Asia Pacific Dental Equipment Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Product Type (Dental Radiology Equipment, Dental Chairs & Equipment, CAD/CAM Systems, Dental Lasers, Dental Surgical Equipment, Instrument Delivery Systems), By Treatment Type ( ... Orthodontic Equipment, Endodontic Equipment, Periodontic Equipment, Prosthodontic Equipment, Implantology Equipment, General Dentistry Equipment), By End User (Dental Clinics, Hospitals, Dental Laboratories, Academic & Research Institutes), and others Read more

- Healthcare

- Mar 2026

- Pages 210

- Report Format: PDF, Excel, PPT

Asia Pacific Dental Equipment Market

Projected 7.92% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 2.31 Billion

Market Size (2032)

USD 3.65 Billion

Base Year

2025

Projected CAGR

7.92%

Leading Segments

By End User: Dental Clinics

Asia Pacific Dental Equipment Market Report Key Takeaways:

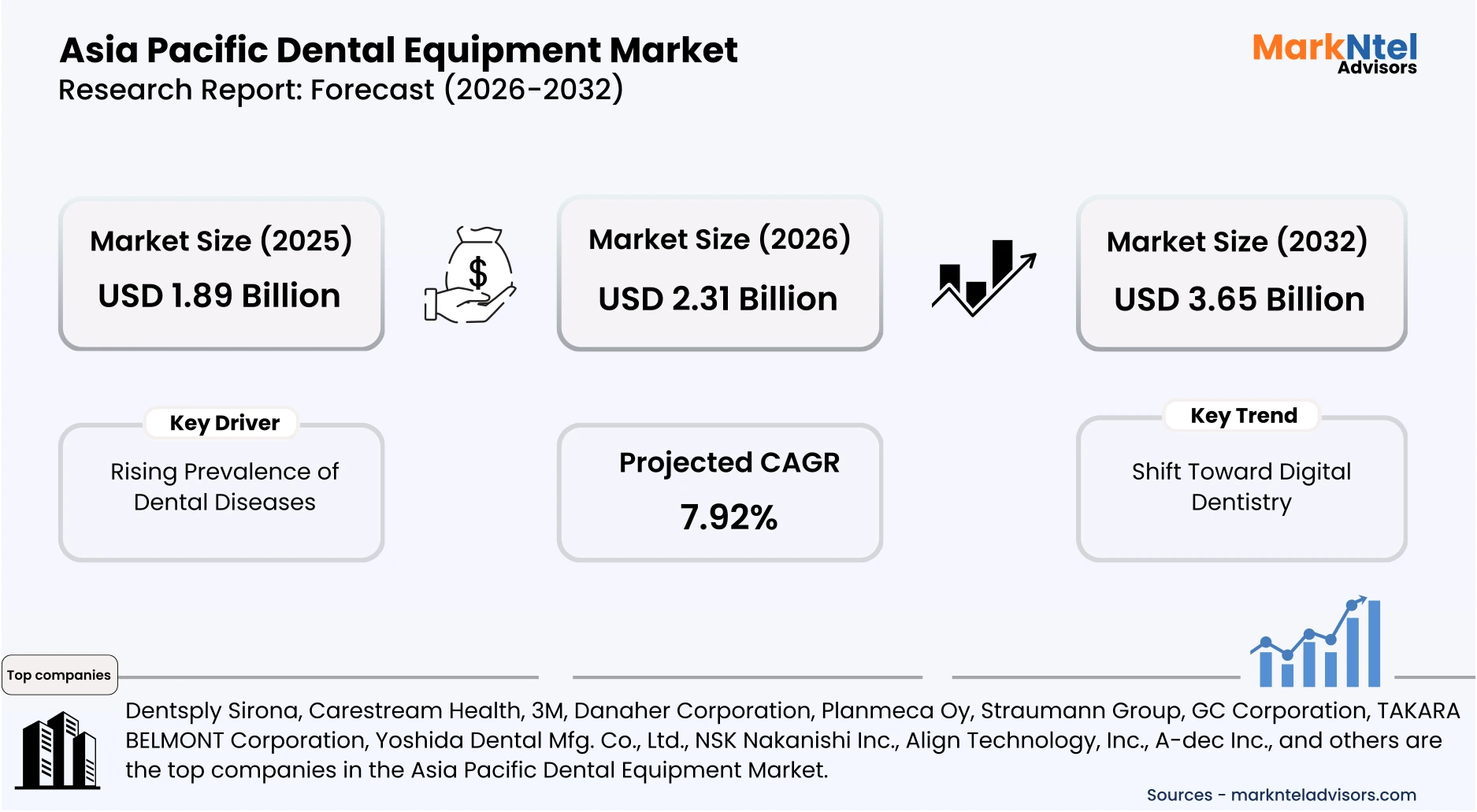

- The Asia Pacific Dental Equipment Market size was valued at around USD 1.89 billion in 2025 and is projected grow from USD 2.31 billion in 2026 to USD 3.65 billion by 2032, exhibiting a CAGR of 7.92% during the forecast period.

- China holds the largest market share of about 31% in the Asia Pacific Dental Equipment Market in 2026.

- By Product Type, the Dental Radiology Equipment segment represented a significant share of about 28% in the Asia Pacific Dental Equipment Market in 2026.

- By End-User, the Dental Clinics segment presented a significant share of about 68% in the Asia Pacific Dental Equipment Market in 2026.

- Leading dental equipment companies in the Asia Pacific market are Dentsply Sirona, Carestream Health, 3M, Danaher Corporation, Planmeca Oy, Straumann Group, GC Corporation, TAKARA BELMONT Corporation, Yoshida Dental Mfg. Co., Ltd., NSK Nakanishi Inc., Align Technology, Inc., A-dec Inc., and others.

Market Insights & Analysis: Asia Pacific Dental Equipment Market (2026-32):

The Asia Pacific Dental Equipment Market size was valued at around USD 1.89 billion in 2025 and is projected grow from USD 2.31 billion in 2026 to USD 3.65 billion by 2032, exhibiting a CAGR of 7.92% during the forecast period, i.e., 2026-32.

The Asia Pacific dental equipment industry has demonstrated steady expansion, supported by rising oral disease burden and improving healthcare access across the region. According to the World Health Organization, oral diseases affect approximately 3.7 billion people globally, with a disproportionate burden in low- and middle-income regions, including much of the Asia Pacific. Governments in major economies such as China and India have strengthened public healthcare systems and expanded dental infrastructure. These developments have historically increased treatment volumes and supported sustained demand for diagnostic and therapeutic dental equipment.

Current market conditions are driven by institutional end users, particularly dental clinics and hospitals, which account for the majority of equipment procurement. In India, the National Health Mission supports the establishment of dental units in public healthcare facilities, improving access in underserved regions . China’s Healthy China 2030 initiative emphasizes preventive care and oral health awareness, leading to higher patient inflow and service utilization. These policy-driven expansions, combined with the rapid growth of private dental clinics, are accelerating investments in advanced dental technologies.

Regulatory frameworks and reimbursement systems play a critical role in shaping market dynamics, particularly in developed economies such as Japan. Japan’s universal health insurance system provides comprehensive dental coverage, with a significant portion of diagnostic and restorative procedures reimbursed by the government. With annual public healthcare expenditure exceeding USD 400 billion, dental services are well-integrated within the national system, ensuring consistent treatment demand. This reimbursement-driven model supports continuous adoption of advanced dental equipment and stable long-term industry growth.

Looking ahead, the market outlook remains positive, supported by demographic shifts, rising income levels, and ongoing policy support across the Asia Pacific. The region’s aging population is accelerating, with elderly individuals expected to exceed 570 million by 2050 , significantly increasing demand for restorative and implant procedures. Countries such as Japan, where nearly 30% of the population is aged 65 and above, are witnessing sustained treatment volumes. Additionally, the expansion of nearly 200 million middle-class households across developing Asia is driving higher healthcare spending, further supporting long-term demand for dental equipment.

Asia Pacific Dental Equipment Market Recent Developments:

- 2025 : Dentsply Sirona upgraded its Primescan 2 intraoral scanning system with enhanced digital workflow capabilities and improved scanning accuracy. The innovation supports cloud-based dentistry and seamless chairside integration, strengthening digital adoption across Asia Pacific clinics.

- 2026 : Dentsply Sirona introduced new CEREC milling machines, including expanded variants alongside Primemill. The portfolio enables clinics to choose solutions based on budget and workflow complexity, accelerating digital dentistry adoption globally and in the Asia Pacific.

Asia Pacific Dental Equipment Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Dental Radiology Equipment, Dental Chairs & Equipment, CAD/CAM Systems, Dental Lasers, Dental Surgical Equipment, Instrument Delivery Systems), |

| By Treatment Type | (Orthodontic Equipment, Endodontic Equipment, Periodontic Equipment, Prosthodontic Equipment, Implantology Equipment, General Dentistry Equipment), |

| By End User | (Dental Clinics, Hospitals, Dental Laboratories, Academic & Research Institutes), |

Asia Pacific Dental Equipment Market Driver:

Rising Prevalence of Dental Diseases

The rising prevalence of dental diseases has intensified across the Asia Pacific due to rapid urbanization, dietary shifts, and limited preventive care access. According to the World Health Organization, nearly 50% of the population in the South-East Asia region is affected by oral diseases, representing over 1 billion cases. Peer-reviewed evidence from the Global Burden of Disease Study identifies untreated dental caries as the most prevalent health condition globally . This expanding disease burden has significantly increased the need for continuous dental diagnosis and treatment.

The impact is clearly visible across end-user segments, particularly dental clinics and hospitals, which are experiencing rising patient volumes. More than 900 million untreated cases of dental caries, periodontal disease, and tooth loss in the region highlight a substantial backlog of treatment demand. In India, recent evidence indicates that the country accounts for over one-third of global oral cancer cases, with nearly 20% occurring in individuals under 45, reflecting changing risk exposure. These trends are driving higher utilization of diagnostic imaging systems, dental chairs, and surgical equipment across healthcare facilities.

This driver materially expands market volume by increasing the frequency and necessity of dental procedures rather than influencing pricing alone. Chronic oral conditions require repeated interventions such as fillings, root canal treatments, and periodontal therapies, ensuring sustained equipment usage. The large untreated population further creates a continuous pipeline of patients requiring care over the long term. Consequently, the persistent and growing disease burden is establishing a stable and recurring demand base, supporting long-term expansion of the dental equipment industry across the Asia Pacific.

Asia Pacific Dental Equipment Market Trend:

Shift Toward Digital Dentistry

The shift toward digital dentistry has accelerated across the Asia Pacific due to increasing demand for precision-driven and efficiency-oriented care delivery. Digital tools such as intraoral scanners, CAD/CAM systems, and 3D imaging are replacing conventional impression techniques. The World Health Organization’s Global Strategy on Digital Health 2020–2025 has further encouraged integration of digital technologies into healthcare systems. This policy direction is enabling standardized, technology-driven diagnostic and treatment workflows across clinical settings.

This trend is restructuring the dental care value chain by reducing reliance on manual processes and external laboratories. Chairside CAD/CAM systems enable same-day restorations, improving patient throughput and operational efficiency. For instance, in 2025, SHINING 3D Dental launched the Aoralscan Elf intraoral scanner integrated with artificial intelligence features such as IntelliBite and an Intelligent Plaque Management Suite, enabling automated diagnostics and real-time analysis. Such innovations demonstrate a transition from standalone equipment to intelligent, software-integrated clinical platforms.

The trend is expected to persist due to measurable improvements in clinical accuracy and workflow efficiency. Peer-reviewed studies indicate that digital impressions improve precision and reduce procedural errors compared to conventional methods. Additionally, increasing investments by clinics in digital infrastructure to enhance patient experience and competitiveness are reinforcing adoption. As a result, digital dentistry is becoming a structural standard, fundamentally reshaping equipment demand and long-term industry dynamics across the Asia Pacific.

Asia Pacific Dental Equipment Market Opportunity:

Growth in Cosmetic and Implant Dentistry

The growth of cosmetic and implant dentistry presents a strong structural opportunity driven by demographic and behavioral shifts across the Asia Pacific. According to the United Nations, the region’s population aged 65 and above is projected to exceed 570 million by 2050, increasing demand for restorative and implant procedures. Additionally, the World Health Organization highlights a high and persistent burden of oral diseases across the region, necessitating advanced treatment solutions. These factors are expanding the patient base seeking both functional and aesthetic dental interventions.

This opportunity translates into tangible equipment demand through increased procedure volumes requiring imaging systems, CAD/CAM technologies, and implantology equipment. Real-world treatment patterns further support this trend, with Thailand attracting a large number of international dental patients annually due to treatment costs that are up to 50–70% lower than Western markets, supported by advanced digital technologies. This influx of patients is driving clinics to upgrade infrastructure and adopt precision-driven equipment. As a result, demand for high-value dental technologies is expanding across both domestic and international care settings.

The opportunity is particularly favorable for new entrants due to the fragmented and price-sensitive nature of the regional market. Emerging players can differentiate by offering cost-effective implant systems and digital solutions tailored to mid-tier clinics. Unlike established incumbents focused on premium segments, smaller firms can scale through localized manufacturing and flexible pricing strategies. This enables new entrants to capture high-growth segments while addressing unmet demand in rapidly expanding urban and medical tourism-driven markets.

Asia Pacific Dental Equipment Market Challenge:

High Cost of Advanced Dental Equipment

The high cost of advanced dental equipment remains a critical structural barrier limiting adoption across the Asia Pacific. Technologies such as CBCT imaging systems and CAD/CAM units require substantial upfront investment, with CBCT machines costing approximately USD 50,000–100,000 and digital systems reaching up to USD 150,000 . Additional expenses related to software, maintenance, and training further increase total ownership costs. These capital requirements have intensified in recent years with the rapid shift toward digital dentistry and advanced clinical workflows.

This challenge is particularly evident among small and mid-sized dental clinics, which dominate the regional healthcare landscape but operate under financial constraints. In emerging economies such as India and Indonesia, limited access to financing and lower healthcare spending restrict the ability of clinics to invest in high-cost technologies. As a result, many practices continue to rely on conventional equipment, delaying digital adoption. This creates a measurable gap between technologically advanced urban centers and resource-constrained facilities in semi-urban and rural regions.

The high cost of equipment materially restricts market expansion by limiting new market entry and slowing replacement cycles. Elevated capital investment increases operational risk and extends return-on-investment periods, discouraging adoption among smaller players. Consequently, demand for advanced systems remains concentrated among premium clinics and hospital chains, reducing overall market penetration. This structural cost barrier continues to hinder scalability, limit competitive diversity, and slow the widespread adoption of advanced dental technologies across the Asia Pacific.

Asia Pacific Dental Equipment Market (2026-32) Segmentation Analysis:

The Asia Pacific Dental Equipment market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Dental Radiology Equipment

- Dental Chairs & Equipment

- CAD/CAM Systems

- Dental Lasers

- Dental Surgical Equipment

- Instrument Delivery Systems

Dental radiology equipment dominates the Asia Pacific dental equipment market, accounting for approximately 28% of total demand, primarily because diagnostic imaging is a mandatory prerequisite for nearly all dental procedures. According to the World Health Organization, oral diseases affect a significant portion of the population in low- and middle-income countries, including much of the Asia Pacific, requiring routine screening and early diagnosis. Procedures such as implants, orthodontics, and endodontics depend heavily on imaging systems like intraoral X-rays and CBCT for accurate treatment planning. This universal application across treatment types ensures consistently high utilization of radiology equipment.

Infrastructure expansion and policy-driven healthcare development further reinforce this dominance. Governments in countries such as China and India are strengthening public healthcare systems and expanding dental units under national health programs, increasing access to diagnostic services. These initiatives are driving higher patient volumes in hospitals and clinics, where imaging systems are essential for both initial assessment and follow-up care. Additionally, regulatory emphasis on accurate diagnostics and patient safety is encouraging the adoption of advanced imaging technologies across clinical settings.

Industrial and technological advancements also contribute to the segment’s leading position. Manufacturers are introducing digital radiography and AI-enabled imaging systems that improve diagnostic accuracy and workflow efficiency, making them indispensable in modern dental practices. Unlike other equipment categories that are procedure-specific, radiology systems are utilized across multiple treatment applications, ensuring a higher return on investment. This combination of universal demand, policy support, and technological integration positions dental radiology equipment as the dominant segment in the Asia Pacific market.

Based on End User:

- Dental Clinics

- Hospitals

- Dental Laboratories

- Academic & Research Institutes

Dental clinics dominate the Asia Pacific dental equipment market by end user, accounting for approximately 68% of total demand, primarily because the majority of dental care is delivered through outpatient settings. According to peer-reviewed evidence, over 80% of dentists operate in private clinic settings, while nearly 68% of patient visits occur in these facilities, reflecting a strong clinic-centric care model. The high frequency of routine and elective procedures, such as diagnostics, fillings, and implants, ensures continuous patient flow into clinics. This concentration of service delivery directly drives consistent demand for dental equipment in these settings.

The fragmented healthcare structure across the Asia Pacific further reinforces this dominance. Countries such as India, China, and Southeast Asian nations have a large number of independent dental clinics compared to hospital-based dental departments, improving accessibility across urban and semi-urban areas. Rising income levels and increasing awareness of oral healthcare are encouraging patients to prefer private clinics for faster and specialized treatment. This shift is increasing procedural volumes and accelerating equipment adoption within clinic environments.

Additionally, dental clinics are more agile in adopting advanced technologies to remain competitive and enhance patient experience. Investments in digital imaging, CAD/CAM systems, and modern treatment equipment are increasingly common among private practitioners. Unlike hospitals, which allocate resources across multiple departments, clinics focus exclusively on dental care, resulting in higher equipment utilization rates. This combination of high patient volume, widespread presence, and rapid technology adoption positions dental clinics as the dominant end-user segment in the Asia Pacific market.

Asia Pacific Dental Equipment Market (2026-32): Regional Projection

China dominates the Asia Pacific dental equipment market, accounting for approximately 31% of total regional demand, primarily due to its large population base and expanding healthcare infrastructure. According to the National Bureau of Statistics of China, the country’s population exceeds 1.4 billion, creating a substantial patient pool requiring dental care services . This high demand is further supported by the increasing prevalence of oral diseases and the rising awareness of preventive and restorative treatments. As a result, the volume of dental procedures in China remains significantly higher than in other regional markets.

This dominance is reinforced by strong government-led healthcare initiatives and infrastructure expansion. Under the Healthy China 2030 strategy, the government is actively promoting oral health awareness and improving access to medical services, including dental care . Public hospitals and dental institutions are being upgraded, while private dental chains are rapidly expanding across urban centers. These developments are increasing patient inflow and driving large-scale procurement of diagnostic and treatment equipment across both public and private healthcare facilities.

China’s manufacturing capabilities and industrial ecosystem further strengthen its leading position in the market. The country is a major producer of medical devices, supported by established supply chains, cost advantages, and domestic production capacity. This enables local availability of dental equipment at competitive prices, improving accessibility for clinics and hospitals. Combined with high treatment volumes, policy support, and manufacturing strength, these factors position China as the dominant country in the Asia Pacific dental equipment market.

Gain a Competitive Edge with Our Asia Pacific Dental Equipment Market Report:

- Asia Pacific Dental Equipment Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Asia Pacific Dental Equipment Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Asia Pacific Dental Equipment Market Policies, Regulations, and Product Standards

- Asia Pacific Dental Equipment Market Trends & Developments

- Asia Pacific Dental Equipment Market Dynamics

- Growth Factors

- Challenges

- Asia Pacific Dental Equipment Market Hotspot & Opportunities

- Asia Pacific Dental Equipment Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Dental Radiology Equipment

- Dental Chairs & Equipment

- CAD/CAM Systems

- Dental Lasers

- Dental Surgical Equipment

- Instrument Delivery Systems

- By Treatment Type- Market Size & Forecast 2022-2032, USD Million

- Orthodontic Equipment

- Endodontic Equipment

- Periodontic Equipment

- Prosthodontic Equipment

- Implantology Equipment

- General Dentistry Equipment

- By End User- Market Size & Forecast 2022-2032, USD Million

- Dental Clinics

- Hospitals

- Dental Laboratories

- Academic & Research Institutes

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia-Pacific

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Dental Equipment Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Treatment Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Dental Equipment Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Treatment Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Dental Equipment Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Treatment Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- South Korea Dental Equipment Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Treatment Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Australia Dental Equipment Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Treatment Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Southeast Asia Dental Equipment Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Treatment Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Asia Pacific Dental Equipment Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Dentsply Sirona

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Carestream Health

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- 3M

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Danaher Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Planmeca Oy

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Straumann Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GC Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TAKARA BELMONT Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yoshida Dental Mfg. Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NSK Nakanishi Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Align Technology, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- A-dec Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dentsply Sirona

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now