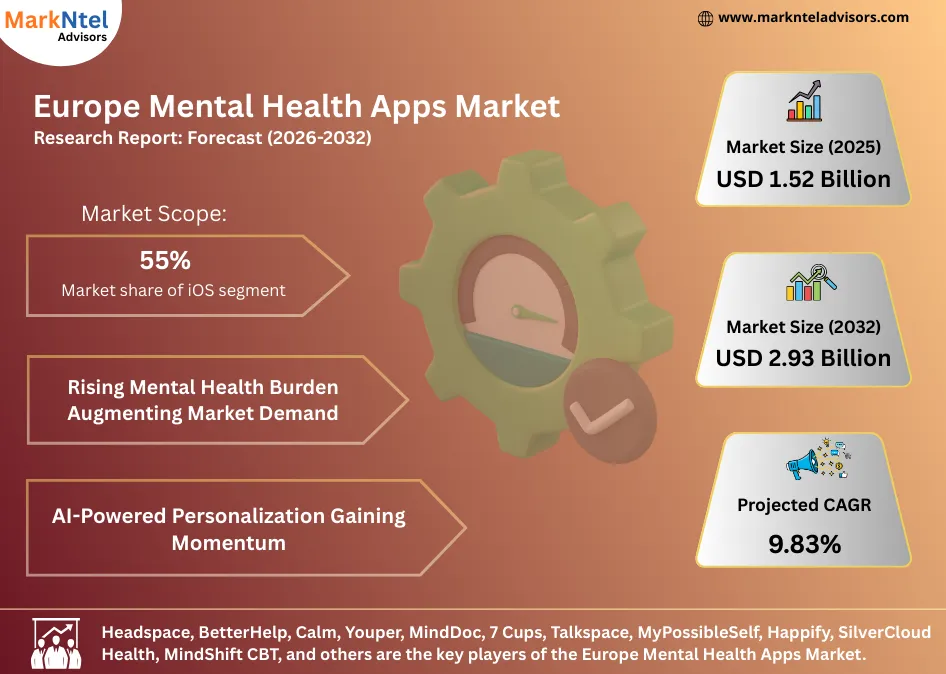

- The Europe Mental Health Apps Market size is valued at around USD 1.52 billion in 2025 and is projected to reach USD 2.93 billion by 2032. The estimated CAGR from 2026 to 2032 is around 9.83%, indicating strong growth.

- By platform, the iOS segment represented 55% of the Europe Mental Health Apps Market size in 2025.

- By end user, the individuals/consumers represented 60% of the Europe Mental Health Apps Market size in 2025.

- By Application, the depression and anxiety represented 29% of the Europe Mental Health Apps Market size in 2025.

- By Country, Germany leads the Europe Mental Health Apps Market with a dominant 19% share in 2025; meanwhile, the Nordics are the fastest-growing during 2026-32.

- The leading mental health apps companies in Europe are Headspace, BetterHelp, Calm, Youper, MindDoc, 7 Cups, Talkspace, MyPossibleSelf, Happify, SilverCloud Health, MindShift CBT, and others.

Market Insights & Analysis: Europe Mental Health Apps Market (2026- 2032):

The Europe Mental Health Apps Market size is valued at around USD 1.52 billion in 2025 and is projected to reach USD 2.93 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 9.83 % during the forecast period, i.e., 2026-32.

The Europe Mental Health Apps Market is experiencing rapid growth, driven by rising mental health conditions and the adoption of AI-powered personalization. Increasing anxiety, depression, and stress are boosting demand for accessible digital care, while data-driven interventions enhance engagement, effectiveness, and scalability across the region.

A Mental Health in Europe 2025 overview indicates that mental disorder prevalence across the EU27 and the UK remains elevated at 16.5%, with anxiety disorders increasing by 43.9% and depression cases rising by 22.3%. These trends signal a deepening and long-term demand for scalable mental health support beyond traditional clinical settings.

Workplace mental health pressures further reinforce market expansion. The EU-OSHA World Mental Health Day 2025 survey reports that 29% of EU workers experience stress, anxiety, or depression, representing a sizeable population increasingly underserved by conventional, in-person care models. Complementing this, the European Parliamentary Research Service highlights that 54% of Europeans with mental health conditions have not accessed professional support, underscoring systemic capacity constraints and reinforcing the role of digital applications in extending care reach.

Youth mental health is a critical factor shaping future demand. The European Parliament Report A9-0367/2023 estimates that over 150 million Europeans live with a mental health condition, with mental disorders being the leading cause of years lived with disability in the EU. Nearly 70% lack timely intervention, while suicide is the second leading cause of death among Western European adolescents aged 15–19, underscoring the need for early, accessible digital support.

Innovation and public investment are reinforcing market maturity. AI-powered personalization is being actively deployed by companies such as Headspace, which integrates generative AI into its meditation and professional care offerings; Wysa, delivering AI-driven CBT, DBT, and mindfulness support; Youper, combining conversational AI with clinically validated techniques; and Mindsera, using AI-powered journaling to generate emotional insights from user inputs. These developments align with substantial public funding, including the EU4Health 2021–2027 budget of approximately USD 5 billion and the European Commission’s Comprehensive Approach to Mental Health, backed by USD 1.5 billion through 2027 to support prevention, care, and digital integration.

Furthermore, depression and anxiety account for 29% of application usage as they are the most prevalent mental health conditions, require continuous self-management, and are well-suited to app-based CBT, mood tracking, and on-demand, personalized interventions.

Collectively, the rising mental health burden, persistent access gaps, and increasing reliance on AI-driven personalization are reshaping mental healthcare delivery across Europe. Supported by strong public funding frameworks and accelerating innovation, mental health apps are evolving from supplementary tools into integral components of care delivery, positioning the market for sustained and structurally driven growth in the coming years.

Europe Mental Health Apps Market Recent Developments:

- December 2025: Wysa has launched expanded multilingual capabilities for its clinically validated digital mental health support platform, now offering services in French, German, Italian, Arabic, Japanese, and Brazilian Portuguese alongside English, Spanish, and Hindi. This enhancement enables organizations to deliver more inclusive, culturally relevant mental health care across Europe and globally.

- November 2025: HelloBetter has officially introduced Ello, a new AI-driven companion designed to support everyday mental and emotional well-being. Developed in collaboration with psychologists and data scientists, Ello provides 24/7 conversational support, encourages self-reflection, and integrates safety features with human-in-the-loop access to clinical assistance when needed. The app is GDPR-compliant and designed for accessible, evidence-based support, without attempting to make diagnoses.

Europe Mental Health Apps Market Scope:

| Category | Segments |

|---|---|

| By Type / Functionality | Cognitive Behavioral Therapy (CBT) Apps, Mood Tracking & Self-Assessment Apps, Meditation & Mindfulness Apps, AI / Chatbot-Based Mental Health Apps, Gamified Mental Health Apps, Community & Peer Support Apps), |

| By Platform | iOS, Android, Others), |

| By Revenue Model | Subscription-Based, Freemium, One-Time Purchase, In-App Purchases, B2B / Enterprise Licensing, Reimbursement-Based (Public or Insurance), Others) |

| By Age Group | Children & Adolescents, Adults, Geriatric Population), |

| By Application | Depression & Anxiety Management, Stress Management, Meditation & Mindfulness, Wellness & General Mental Well-Being, Sleep Disorder Management, PTSD & Trauma Management, Addiction & Substance Abuse Support, Other Mental Health Conditions), |

| By End User | Individuals / Consumers, Healthcare Providers, Employers / Corporates, Public Health Systems, Insurers & Payers), and others |

Europe Mental Health Apps Market Drivers:

Rising Mental Health Burden Augmenting Market Demand

The escalating mental-health burden across Europe represents a fundamental driver of demand for digital mental-health applications, as existing healthcare systems struggle to address growing population-level needs.

The World Health Organization (WHO) estimates that one in six individuals in the European Region lives with a mental-health condition, underscoring the structural scale of the challenge. This burden has intensified in the post-pandemic period, with depression and anxiety among young people increasing by approximately 25%, sharply elevating demand for accessible, continuous, and preventive mental-health support.

Population-wide data further reinforce this demand trend. The Eurobarometer survey reported that 46% of Europeans experienced emotional or psychosocial difficulties such as anxiety, stress, or depressive symptoms within the preceding 12 months. Such widespread self-reported distress highlights the limitations of conventional, appointment-based care models and strengthens the case for scalable, technology-enabled interventions that can reach users early and at low cost.

Beyond immediate demand pressures, public funding is reinforcing long-term market growth. The EU4Health programme allocated USD 21.7 million to mental-health promotion in 2023, while Horizon Europe 2025 prioritizes AI-driven and digital health innovations, accelerating integration of mental-health applications.

As mental-health prevalence rises and public health systems prioritize digital care delivery, the growing mental-health burden will continue to drive sustained adoption and expansion of mental-health apps across Europe.

Europe Mental Health Apps Market Trends:

AI-Powered Personalization Gaining Momentum

AI-powered personalization is emerging as a defining trend in Europe’s digital mental-health landscape, enabling more responsive and individualized care delivery. The European Commission actively promotes AI adoption in healthcare to enhance clinical outcomes and system sustainability. Through initiatives such as GenAI4EU, the EU has committed USD 819 million under Horizon Europe and Digital Europe programmes to scale AI-enabled health solutions, including personalized digital mental-health interventions.

Public health organizations are also advancing this shift. For instance, Mental Health Europe launched a 2025 study on AI in mental healthcare, highlighting AI’s ability to personalize therapeutic pathways, enhance diagnostic accuracy, and support early, context-aware interventions tailored to individual needs.

At the national level, UK government-backed innovation programmes are funding AI-enabled tools such as smart glasses and AI-driven applications that provide real-time mental-health support for individuals experiencing anxiety and depression, reinforcing public-sector confidence in personalized digital care.

On the commercial front, Woebot Health leverages NLP-driven daily check-ins to tailor CBT-based guidance according to individual emotional patterns, while Earkick integrates real-time biometric signals with conversational AI to dynamically adjust mental-health support.

With strong EU-level funding, government-led pilots, and rapid enterprise adoption, AI-powered personalization is enhancing the relevance, engagement, and effectiveness of mental-health apps, positioning them as a key trend for sustained market growth across Europe.

Europe Mental Health Apps Market Challenges:

Data Privacy & Regulatory Compliance

Digital mental health app providers in Europe face rising compliance costs due to an increasingly complex regulatory landscape. The European Health Data Space, effective March 2025, introduces strict requirements for health data access, security, consent, and cross-border interoperability, significantly increasing technical and operational burdens for developers.

Further complexity arises from the EU Artificial Intelligence Act, in force since August 2024, which classifies many AI-enabled healthcare solutions as “high-risk.” This designation mandates extensive conformity assessments, transparent algorithms, human oversight mechanisms, and high-quality training datasets, collectively extending development timelines and inflating certification and compliance expenditures.

Regulatory enforcement under GDPR remains substantial. As of March 2025, cumulative fines across sectors have reached approximately USD 6.22 billion, with high-profile penalties such as the USD 33.6 million sanction against Clearview AI underscoring strict supervisory scrutiny.

Additionally, national reimbursement pathways such as Germany’s DiGA fast-track require robust clinical evidence alongside rigorous data-protection compliance, further raising entry thresholds.

Heightened regulatory scrutiny, rising compliance costs, and complex approval pathways are slowing innovation cycles and discouraging smaller developers, thereby constraining the pace of market expansion despite strong underlying demand.

Europe Mental Health Apps Market (2026-32) Segmentation Analysis:

The Europe Mental Health Apps Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Platform

- iOS

- Android

- Others

The iOS segment now holds the top spot in the Europe Mental Health Apps Market, accounting for 55% market share, supported by a combination of user demographics, ecosystem maturity, and regulatory readiness.

iOS devices have higher penetration among premium smartphone users in Western Europe, including professionals and younger adults who show a stronger willingness to pay for subscription-based wellness and mental-health applications.

Apple’s integrated ecosystem, encompassing iPhone, Apple Watch, and HealthKit, enables seamless data collection, secure health-data management, and advanced personalization, which are critical for mental-health use cases.

From a compliance perspective, iOS is often preferred by developers due to Apple’s strong privacy architecture, encrypted data handling, and standardized app review processes that align well with GDPR and emerging EU health-data regulations. Additionally, iOS users demonstrate higher engagement rates and longer session durations, improving clinical adherence and monetization outcomes for app providers.

Android continues to expand through wider device accessibility, but iOS’s combination of security, user trust, and monetization efficiency firmly positions it as the leading platform in Europe’s mental-health app ecosystem.

Based on End User

- Individuals / Consumers

- Healthcare Providers

- Employers / Corporates

- Public Health Systems

- Insurers & Payers

The individuals/consumers category leads the Europe Mental Health Apps Industry, accounting for 60% market share, primarily due to direct-to-consumer adoption. Rising awareness of mental well-being, combined with increasing prevalence of anxiety, stress, and depression, has encouraged individuals to seek immediate, self-guided support beyond traditional clinical settings.

Mental health apps offer privacy, flexibility, and on-demand access, which strongly appeals to users reluctant to pursue in-person therapy due to stigma, cost, or long waiting times. Subscription-based models, freemium access, and personalised AI-driven features such as mood tracking, CBT exercises, and guided mindfulness further enhance consumer uptake.

Additionally, widespread smartphone penetration and familiarity with wellness apps have normalized self-care-oriented digital solutions. Younger demographics and working professionals, in particular, favor app-based mental health support for its convenience and autonomy, reinforcing the dominance of individual consumers as the primary end-user segment in Europe.

Europe Mental Health Apps Market (2026-32): Regional Projection

The Europe Mental Health Apps Market is dominated by Germany, which holds a commanding 19% market share, driven by strong institutional support, high digital health adoption, and structured reimbursement pathways.

The country’s Digital Healthcare Act (DVG) and the DiGA fast-track system enable certified mental health apps to be prescribed and reimbursed through statutory health insurance, significantly accelerating adoption among both clinicians and patients.

Germany also benefits from a large, digitally literate population, rising mental health awareness, and increasing prevalence of stress-related and anxiety disorders. Strong data protection standards and clinical validation requirements have fostered trust in regulated digital therapeutics, encouraging sustained usage.

Meanwhile, the Nordic countries are the fastest-growing due to advanced digital infrastructure, high smartphone penetration, progressive public healthcare systems, and early adoption of AI-enabled, preventive mental health solutions.

Overall, Germany’s combination of progressive regulation, reimbursement-backed adoption, and high consumer trust has positioned it as the most mature and commercially attractive market for mental health apps in Europe, setting a benchmark for scalable and regulated digital mental healthcare across the region.

Gain a Competitive Edge with Our Europe Mental Health Apps Market Report

- Europe Mental Health Apps Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Europe Mental Health Apps Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Market Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Mental Health Apps Market Trends & Development

- Europe Mental Health Apps Market Dynamics

- Growth Drivers

- Challenges

- Europe Mental Health Apps Market Regulations, Policies & Standards

- Europe Mental Health Apps Market Hotspots & Opportunities

- Europe Mental Health Apps Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type / Functionality - Market Size & Forecast 2022-2032, USD Million

- Cognitive Behavioral Therapy (CBT) Apps

- Mood Tracking & Self-Assessment Apps

- Meditation & Mindfulness Apps

- AI / Chatbot-Based Mental Health Apps

- Gamified Mental Health Apps

- Community & Peer Support Apps

- By Platform - Market Size & Forecast 2022-2032, USD Million

- iOS

- Android

- Others

- By Revenue Model - Market Size & Forecast 2022-2032, USD Million

- Subscription-Based

- Freemium

- One-Time Purchase

- In-App Purchases

- B2B / Enterprise Licensing

- Reimbursement-Based (Public or Insurance)

- Others

- By Age Group - Market Size & Forecast 2022-2032, USD Million

- Children & Adolescents

- Adults

- Geriatric Population

- By Application - Market Size & Forecast 2022-2032, USD Million

- Depression & Anxiety Management

- Stress Management

- Meditation & Mindfulness

- Wellness & General Mental Well-Being

- Sleep Disorder Management

- PTSD & Trauma Management

- Addiction & Substance Abuse Support

- Other Mental Health Conditions

- By End User - Market Size & Forecast 2022-2032, USD Million

- Individuals / Consumers

- Healthcare Providers

- Employers / Corporates

- Public Health Systems

- Insurers & Payers

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics

- Rest of Europe

- By Company

- Competition Characteristics

- Market Share of Leading Companies

- By Type / Functionality - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Germany Mental Health Apps Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type / Functionality - Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model - Market Size & Forecast 2022-2032, USD Million

- By Age Group - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- The United Kingdom Mental Health Apps Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type / Functionality - Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model - Market Size & Forecast 2022-2032, USD Million

- By Age Group - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- France Mental Health Apps Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type / Functionality - Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model - Market Size & Forecast 2022-2032, USD Million

- By Age Group - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Italy Mental Health Apps Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type / Functionality - Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model - Market Size & Forecast 2022-2032, USD Million

- By Age Group - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Spain Mental Health Apps Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type / Functionality - Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model - Market Size & Forecast 2022-2032, USD Million

- By Age Group - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Netherlands Mental Health Apps Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type / Functionality - Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model - Market Size & Forecast 2022-2032, USD Million

- By Age Group - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Nordics Mental Health Apps Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type / Functionality - Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model - Market Size & Forecast 2022-2032, USD Million

- By Age Group - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Europe Mental Health Apps Market Key Strategic Imperatives for Growth & Success

- Competition Outlook

- Company Profiles

- Headspace

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- BetterHelp

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Calm

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Youper

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- MindDoc

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- 7 Cups

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Talkspace

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- MyPossibleSelf

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Happify

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- SilverCloud Health

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Thrive Therapeutic Software

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- MindShift CBT

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Headspace

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now