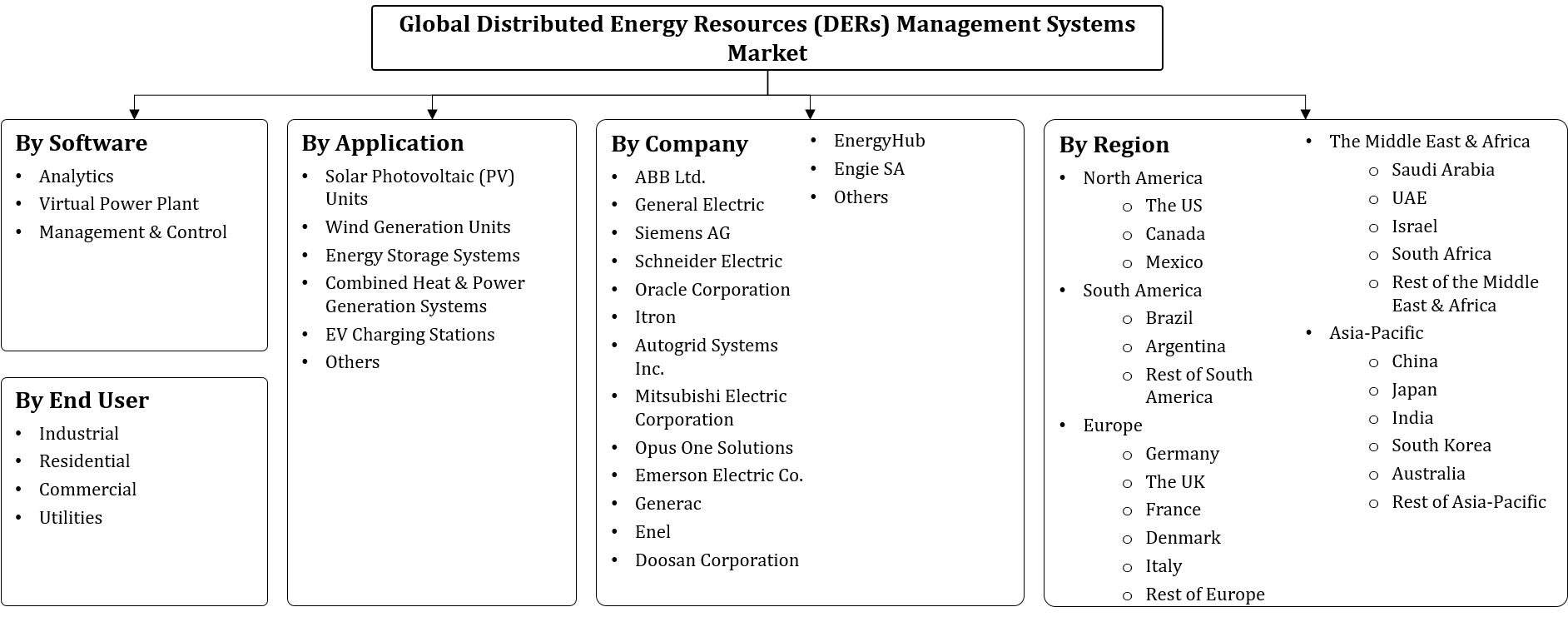

Distributed Energy Resources (DERs) Management Systems Market Report - By Software (Analytics, Virtual Power Plant, Management & Control), By Application (Solar Photovoltaic (PV) Units, Wind Generatio... ... nits, Wind Generation Units, Energy Storage Systems, Combined Heat & Power Generation Systems, EV Charging Stations, Others), By End User (Industrial, Residential, Commercial, Utilities), and Others Read more

- Energy

- Mar 2026

- 450

- PDF, Excel, PPT

Global Distributed Energy Resources (DERs) Management Systems Market Report Key Takeaways:

- The Global Distributed Energy Resources (DERs) Management Systems market size was valued at USD 0.78 billion in 2025 and is projected to grow from USD 0.89 billion in 2026 to USD 3.6 billion by 2032, exhibiting a CAGR of 26.23% during 2026-32.

- North America is the leading region with a significant share of 39% in 2026.

- By Software type, the Management and control segment represented a significant share of about 68% in the Global Distributed Energy Resources (DERs) Management Systems Market in 2026.

- By application, the Solar PV cells seized a significant share of about 42% in the Global Distributed Energy Resources (DERs) Management Systems Market in 2026.

- Leading companies are ABB Ltd., General Electric, Siemens AG, Schneider Electric, Oracle Corporation, Itron, AutoGrid Systems Inc., Mitsubishi Electric Corporation, Opus One Solutions, Emerson Electric Co., Generac, Enel, Doosan Corporation, EnergyHub, Engie SA, and Others.

Market Insights & Analysis: Global Distributed Energy Resources (DERs) Management Systems Market (2026-32):

The Global Distributed Energy Resources (DERs) Management Systems market size was valued at USD 0.78 billion in 2025 and is projected to grow from USD 0.89 billion in 2026 to USD 3.6 billion by 2032, exhibiting a CAGR of 26.23% during the forecast period. i.e., 2026-32.

The global adoption of distributed energy resources (DERs) has strengthened significantly as renewable electricity additions are expected to reach nearly 4,600 GW between 2025 and 2030, with distributed solar PV and other DER technologies leading much of this expansion. DER management systems (DERMS) have emerged as a key technological response enabling utilities and grid operators to harness DER flexibility, manage bidirectional power flows, and safeguard grid stability amid variable generation and peak demand scenarios. Residential rooftop PV, behind‑the‑meter battery systems, and increasing electrification of end uses like demand response appliances require advanced monitoring and control capabilities that conventional grid infrastructure lacks, further reinforcing DERMS relevance.

Public sector initiatives are shaping how DER integration unfolds globally. In the United States, the Department of Energy published its Distributed Energy Resource Interconnection Roadmap in January 2025, offering actionable strategies to streamline DER interconnection processes, enhance data transparency, and bolster grid planning to accommodate rising DER deployment rates. Europe’s 2025–2026 policy agenda includes the European Grids Package, which aims to accelerate permitting and enhance digitalisation and flexibility in grid operations, thereby supporting smoother integration of DERs through smarter network planning and infrastructure investment frameworks. These regulatory developments are directly influencing the scope and sophistication of DERMS solutions, as regulators and system planners increasingly prioritize visibility, automation, and flexibility at the grid edge.

DERMS adoption varies across end‑use segments, with utility and commercial applications driving initial implementation due to their need to balance variable generation, manage congestion, and support reliability objectives. Residential segments are contributing to demand growth through behind‑the‑meter DER integration, often coupling solar PV and storage with demand response capabilities to reduce electricity costs and enhance resiliency in the face of grid outages. Industrial adopters are beginning to leverage DERMS to optimize distributed generation assets, integrate flexible load management, and participate in emerging flexibility services markets. Regional infrastructure investments and policy support for electrification and smart grid upgrades will continue to influence the distribution of DERMS deployments globally.

Forward‑looking prospects for the DERMS market are grounded in the accelerating shift toward electrification, grid modernization, and digitalization of energy systems. As DER penetration grows, system operators and grid planners will increasingly require tools that provide real‑time visibility, forecasting, and optimization capabilities to ensure grid resilience and operational efficiency. Continued evolution in data analytics, interoperability standards, and automation functions within DERMS platforms is expected to support a more flexible, reliable, and economically efficient grid, meeting both utility performance goals and end‑user expectations in a decarbonizing energy landscape.

Global Distributed Energy Resources (DERs) Management Systems Market Scope:

| Category | Segments |

|---|---|

| By Software | (Analytics, Virtual Power Plant, Management & Control), |

| By Application | (Solar Photovoltaic (PV) Units, Wind Generation Units, Energy Storage Systems, Combined Heat & Power Generation Systems, EV Charging Stations, Other), |

| By End User | (Industrial, Residential, Commercial, Utilities), |

Global Distributed Energy Resources (DERs) Management Systems Market Driver:

Growing Adoption of Renewable Energy in Power Generation

A foundational driver reshaping the global power sector and expanding demand for related energy technologies is the accelerated adoption of renewable energy in electricity generation under strong government policy frameworks. In 2024, renewable power additions worldwide totaled about 585 GW, accounting for over 90% of new global capacity growth and reflecting strong national targets, competitive auctions, and policy support mechanisms that prioritize clean generation deployment. This structural scale‑up reflects sustained policy incentives such as auctions, grid access rules, and capacity targets rather than sporadic market trends.

The measurable impact of renewable energy policy is also evident in specific national contexts. In India, official government data shows a record addition of 44.5 GW of new renewable capacity in 2025, raising total installed renewable capacity to approximately 254 GW by November 2025 and marking a more than 23 % year‑on‑year increase over 2024. These outcomes stem from sustained federal targets for non‑fossil fuel capacity and state‑level policies such as Renewable Energy Plans designed to accelerate deployment, thus structurally expanding renewable generation capacity. This expansion has driven utilities and grid planners to invest in systems capable of integrating larger shares of variable energy.

Importantly, this driver directly expands market volume because policy‑mandated renewable capacity growth requires corresponding grid integration technologies and energy management tools as a matter of infrastructure necessity rather than optional enhancement. Governments are embedding renewable targets into national strategies, making deployment of renewable generation and the related systems required to manage it a long‑term, enforceable outcome. The resultant increase in renewable generation creates sustained demand for complementary technologies, operational solutions, and digital grid management capacities, underlining how policy‑enabled deployment fundamentally enlarges market scale.

By anchoring renewable energy adoption in statutory targets, regulatory frameworks, and national plans, governments globally continue to catalyze structural demand that expands market size and supports long‑term technology investment across power systems. This makes policy‑driven renewable expansion the most influential and durable market driver today.

- Market Segmentation

- Introduction

- Market Definition

- Research Process

- Assumption

- Executive Summary

- Global Distributed Energy Resources (DERs) Management Systems Market Start-Up Ecosystem

- Entrepreneurial Activity

- Funding Received by Top Companies

- Key Investors Active in The Market

- Series Wise Funding Received

- Seed Funding

- Angel Investing

- Venture Capitalists (VC) Funding

- Others

- Global Distributed Energy Resources (DERs) Management Systems Market Trends & Development

- Global Distributed Energy Resources (DERs) Management Systems Market Dynamics

- Growth Drivers

- Challenges

- Global Distributed Energy Resources (DERs) Management Systems Market Hotspot & Opportunities

- Global Distributed Energy Resources (DERs) Management Systems Market Regulation & Policy

- Global Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- Analytics

- Virtual Power Plant

- Management & Control

- By Application- (USD Million)

- Solar Photovoltaic (PV) Units

- Wind Generation Units

- Energy Storage Systems

- Combined Heat & Power Generation Systems

- EV Charging Stations

- Other

- By End User- (USD Million)

- Industrial

- Residential

- Commercial

- Utilities

- By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- By Company

- Competition Characteristics

- Revenue Shares

- By Software- (USD Million)

- Market Size & Analysis

- North America Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- By Country

- The US

- Canada

- Mexico

- The US Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Canada Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Mexico Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Market Size & Analysis

- South America Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Argentina Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Market Size & Analysis

- Europe Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- By Country

- Germany

- The UK

- France

- Denmark

- Italy

- Rest of Europe

- Germany Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- The UK Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- France Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Denmark Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Italy Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Market Size & Analysis

- Middle East & Africa Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- By Country

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Saudi Arabia Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- UAE Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Israel Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- South Africa Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Market Size & Analysis

- Asia Pacific Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- China Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Japan Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- India Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- South Korea Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Australia Distributed Energy Resources (DERs) Management Systems Market Outlook, 2022- 2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Software- (USD Million)

- By Application- (USD Million)

- By End User- (USD Million)

- Market Size & Analysis

- Market Size & Analysis

- Global Distributed Energy Resources (DERs) Management Systems Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- ABB Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- General Electric

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Siemens AG

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Schneider Electric

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Oracle Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Itron

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Autogrid Systems Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Mitsubishi Electric Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Opus One Solutions

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Emerson Electric Co.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Generac

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Enel

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Doosan Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- EnergyHub

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Engie SA

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- ABB Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We’d love to understand what matters most to you.