India Heat Exchanger Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Product Type (Shell & Tube Heat Exchangers, Plate Heat Exchangers, Air Cooled Heat Exchangers, Finned Tube Heat Exchangers, others), By End-User / Industry (Power Generation, Ch ... emical & Petrochemical, Oil & Gas, Automotive & Manufacturing, Food & Beverage / Pharma, HVAC / Building Services, others), By Application (Process Heating / Cooling, Energy Recovery / Waste Heat Recovery, Refrigeration & Air Conditioning, Steam Condensation / Boiler Systems, others), By Material Type (Stainless Steel, Carbon Steel, Copper, Aluminum, others), and others Read more

- Energy

- Mar 2026

- Pages 145

- Report Format: PDF, Excel, PPT

India Heat Exchanger Market

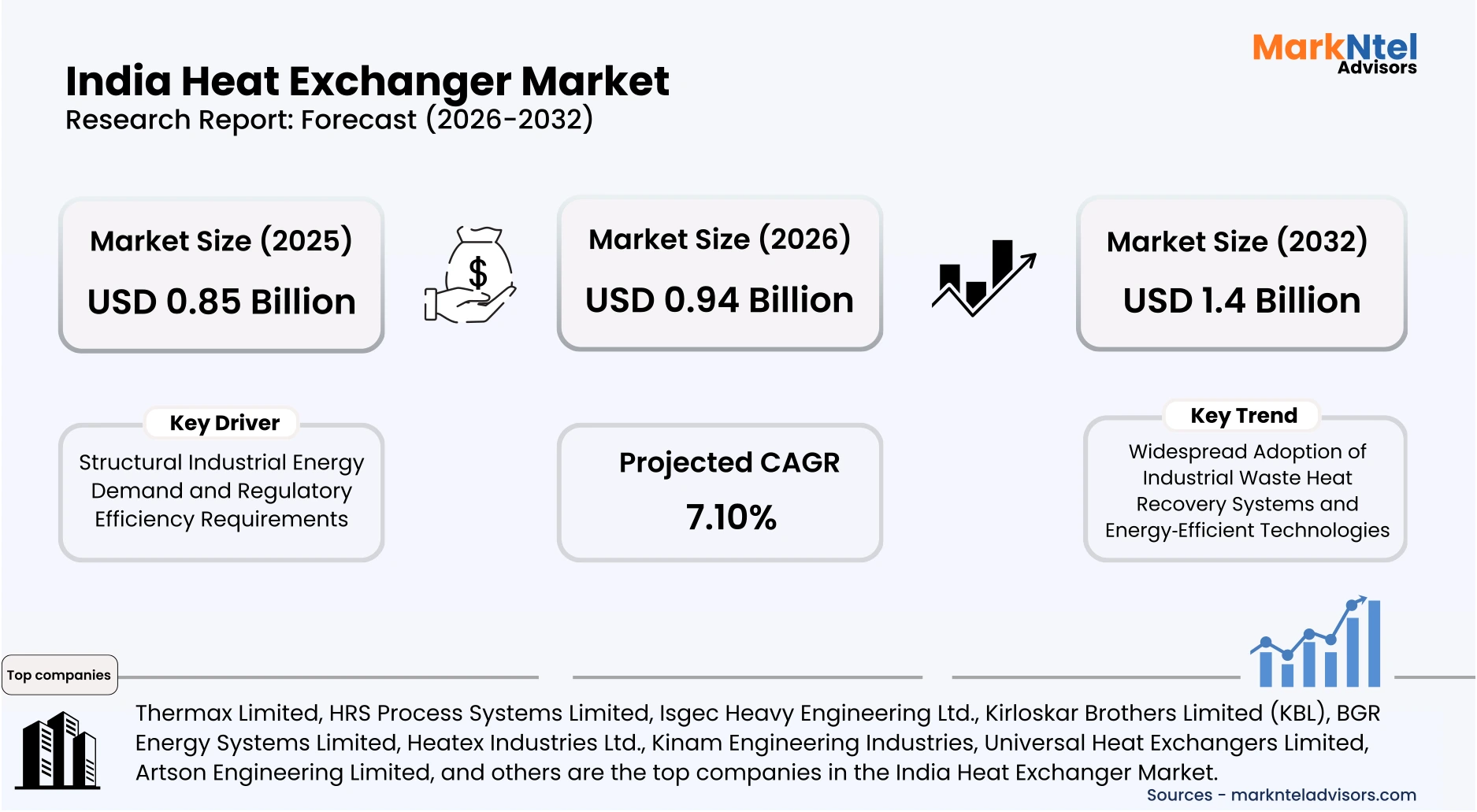

Projected 7.10 % CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 0.94 Billion

Market Size (2032)

USD 1.4 Billion

Base Year

2025

Projected CAGR

7.10 %

Leading Segments

By Product Type: Shell & Tube Heat Exchangers

India Heat Exchanger Market Report Key Takeaways:

- The India Heat Exchanger market size was valued at USD 0.85 billion in 2025 and is projected to grow from USD 0.94 billion in 2026 to USD 1.4 billion by 2032, exhibiting a CAGR of 7.10 % during the forecast period.

- Maharashtra is the leading state with a significant share of 20% in 2026.

- By Product type, the shell and tube heat exchangers represented a significant share of about 53% in the India Heat Exchanger Market in 2026.

- By material type, the stainless-steel segment presented a significant share of about 40% in the India Heat Exchanger Market in 2026.

- Leading companies in the market are Thermax Limited, HRS Process Systems Limited, Isgec Heavy Engineering Ltd., Kirloskar Brothers Limited (KBL), BGR Energy Systems Limited, Heatex Industries Ltd., Kinam Engineering Industries, Universal Heat Exchangers Limited, Artson Engineering Limited, and Others.

Market Insights & Analysis: India Heat Exchanger Market (2026-32):

The India Heat Exchanger market size was valued at USD 0.85 billion in 2025 and is projected to grow from USD 0.94 billion in 2026 to USD 1.4 billion by 2032, exhibiting a CAGR of 7.10 % during the forecast period. i.e., 2026-32.

India’s heat exchanger market has shown resilient growth driven by expanding industrial activity and stringent energy use standards in recent years. Industrial expansion in core sectors such as chemicals, power generation, and manufacturing has increased demand for thermal management equipment that enhances process efficiency and reduces energy costs. According to government energy efficiency frameworks, industrial waste heat recovery systems have been linked with energy savings of up to 20–30% in energy‑intensive sectors, emphasizing the role of thermal technologies in cost and carbon mitigation.

Economic infrastructure development, urbanization, and modernization of manufacturing facilities have underpinned increased deployment of advanced heat exchangers across key industrial hubs. The Bureau of Energy Efficiency (BEE) has rolled out focused energy efficiency programs targeting industrial clusters and MSMEs, earmarking significant funds for interest subvention and capacity‑building to adopt high‑efficiency technologies. The Andhra Pradesh rollout of pilot heat pump systems under a state‑led energy efficiency program further signals rising acceptance of efficient heating and cooling solutions beyond conventional industrial use .

Recent regulatory and policy developments in India are strengthening the market’s foundation by promoting indigenous industrial growth and sustainability. State‑level industrial policies, for example, in Punjab, are offering flexible incentive packages for modernization of production lines, while national schemes under the Bureau of Energy Efficiency support energy conservation technologies and performance standards for thermal equipment. These initiatives reduce the cost burden of technology upgrades and align industrial energy use with broader national targets for emissions reduction and sustainable manufacturing.

Looking forward, the heat exchanger market’s prospects remain positive as India advances its energy transition and infrastructure agenda. Investments in energy‑efficient systems and renewable energy integration are expected to drive consistent demand for specialized heat transfer equipment in diverse industries. Furthermore, the increasing number of large data centers and urban cooling infrastructure in India is creating opportunities for the adoption of advanced heat exchange solutions in non‑industrial applications, illustrating the expanding scope of the market beyond traditional industrial end‑users.

India Heat Exchanger Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Shell & Tube Heat Exchangers, Plate Heat Exchangers, Air Cooled Heat Exchangers, Finned Tube Heat Exchangers, others), |

| By End-User / Industry | (Power Generation, Chemical & Petrochemical, Oil & Gas, Automotive & Manufacturing, Food & Beverage / Pharma, HVAC / Building Services, others), |

| By Application | (Process Heating / Cooling, Energy Recovery / Waste Heat Recovery, Refrigeration & Air Conditioning, Steam Condensation / Boiler Systems, others), |

| By Material Type | (Stainless Steel, Carbon Steel, Copper, Aluminum, others), |

India Heat Exchanger Market Driver:

Structural Industrial Energy Demand and Regulatory Efficiency Requirements

India’s industrial sector has become the country’s largest energy-consuming segment, responsible for over 50% of total final energy use, with energy‑intensive industries such as iron and steel, chemicals, and petrochemicals consuming a significant share of industrial power. This structural rise reflects sustained expansion in manufacturing and infrastructure development, necessitating equipment that enhances thermal efficiency and energy reuse in core processes. The increasing energy burden in industrial operations directly correlates with the growing adoption of heat transfer technologies that improve energy utilization and reduce operational inefficiencies.

Over recent years, the Perform, Achieve, and Trade (PAT) scheme, a key energy efficiency regulatory framework administered by the Bureau of Energy Efficiency (BEE), has intensified requirements for designated industrial units to reduce specific energy consumption. The scheme covers major energy‑intensive sectors, including steel, cement, petrochemicals, and textiles, mandating regular energy audits and compliance reporting. By embedding efficiency targets into regulatory obligations, industries are compelled to invest in thermal systems such as advanced heat exchangers to comply with energy performance norms, making efficient heat transfer technology a measurable requirement rather than an optional upgrade.

This driver materially expands market volume, not merely affecting pricing or short‑term adoption, because it fundamentally alters capital allocation in energy‑intensive industries toward technologies that deliver quantifiable efficiency gains and regulatory compliance. By linking regulatory performance to operational cost and industry benchmarks, PAT creates sustained demand for high‑efficiency heat exchangers as long‑term assets in industrial infrastructure. The regulatory impetus thus generates structural demand incrementally over time across regions and end‑users, embedding heat exchange technology within broader industrial energy optimization strategies supported by official policy and performance mandates.

India Heat Exchanger Market Trend:

Widespread Adoption of Industrial Waste Heat Recovery Systems and Energy‑Efficient Technologies

Industrial adoption of waste heat recovery systems (WHRS) has accelerated in India over recent years, emerging from rising energy costs, stringent efficiency norms, and the need to reduce carbon emissions in energy‑intensive sectors. WHRS integrates heat exchangers and related technologies to capture and repurpose excess thermal energy from manufacturing processes that would otherwise be lost, thereby improving overall energy efficacy . Government emphasis on energy efficiency under programs like the National Mission for Enhanced Energy Efficiency has bolstered industrial investment in heat recovery solutions.

This trend is causing structural change across the industrial value chain by shifting operational practices from reliance on external energy inputs toward internal energy optimization. Cement, steel, petrochemical, and refinery sectors increasingly deploy WHRS to pre‑heat inputs or generate steam/electricity from waste heat, reducing dependence on grid electricity and fossil fuels. Companies are integrating advanced heat exchanger designs, organic Rankine cycle units, and modular WHRS configurations to align with efficiency goals and environmental compliance requirements.

For example, Ramco Cements commissioned a 10 MW Waste Heat Recovery System (WHRS) at its Ramasamy Raja Nagar plant in September 2025 and is planning a 15 MW WHRS at Kolimigundala, Andhra Pradesh, highlighting large‑scale deployment of heat recovery systems that integrate heat exchangers into core operations. Tata Steel signed a Memorandum of Understanding in June 2025 to implement a Waste Heat Recovery project at its Ferro Alloys Plant in Athagarh, Odisha, which will deploy dedicated WHR systems to capture and reuse industrial heat as a structural investment in thermal efficiency.

The persistence of this trend is rooted in long‑term cost savings and regulatory expectations, positioning waste heat recovery and energy efficiency as strategic priorities rather than short‑term adaptations. Continued industrial expansion and rising industrial electricity tariffs incentivize deeper investments in energy management technologies. Additionally, the ongoing focus on reducing greenhouse gas emissions and achieving sustainability targets ensures that WHRS and energy‑efficient technologies will remain central to the evolution of India’s industrial landscape and the heat exchanger market.

India Heat Exchanger Market Challenge:

Lack of Adequately Trained Technical Personnel

One of the most critical barriers in India’s heat exchanger market is the lack of adequately trained technical personnel for installation, operation, and maintenance. Advanced heat exchanger systems, especially in chemical, power, and renewable energy sectors, require precise calibration, specialized welding, and knowledge of corrosion/fouling management. The Council on Energy, Environment, and Water (CEEW) found that 40 per cent of HVAC technicians in India have no formal training, and many received their last skill training over five years ago, showing a systemic lack of tech training relevant to thermal and HVAC systems.

This shortage exists due to limited vocational and industry-specific training programs focused on thermal systems and process equipment, despite government initiatives promoting energy efficiency and industrial modernization. Without targeted training programs, the knowledge gap remains, restricting the adoption of high-efficiency heat exchangers. Companies often rely on external experts, increasing project costs and slowing deployment timelines.

As a result, skill gaps materially constrain scalability and operational performance, particularly for SMEs that cannot afford to hire or train specialized staff. This leads to slower uptake of energy-efficient technologies, hinders compliance with government energy-efficiency schemes, and delays return on investment for new heat exchanger deployments. Addressing these gaps is essential for sustainable market growth.

India Heat Exchanger Market (2026-32) Segmentation Analysis:

The India Heat Exchanger Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Shell & Tube Heat Exchangers

- Plate Heat Exchangers

- Air Cooled Heat Exchangers

- Finned Tube Heat Exchangers

- Others

Shell & Tube Heat Exchangers (STHE) dominate the target market with a market share of 53% due to their adaptability across high-pressure and high-temperature industrial processes. Their design allows handling of large volumes and a wide range of fluids, making them indispensable in petrochemical, chemical, and power generation industries. Growing industrialization and the expansion of oil & gas infrastructure are primary market drivers that sustain their demand.

Government policies promoting energy efficiency and industrial modernization also favor STHE adoption. Incentives for power plants and petrochemical expansions ensure steady investment in technologies that rely on robust heat transfer equipment. Furthermore, regulatory frameworks emphasizing safety and operational reliability strengthen the preference for STHE over alternatives.

End-user demand characteristics reinforce this dominance. Large-scale industries prioritize durability, ease of maintenance, and long operational lifetimes, attributes where STHE excels. For example, A case study on Teknoflow heat exchangers shows an Indian plant implementing shell & tube units specifically to improve energy efficiency and reduce operating costs in manufacturing processes, highlighting performance benefits driving local demand. Additionally, continuous R&D innovations in tube materials and fouling resistance enhance their efficiency , securing long-term leadership in the market segment and ensuring sustained investor confidence.

Based on Material Type:

- Stainless Steel

- Carbon Steel

- Copper

- Aluminum

- Others

Stainless steel emerges as the leading material with a market share of 40% due to its superior corrosion resistance, thermal conductivity, and longevity under extreme operating conditions. Industries such as chemical processing, food & beverage, and pharmaceuticals prefer stainless steel heat exchangers for reliability and compliance with stringent hygiene and environmental standards.

Policy initiatives and environmental regulations indirectly promote stainless steel adoption by incentivizing materials that reduce maintenance frequency and minimize contamination risks. Investment flows are directed toward durable, low-maintenance materials that ensure operational continuity and reduce downtime costs, favoring stainless steel over alternatives like carbon steel or aluminum.

End-user demand for high-performance, low-risk equipment drives stainless steel leadership. Industries increasingly prioritize lifecycle cost efficiency and adaptability across multiple processes. For instance, Jindal Stainless (India’s largest stainless-steel producer) provides documented application cases showing how its stainless-steel grades are deployed across industrial equipment, including heat exchangers, tanks, and pressure vessels for chemical, petrochemical, power, and process industries. This highlights real industrial use of stainless steel in Indian process equipment applications where corrosion resistance and durability are critical for long‑term performance.

The combination of regulatory compliance, material performance, and industrial preference ensures stainless steel remains the dominant material, sustaining its market share and driving continuous innovation in heat exchanger design.

India Heat Exchanger Market (2026-32) Regional Analysis:

Maharashtra stands out as one of India’s most dominant industrial regions with a market share of 20% due to its large economic scale, diversified industrial ecosystem, and strong infrastructure network. Maharashtra hosts over 42,000 manufacturing units, spanning chemicals, petrochemicals, automotive, machinery, textiles, and engineering industries sectors that are intensive users of industrial equipment and process technologies. Industrial activity is highly concentrated in major districts such as Mumbai, Thane, Pune, Nashik, and Aurangabad, which collectively form one of India’s largest industrial corridors with integrated logistics, ports, and financial services infrastructure. This strong industrial concentration directly translates into high regional demand and market leadership.

Government policies and investment flows further strengthen Maharashtra’s leadership. The state attracted the highest foreign direct investment (FDI) in India during 2024–25, USD 17.7 billion, representing about 39% of national inflows, highlighting its position as the country’s primary industrial investment destination. In addition, Maharashtra announced the Industry, Investment, and Services Policy-2025, targeting USD 840 billion in investments and 50 lakh new jobs by 2030, which is expected to accelerate industrial expansion and equipment demand across manufacturing sectors.

Large-scale industrial development projects such as the Auric City industrial node, Samruddhi Expressway corridor, and Dighi Port industrial corridor are improving logistics connectivity and supporting manufacturing clusters, enabling industries to scale operations efficiently. These structural advantages create a favorable regulatory and infrastructure environment that sustains the region’s market dominance.

The presence of global financial and corporate headquarters in Mumbai, along with large manufacturing clusters in Pune, Nashik, and Aurangabad, creates a concentrated base of industrial buyers and investment decision-makers. This combination of industrial density, capital availability, and policy support positions Maharashtra as a dominant regional hub driving sustained market growth and adoption across industrial sectors.

Gain a Competitive Edge with Our India Heat Exchanger Market Report:

- The India Heat Exchanger Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The India Heat Exchanger Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- India Heat Exchanger Market Policies, Regulations, and Product Standards

- India Heat Exchanger Market Trends & Developments

- India Heat Exchanger Market Dynamics

- Growth Factors

- Challenges

- India Heat Exchanger Market Hotspot & Opportunities

- India Heat Exchanger Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Shell & Tube Heat Exchangers

- Plate Heat Exchangers

- Air Cooled Heat Exchangers

- Finned Tube Heat Exchangers

- others

- By End-User / Industry- Market Size & Forecast 2022-2032, USD Million

- Power Generation

- Chemical & Petrochemical

- Oil & Gas

- Automotive & Manufacturing

- Food & Beverage / Pharma

- HVAC / Building Services

- others

- By Application- Market Size & Forecast 2022-2032, USD Million

- Process Heating / Cooling

- Energy Recovery / Waste Heat Recovery

- Refrigeration & Air Conditioning

- Steam Condensation / Boiler Systems

- others

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- Stainless Steel

- Carbon Steel

- Copper

- Aluminum

- others

- By Region- Market Size & Forecast 2022-2032, USD Million

- North

- National Capital Region (Delhi NCR)

- Uttar Pradesh

- Punjab

- Rajasthan

- South

- Karnataka

- Tamil Nadu

- Kerala

- East

- West Bengal

- Odisha

- West

- Maharashtra

- Gujarat

- North

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Shell & Tube Heat Exchangers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By End-User / Industry- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Plate Heat Exchangers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By End-User / Industry- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Air Cooled Heat Exchangers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By End-User / Industry- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Finned Tube Heat Exchangers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By End-User / Industry- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Heat Exchanger Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Thermax Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HRS Process Systems Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Isgec Heavy Engineering Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kirloskar Brothers Limited (KBL)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BGR Energy Systems Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Heatex Industries Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kinam Engineering Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Universal Heat Exchangers Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Artson Engineering Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thermax Limited

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now